RAIN in some parts of southern Australia has impacted rates of slaughter and saleyards numbers over the past week, however there’s been little change in direct consignment grid prices, with plenty of paddock cattle still being presented.

Most physical sales held early this week had smaller or rain-affected yardings, with prices for most processor cattle rising in line with tighter supply.

Current competitive over-the-hooks grids for kills in southern Queensland have good heavy cows this week on 540c/kg (same as last week, but coming after earlier 10-20c falls) and 610-620c on four-tooth grass heavy ox (also back 20c on rates seen earlier this month). Many northern processors are currently offering unpriced spaces only, with rates to be negotiated closer to slaughter date.

Current competitive over-the-hooks grids for kills in southern Queensland have good heavy cows this week on 540c/kg (same as last week, but coming after earlier 10-20c falls) and 610-620c on four-tooth grass heavy ox (also back 20c on rates seen earlier this month). Many northern processors are currently offering unpriced spaces only, with rates to be negotiated closer to slaughter date.

Central Queensland plants today are generally 10-20c behind those rates.

In southern states, kill spaces are also loading up, with one plant in the eastern region of South Australia booked through to the start of July. The most recent active grid in the region had 590c/kg on best cows and 670c on four-tooth ox. Southern regions of NSW show a similar supply pressure, with cows well down at 550c/kg and grass steer 690c.

Grainfed impact on processor congestion

Beef Central has written plenty about the congestion in processing space this year, as bigger cattle numbers have come forward.

On top of the obvious labour access and staff accommodation issues plaguing beef processors’ throughput Australia wide since COVID, another less obvious factor impacting current congestion in slaughter cattle space is the growth in grainfed cattle numbers, as cattle turnoff reaches its cyclical peak.

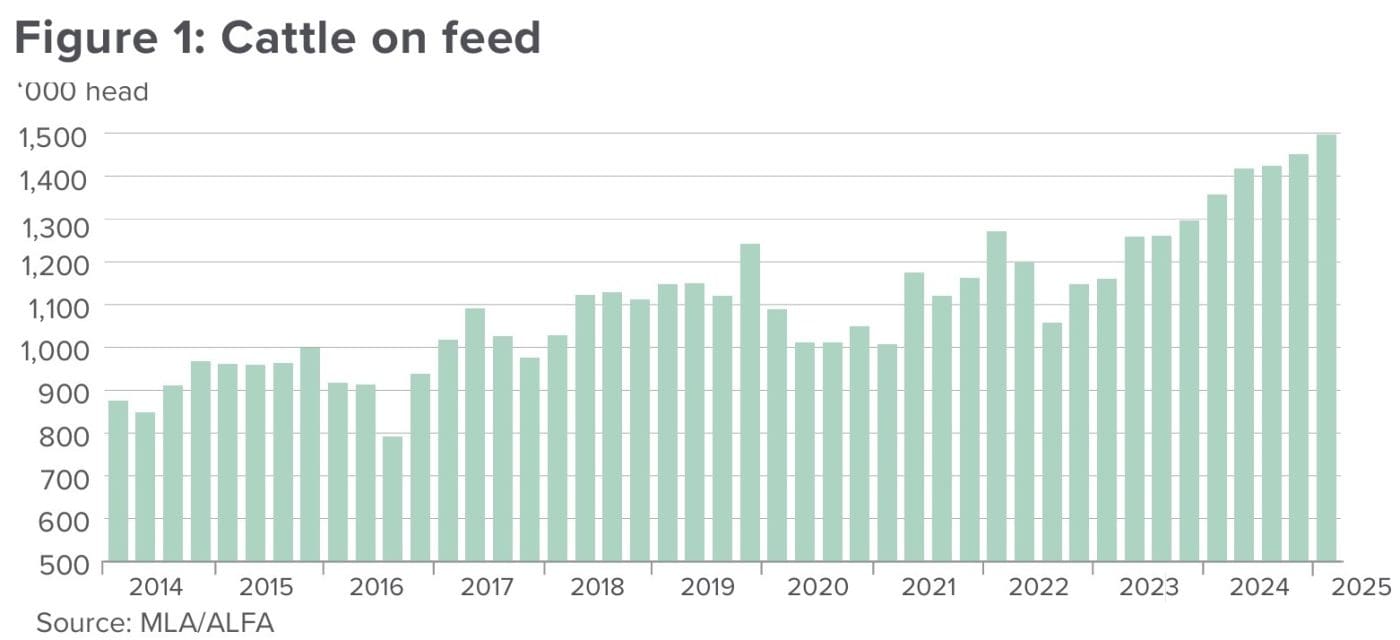

At the same time, there has been a relentless expansion in numbers of cattle on feed across Australia since 2022. The grainfed industry went within an inch of hitting 1.5 million head on feed for the first time in the March quarter just completed.

In the cattle on feed graph published here, numbers have increased almost 50pc since the third quarter of 2022. Each of the past eight quarters have been record high.

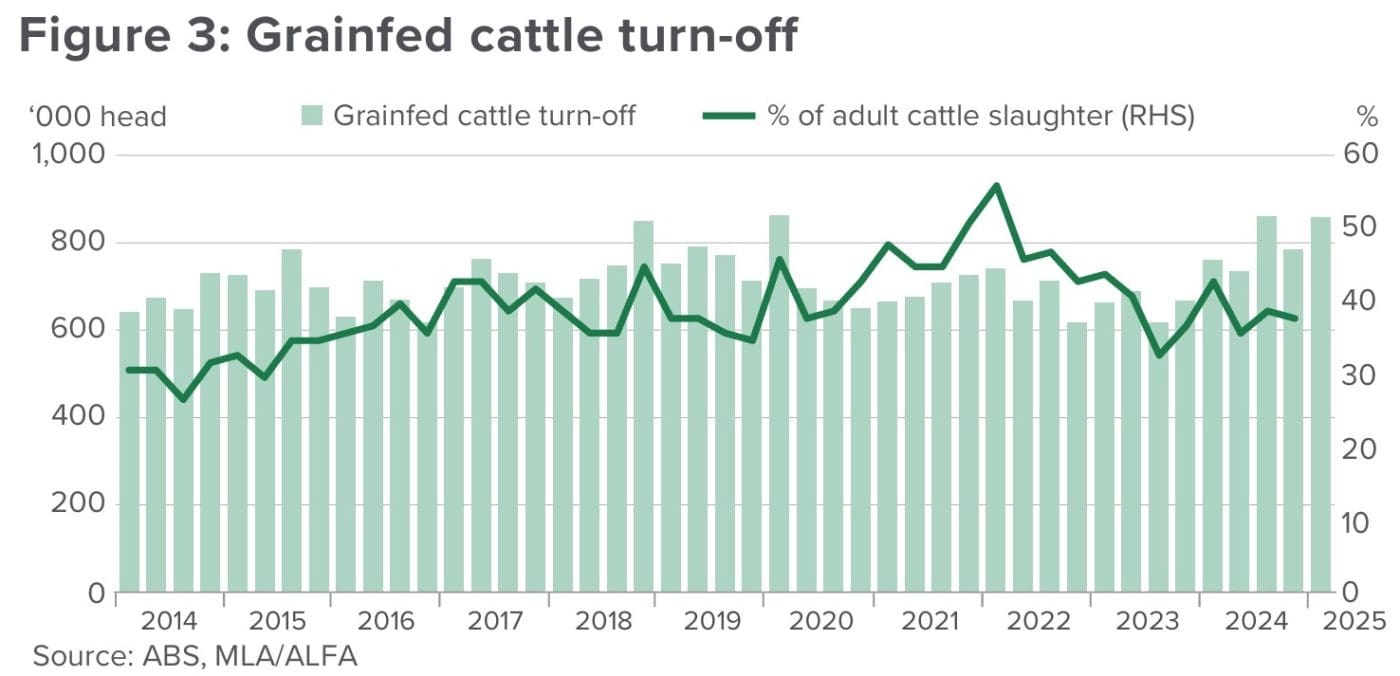

The second graph plotting turnoff published below shows a similar trend, with grainfed cattle turnoff growing from a little over 600,000 in late 2022, to around 850,000 in the March quarter this year. On top of that, average days on feed have expanded substantially over the same period, adding to average carcase weight, but somewhat moderating the ‘head count’ at slaughter. Average days on feed was calculated recently by Episode 3’s Matt Dalgleish at about 159 days, up from 120 days a decade ago.

If anything, that’s been a positive in the processing congestion issue. If average DOF was still 120 or less, it would mean even more grainfeds taking kill space priority over grassfed cattle.

The key point with the grainfed discussion above is that grainfed cattle inevitably take priority at the processing plant, when they have done their time in the feedyard. That means the proportion of available kill space left for ‘non-fed’ slaughter cattle (everything from cows and bulls to certified grassfed steer and heifer) is reduced, during periods of high supply like that we are currently experiencing. When seasonal supply of non fed cattle grows, as it recently has, it creates a pinch-point.

The counter argument to all this is the old saying that, “You can only kill them once,” meaning that each animal, regardless of whether it is grainfed or not, only occupies a single spot on the processor’s chain.

But what that does not acknowledge is that when the ‘inelastic’ grainfed footprint grows, the amount of remaining latent processing capacity available in the industry is reduced.

While during more orderly turnoff periods the issue is manageable, it’s during times like this when available kill space is tight that finding space for cows and bulls, and even some better grass-finished stock becomes problematic.

Expansion in some southern processing establishments over the past 12 months has helped, but its fair to say that a lot more processing plants are today housing a lot more grainfed cattle in their weekly intakes. A good example is JBS Dinmore, the nation’s single largest processing site. Dinmore today kills large numbers of grainfeds, whereas a decade or more ago, it was almost exclusively grass.

Similarly TFI’s Murray Bridge plant today processes far more grainfed cattle as a proportion of overall kill, than it ever did prior to the 2019 fire that destroyed the plant.

None of the above is anything the grainfed industry needs to apologise for, but it remains a fact that grainfed growth it intensifies the congestion issue for non-fed cattle in the current supply climate.

Slaughter edges higher to new season record

National seven-day slaughter for the week ended Friday edged higher to a new 2025 season record, accounting for 152,569 head. That was up another 173 head on the previous 2025 record set a week earlier.

Final clean-up after the series of holiday-shortened weeks partly explained the recent rise. NSW numbers actually went backwards last week, falling 1314 head on the previous seven days due to flood and access issues in the mid-north coast region around Coffs Harbour and Port Macquarie affecting some local processors. Other states lifted, with Queensland hitting 80,000 head for the first time this year, and Victoria lifting to 25,965 head.

Nationally, last week’s kill was up 13,200 head or 9.54pc on the same week last year. Female slaughter ratio remained high, at 48.67pc. much the same as the previous two weeks.

Worth noting, current rates of weekly slaughter around 150,000 head are still 11pc below the highs (regular weekly numbers above 165,000-170,000 head) of 2014, before the most recent labour access challenges emerged.

Saleyards trends

Most physical sales held early this week had smaller or rain-affected yardings, with prices for most processor cattle rising in line with supply.

Gunnedah sale this morning yarded 1860, up about 600 on last week. Rain through the drawing area precluded some drafts from being yarded. Heavy grown steers to process made 336c/kg and similar heifers to 28c/kg better 278-342c/kg. Score three and four cows gained 13-19c/kg selling from 253- 304c.

Wodonga sale this morning yarded 1300, down 530 on last week, with cows making up the bulk of the offering. Quality was mostly secondary with a lot of clean up lots in the mix. The market was notably stronger over all categories. Export cattle were in short supply across steer categories. In the export market competition was better due to the limited supply. The limited supply distorted price trends. Heavy steers and bullocks sold from 370-385c/kg. A mixed quality offering of cows saw all classes lift significantly in prices. Heavy cows gained 62c and traded from 308-335c/kg, while D2 and D3 cows less than 520kg sold to strong bidding making from 200-298c. Store cows were in bigger numbers making from 244-294c.

Wagga sale yesterday yarded 4500, down more than 2000 on the previous week, with rain having a substantial impact. The majority of the cattle were in store condition. The export market lacked supplies of heavy steers and bullocks to suit processors. Those available gained 20-52c/kg selling from 355-424c/kg. The cow market was a highlight with prices continuing to rise as the sale progressed. Heavy cows gained 44c selling from 290-338c/kg. Leaner types fetched 240-303c/kg,l with store cows from 258-306c/kg.

HAVE YOUR SAY