SLAUGHTER cattle supply has continued to tighten across Eastern Australia this week, in the face of local isolated storm rain delivering hope of the start of a more substantive seasonal break this side of Christmas.

Some of Queensland’s large multi-site export processors are now quite current for bookings, looking for cattle to fill shifts only ten days to a fortnight forward. Some vendors who were monitoring a slip in weights in mid-to-late October when conditions were hot and dry may now elect to hold cattle over until early 2026, confident that they will get under some storm rain in coming weeks.

That’s a substantial shift from conditions only two or three weeks ago when supply was looking reasonably solid through to seasonal closures from mid-December.

That’s a substantial shift from conditions only two or three weeks ago when supply was looking reasonably solid through to seasonal closures from mid-December.

The risk with the current cattle price surge, both through direct consignment and saleyards, is that some processors may elect to skip some days heading into Christmas shutdown period – or worse, close for the season early – rather than chase a slaughter cattle ever-higher heading into Christmas. That’s especially so if there is further and more widespread rain across cattle areas.

Oats-finished cattle have now run their race for the year, adding to the current supply squeeze.

In contrast with direct consignment supply, there’s evidence of some bigger yardings in the saleyards channel this week, with Gunnedah looking at around 4000 head, and Blackall also higher. Tamworth yarded almost 3500 yesterday, up 22pc on the previous week, reporting strong competition across the board for cattle to process and feed. Slaughter type cows were firm to 12c/kg dearer with 2 scores to processors selling from 215c to 392c/kg. Prime heavy score 3 and 4 cows sold from 368-428c/kg, close to the highs seen six or eight weeks ago.

Grids lift again

In southern Queensland, there’s been some solid rises in processor over-the-hooks offers since the weekend, with heavy cows up and 10-20c/kg to 710-730c/kg. Heavy grass steers are also higher, with grids this week offering 800-810c/kg, with up to 820c offered on some grids for no HGP cattle.

Central Queensland plants remain 10-20c/kg behind those rates.

Further south, in southern NSW some grids are up another 20c/kg on last week, at 800c/kg on cows and 870c/kg on a four-tooth, no-HGP grass ox. That’s close to, or even above, the highest point seen earlier in the 2025 season.

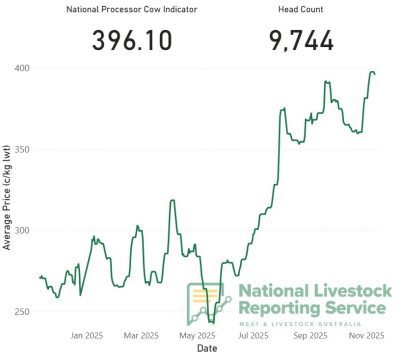

Cow price roller-coaster

Looking back at the meatworks cow market over the past six months, its been a volatile ride for prices.

Both direct consignment and saleyards slaughter cows began a deep and sustained price rally in May, with the NLRS processor cow indicator (see graph) rising from a season-low of 242c/kg liveweight back on 19 May to a high of 392c/kg four months later on 17 September – a 62pc lift.

The hot, dry weather than followed saw some confidence washed out of producers’ minds, leading to a surge in numbers and a mini-collapse in prices, back below 360c/kg by late October.

But since then, saleyards cow prices have rallied again, hitting a new 2025 season high of 397c/kg late last week. Renewed southern processor buying strength in Queensland, after a few quieter weeks, contributed to that. As of yesterday, the saleyards processor cow indicator say just below that number, at 396c/kg.

Southern processors remain active in northern markets but QLD processors have upped the ante pushing heavy cow bids in saleyards to 440c/kg as they seek to secure dwindling supplies leading into their seasonal shutdown.

Having been in Mareeba, Far North Queensland for a carcase competition on the weekend, Beef Central learned of Victorian buying activity locally, paying big money for local Brangus cows. This year southern NSW and Victorian processors have continued to press further and further north chasing killable cattle as the year has gone on. Charters Towers has been a hunting ground since around July, but Mareeba is another 400km further north, suggesting freight bills to get the cattle home might top $180-$200 a head, one contact said.

US lean trimmings market continues to edge higher

Part of the current surge in cow prices can be explained by the strong demand and price for lean imported trimmings into the US, Japan and other markets, worth close to 1170c/kg FAS in the most recent weekly quote, up 220c/kg or 24pc on this time last year.

Steiner Consulting’s most recent weekly imported US beef market summary suggested some slowing in trade the week before last, partly because of uncertainty about tariffs and the sharp decline in US fed cattle futures.

What was a rush to cover needs for the first quarter next year, especially with cow meat supplies expected to be limited over the holidays, was replaced with the hope of more supply and lower prices. Imported beef suppliers and traders, on the other hand, had to contend with the possibility of lower inventory value should US tariffs be struck down, resulting in a rush of lower-priced product.

Some domestic US buyers were taking advantage of the lower domestic fresh product (trading near par with imports) and keeping their frozen imported positions in place, Steiner reported.

Steiner reports imported 90CL beef prices into the US market traded firm for most of last week and by Friday they were only a couple of cents below the quoted price for US domestic fresh product.

The average discount narrowed to about US7c/lb below domestic fresh (this discount has been consistently around US30c/lb).

The narrowing discount largely reflects slower imports from South America. It’s also typical for imported 90CL beef to trade close to US domestic prices in Q4. Imports from New Zealand are limited until December, while US domestic cow meat supplies increase as they commence their autumn cow cull.

US end-users remain concerned about lean beef supplies, however. With Australia now the only major source of imported volume, buyers are prepared to pay close to domestic prices for imported product with the flexibility to schedule delivery two to four months out and without the cost to box, freeze and store it.

However, US import policies are adding uncertainty to trading conditions in the US market. In recent weeks Trump has increased access to Argentinean beef, while there is increasing pressure on the US Government from importers to reduce the Brazilian beef tariff and allow increased Brazilian beef imports as a measure to reduce the cost of living.

Meanwhile, the lawfulness of Trump’s tariff regime is currently being challenged in the US Supreme Court, which could have implications for imported prices in the US market.

As to when a decision may come, it could be as late as June next year, but some think it could come as early as December or early 2026. If the tariffs are suspended, it could result in a rush of shipments for fear that the Administration could use other arguments to implement them again. The effect has been to inject more uncertainty for the trade.