Beef Central’s final weekly kill report for 2013 brings absolutely nothing new to the table that has not been seen week-after-week since the start of the year.

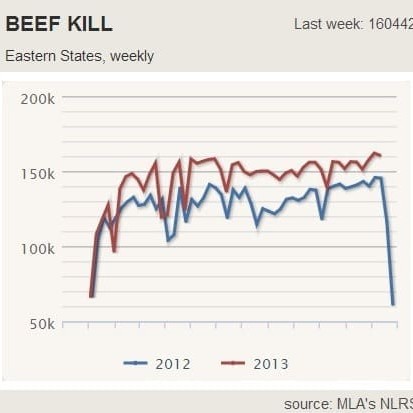

Once again, the Eastern States seven-day kill to Friday gathered by NLRS posted a colossal total of 160,442 head. That’s the second highest weekly kill reported this year – exceeded only by the previous week’s all-time record, driven by record kills in NSW and Victoria. It is all the more extraordinary because it was achieved so late in the slaughter year calendar.

Normally there is a tapering effect evident in Eastern States kills by mid-December, but with the nation’s largest processors all reporting full bookings right up to the season’s last killing day this Thursday, it now looks like there will be no respite in rates of kill until the northern export slaughter season closes.

Normally there is a tapering effect evident in Eastern States kills by mid-December, but with the nation’s largest processors all reporting full bookings right up to the season’s last killing day this Thursday, it now looks like there will be no respite in rates of kill until the northern export slaughter season closes.

Take a moment to look at the graph published here, drawn from Beef Central’s home-page ‘industry dashboard’ graphs. Save for the public holiday weeks where weekly kills are shortened, the trends for 2012 and 2013 show a gap of 10,000 to 15,000 head per week that has remained consistent virtually right throughout the year.

Year to date, average weekly slaughter for beef has been up 14pc compared with 2012, at 144,032 head.

In the breakdown of last week’s Eastern States kill, Queensland’s tally grew 2 percent from the previous week to reach 78,876 head, still 3pc above where it sat this time last year.

In NSW, kills fell 11pc from the all-time record previous week to 38,029 head, but was still +11pc from a year ago. Victoria was a whopping 32pc above this time last year at 29,341 head, while South Australia was 10pc up on last year, and +8pc on the previous week, at 9351 head.

Following the same trend, Tasmania’s kill last week at 4845 head was +2pc on the previous week and +12pc on last year.

Not surprisingly, record production this year has translated into record exports, with total shipped volume in 2013 exceeding last year’s annual total by mid-November, with six weeks of trade still to go.

Total Australian beef exports this year will reach an estimated 1.085 million tonnes – a colossal 119,000 tonnes more than total exports in 2012, which itself was a record export year (967,000t).

One of the most fortunate events to develop in 2013, in terms of protecting price in a heavily-oversupplied market, has been China’s insatiable demand for Australian beef.

Without the vigorous demand from China this year, Australia’s export price performance would have inevitably been dramatically worse, in terms of price, exporters say.

Virtually out of nowhere, China has emerged as one of Australia’s most valuable export markets in 2013. Calendar year to November, China took 140,700t of Australian beef, compared with just 25,200t for the same period last year. That’s a rise of 455pc, and places China behind only Japan (265,900t) and the US (195,000t) as Australia’s largest beef customers, having already surpassed South Korea.

At its current rate of growth, China could conceivably surpass the US as Australia’s second largest beef market some time next year.

Assisting Australia’s trading position at a time when beef production has surged in 2013 has been the recent decline of the A$, which fell this morning to US89.4c, its lowest level since early September. Looking further ahead, recent National Australia Bank forecasts have the currency softening to US86c by the end of 2014, which, if it eventuates, will continue to improve Australia’s trading position.

So what lies ahead for 2014?

What is clearly evident is that Australia’s rate of kill experienced throughout 2013 is unsustainable, and will have repercussions for the industry’s capacity to produce beef not only next year, but for several years hence.

What is clearly evident is that Australia’s rate of kill experienced throughout 2013 is unsustainable, and will have repercussions for the industry’s capacity to produce beef not only next year, but for several years hence.

As discussed in this earlier Beef Central article, this year’s drought event has not only impacted on average carcase weight in slaughter cattle, but has greatly elevated the rate of female kill (almost one million females have been removed from production systems since 2012). It will also impact on calving and branding performance rates achieved next year, and conception rates that will impact on calving/branding rates the year after that.

Average adult carcase weights this year have been back about 3pc on last year, at 278kg/head, underpinned by the high proportion of store-condition cattle slaughtered.

At the farm gate, cattle prices have reflected the oversupply/drought problem, after what were two excellent years of herd rebuilding.

As always, rain, or the lack of it, will dictate the flow of cattle and pricing trends in the early stages of the new year, but the general belief is that killable cattle will be very scarce during the first quarter, and perhaps beyond.

Northern meatworks grid prices inevitably take a few weeks to find a level in the new killing season, as the market again seeks to finds equilibrium.

Large Queensland processors closing down for their seasonal break this Friday already have grids posted for delivery in weeks starting January 6 and 13 next year. Those seen by Beef Central yesterday were unchanged from current rates, but that can change dramatically if weather influences intervene.

Even a modest wet season could make slaughter cattle very expensive during the early stages of 2014, but most extensive beef producing areas in eastern Australia are still a long way from achieving that.

- More on price and supply outlook for 2014 in an article later this week.