A ‘wall of meat’ is building in the United States in coming months, which will inevitably impact pricing for Australian cattle and beef early next year, warns independent meat and livestock analyst Simon Quilty.

Simon Quilty

The problem stems from the enormous back-log of cattle that has built up in the US beef industry since the onset of COVID-19, which has forced meat packing plant closures and created an alarming buildup of ‘unprocessed’ cattle in the system.

Close to 1.5 million slaughter-ready US cattle had been pushed back because of COVID impacts, he said.

Presenting a webinar hosted by NSW Local Land Services last night, Mr Quilty said some recent weeks had seen US cattle slaughterings down 35-40pc on normal production at this time of year, and as a result, US cattle prices had fallen 20 percent or more. At the same time, US retail prices, in response to lower production, had skyrocketed, he said.

“The net effect of those US cattle being held back has changed the global beef market,” Mr Quilty said.

Low kills impact

Due to the record drought last year, Mr Quilty expects Australian slaughterings to go from 8.4 million head in 2019 to 6.6 million this year, and even lower next year to 6.57m.

“The fundamental difference between slaughterings this year and next year, however, is that the animals hardest to find this year will be male cattle, which will be in very short supply. Next year, male cattle numbers will start to rebuild, while females will be very hard to find,” he said.

“There is always this delayed effect after herd liquidation, drought and rebuild, where steers are in shortest supply to begin with, followed a year later by females. This drought is no exception.”

Kicking the can down the road

Mr Quilty used the term, ‘kicking the can down the road’ to describe the action of pushing back a problem, for whatever reason.

“That’s exactly what’s going on when we look at US beef production at the moment. Because of what we described earlier, US producers are struggling to get their cattle placed in US feedlots at the moment, and then getting those cattle killed.

“That 1.5 million head backlog continues to build, as the US processing industry continues to struggle – albeit that the situation has improved slightly this week, but cattle are still backing up.

US production sharply lower

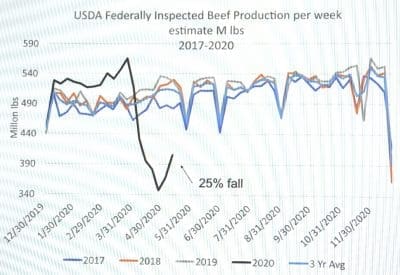

The USDA last week came out with revised predictions for beef, suggesting US beef production this year is likely to be 5.5pc lower than last year.

“Up until now, we were expecting 2020 US production to be higher than last year, but that was before COVID,” Mr Quilty said. “But USDA has now revised their figures due to the recent COVID impact on processing activity (see graph, 202 trend line in black), effectively kicking the can down the road. Those 1.5 million cattle are now going to be slaughtered next year,” he said.

“Up until now, we were expecting 2020 US production to be higher than last year, but that was before COVID,” Mr Quilty said. “But USDA has now revised their figures due to the recent COVID impact on processing activity (see graph, 202 trend line in black), effectively kicking the can down the road. Those 1.5 million cattle are now going to be slaughtered next year,” he said.

“That’s now lifted next year’s US beef production forecast up 6.7pc, and whenever that happens in America, there is significant impact on global pricing of beef, including in Australia,” he said.

The key question was: How far has the US kicked that can?

The USDA’s forecast 6.7pc increase in beef production next year represented about 780,000t of additional US beef, Mr Quilty said.

“In reality, the decisions about exactly when that impact is seen are being determined right now,” he said. “The US had had excellent rain, and pastures were in good condition. All the indications are that they are going to carry those 1.5 million head on pastures a lot longer, and as a result, when the decision is made, it is pretty much committed all the way through to August/September.”

“That’s the point where we will see those animals start going into feedlots in North America. Once they are on feed, the chances are we are going to see those same animals appear in slaughter in probably February, March and April next year – possibly starting as early as January.”

There was likely to be a condensed amount of US meat hit the market dramatically during the first quarter next year – 780,000t to be exact, Mr Quilty said.

“That is enough to really force the market down, which will impact beef prices, not only for the US, but also for Australia. That’s because we compete with the US in Japan, Korea, Indonesia and a host of other markets.”

“If the US has cheaper meat than we do, they are going to sell at much lower levels than we can, which will impact the price at which Australia can sell meat.”

It was important to understand that the US really set global beef prices, and arguably, lamb prices, he said.

“By understanding that, a good appreciation can be gained of just how severe this US beef carry-over of 780,000t is. It’s a ‘wall of meat’ that’s coming.”

How quickly can food service sector respond?

Those US cattle that would be held over to next year would create a hole in the US meat market in the August to November period this year, Mr Quilty said.

“Once again, that impacts global markets, because US exporters will be short of meat for export to Japan, Korea and other customer countries, as well as the US domestic market. Australia and the US share 87pc of the Japanese market, and more than 90pc of the Korean market in beef – so it is absolutely critical to understand when shortages (and excesses) in the US are going to occur.”

COVID restrictions easing

As discussed in last week’s report on an earlier LLS webinar presented by Mr Quilty, COVID restrictions are now starting to be lifted in many countries around the world.

“Fifty percent of the meat market is made up of food service – restaurants, hotels, bars, cafes, etc – and when they re-open, it will mean half the market can start to recover. That particularly affects the middle cuts like striploins, tenderloins and cube rolls that have proven exceptionally hard to sell under COVID,” he said.

“The sooner restrictions are lifted, the sooner the food service sector can get going again.”

In the US, half the states have started to lift restrictions, while in Asia, three key customer countries – China Vietnam and South Korea – have lifted, while others, including Japan have partially lifted restraints. In Europe, ten countries have lifted restrictions, and four are pending.

Australia has started lifting, while South America remained in ‘all sorts of trouble’, Mr Quilty said.

Once this trend gathered further pace, it would help drive recovery in beef in the food service market.

“The US as of this week has started killing a lot more cattle again, and as a result, certain meat prices have started to fall – not as dramatically as what they could if they were back to full production, but a slight correction,” he said.

“That effectively means more people are back to work in US meat plants, and therefore higher throughput, because they can kill more animals per day.”

Mr Quilty said the belief was that the US processing industry would not get back to normal production any time this year. “At best, they may get back to 80-90pc of normal capacity, because of absenteeism among workers and ongoing COVID spot-fire clusters.

“To me, this is critical, because it is going to help drive prices for beef this year,” he said.

Next year, US processors expected to get back to normal, which is when the backlog of this year’s US cattle will be killed.

Bounceback effect

In those US states that were now re-opening, a post-COVID ‘bounce-back’ effect was already taking place.

“My US contacts are saying people in those states are out partying, everywhere,” Mr Quilty said.

“Consumption is improving, and in particular, the US quick service restaurant sector is almost 80pc restored. It’s the white table-cloth restaurant end of food service which is still suffering.”

In the US, the general consensus was that about 50pc of food service is now back in business. A month or two ago, 80-90pc was shut. Imported beef was again starting to flow quickly through the US system, and prices had risen 10-15pc in the past two weeks on imported beef.

The bounceback effect and the predicted rise in US beef production early next year would largely negate themselves, Mr Quilty said, with the back-half of next year looking a lot more positive than the first half, on price.

He said projections had the US beef cut-out value declining sharply, and Australian export meat prices tended to correlate closely with US cut-out values, most of the time.

“Based on the dramatic amount of US meat we expect to see hit the market in the first quarter next year, I have the US cut-out falling – and we are going to fall with it,” he told last night’s webinar.

“The net effect is that Australia’s global meat values will fall in proportion to the value of what the US beef cut-out will fall – mainly felt in the first half of next year, because that’s when the volume starts to appear in the US market.”

Summarising topics raised in last week’s presentations, Mr Quilty said feedlot numbers in Australia were likely to fall by 30pc by mid-year, as middle cuts normally directed into food service were pushed back onto the domestic market, affecting meat pricing, and making it very unprofitable to feed cattle – especially Wagyu and longer-fed Angus types.

“But we know that the pipeline is empty, with record low feedlot placements in the US, also – and the market is starting to pick up on that,” he said.

At the frozen, commodity end of the animal, China over the past two or three years had played a critical role in forcing America to ‘pay up’ for grinding meat.

“But China has not fully recovered from COVID. It is showing signs of improving, but it is not the robust market that we enjoyed for most of last year,” he said.

Forecasts for feed and slaughter cattle price categories for 2021

Mr Quilty said there were opposing forces at play in the beef industry, with a dramatically tighter female kill in Australia, at the same time as over-supply of cattle was emerging in North America.

“If it had not been for US over-supply, I think we would have seen really strong prices going into next year. But US oversupply has dampened prices going into 2021.”

Feeder cattle

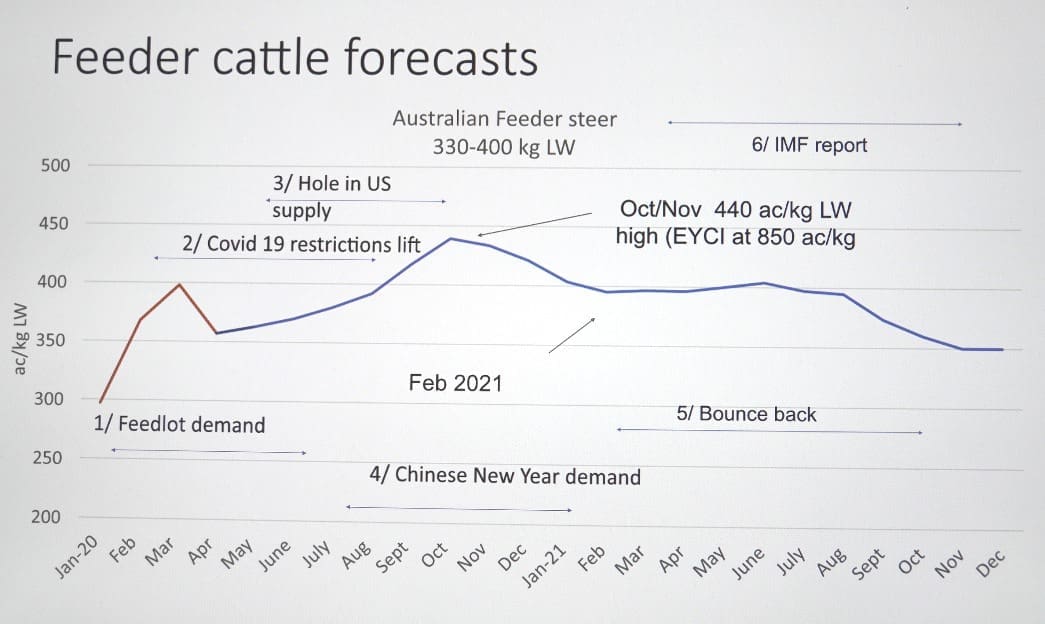

“Originally, a couple of months ago my forecasts had the peak for feeders in February/March, but as the production hole has appeared in North America, and pushed back the huge volume of meat into early next year, I have brought forward the high-point in the feeder market to October/November this year,” he said.

Mr Quilty said he had made some ‘outrageous’ predictions in forecasts he made 18 months ago, suggesting a high of 800c/kg for the Eastern Young Cattle Indicator, occurring around February March 2021.

“But as this hole in production has appeared in North America, pushing the huge volume of meat back into February-March 2021, I’ve effectively brought forward the high in the market into October/November, sitting at around 440c/kg liveweight for feeder steers (the equivalent of an EYCI worth 850c/kg dressed weight – considerably higher than his ‘outrageous’ forecasts published on Beef Central back in 2018).

“As we discussed earlier, this is the year it gets really tight on feeder steers,” he said.

Mr Quilty’s graph predictions, published here, have feeder steers falling back to just below 400c/kg by February 2021, due to the beef over-supply problem in North America early next year.

“But without some of the other positive factors out there, that dip could have been a lot lower,” he said.

Around September next year, there would probably be another step down, partly related to the Australian herd rebuild, and a somewhat higher male kill in Australia next year.

Six points (time-marked on the graph below) had impacted the feeder graph trend along the way:

1 – Feedlot demand: Lotfeeders were starting to realise they needed to start to re-fill pens, because out-front was starting to look ‘OK’ again. This was likely to produce a lot stronger feedlot demand over the next six to eight weeks, continuing through the rest of the year.

2 – COVID-19 restrictions start to lift, with food service sector demand finally starting to return

3 – Hole in US supply, likely to drive demand for beef in the August-September period

4 – Chinese New Year beef buying demand starts to lift September-November, and builds. The Chinese will be aware of over-buying for next year’s New Year period celebrations, because of what went on late last year, where they got out of control, however. Both buyers and sellers will be wary around New Year trading for next year

5 – Bounce-back effect, as consumers start to get out and socialise more often, as more and more restrictions are lifted, and government stimulus money circulates around the economies both overseas and in Australia

6 – IMF predictions of substantial 5.8pc growth in the world economy next year, as the COVID recovery process gathers pace.

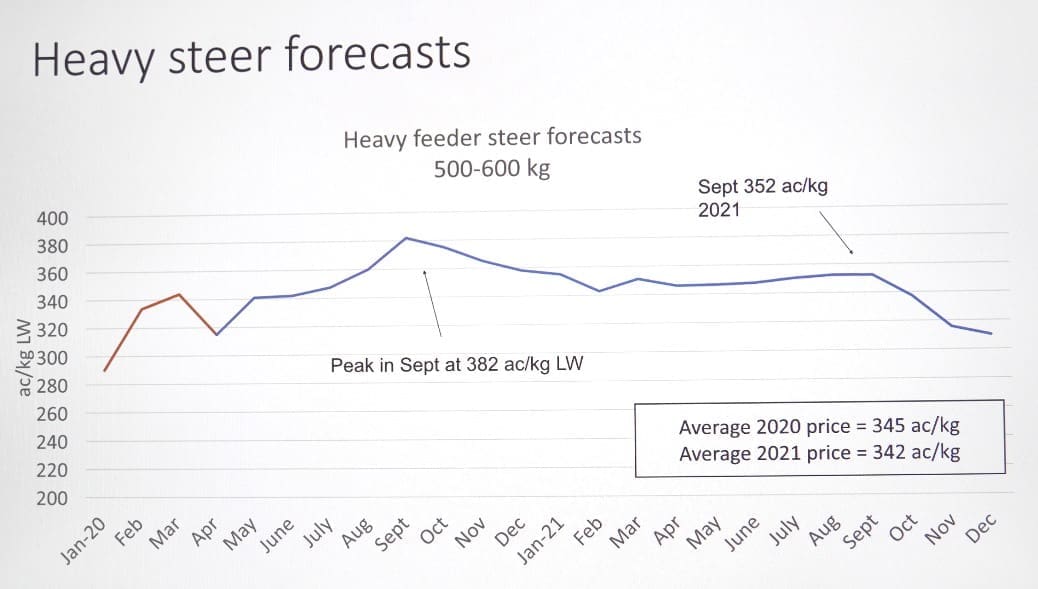

Heavy steers

Mr Quilty’s forecast for heavy steers is for the market to peak a month earlier than feeders, around September this year. With such good pasture conditions across most of Australia, this is one category which will be going hard to get as much weight on their animals, as early as possible. The market is likely to peak at around 382c/kg liveweight, before a dampening effect once volume starts to come onto the market towards the back end of next year. He has the average price for heavy grass steers next year at 342c/kg, virtually the same as 2020.

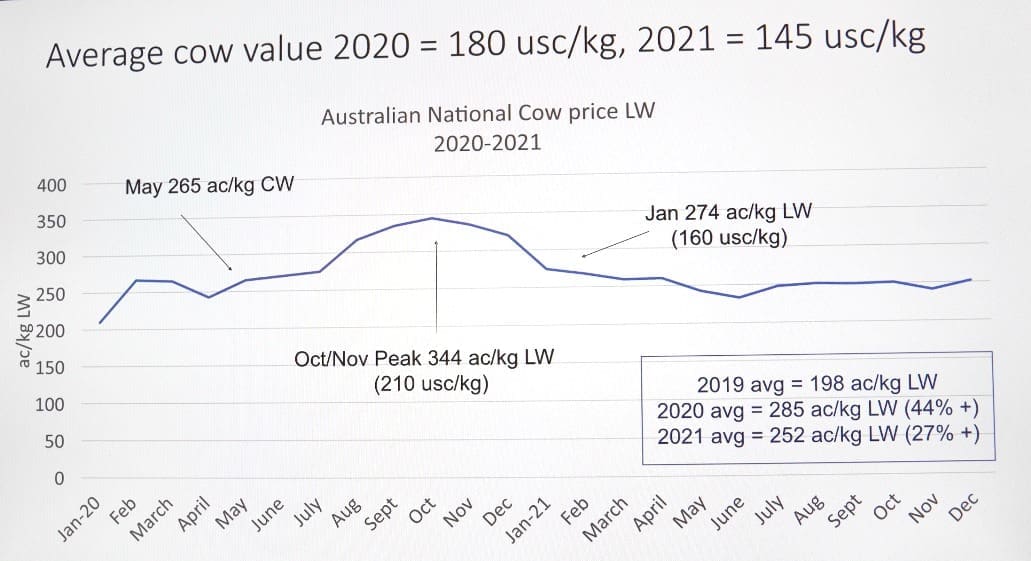

Cows

Mr Quilty has 2021 being a very tight year on cow supply, with cow prices peaking at 344c/kg liveweight in October-November, before falling to 274c in January next year – again, in response to the big beef turnoff that he predicts will occur in the US in the first quarter of 2021. The strengthening in the US imported grinding beef market, as had been seen in the past two or three weeks, as food service starts to re-emerge, combined with some recovery in beef demand from China, would see the two again ‘fighting over the lean end of the market.’ Good prices would result between now and the October-November high period.

He has cows averaging 252c/kg next year, after averaging 285c/kg this year, due to increased US beef production in 2021. Both represented dramatic improvement since 2019, when cow prices averaged 198c/kg, with this year up 44pc, and next year up 27pc.