STRONG beef and lamb export demand pressure is starting to show up in Australian domestic supermarket shelves, delegates attending last week’s Meat Business Women Conference in Brisbane heard.

Consumer sector analyst Garth Francis from MST Marquee unpacked how the Australian retail environment had been impacted over the past few years since COVID, and how that might affect the red meat industry moving forward.

Garth Francis addresses the Meat Business Women conference in Brisbane

He said while the domestic supermarket sector had seen recent sales growth up 4.2pc this year, under the surface, it wasn’t all roses.

“Beneath that, there has been 2.5pc price inflation, in line with the long-term average, but recent population growth as borders have re-opened after COVID has helped keep supermarket sales up,” he said.

However looking at per capita volumes, the trend was actually down. Similarly, food service was ‘over-indexed’, coming out of COVID, as everybody wanted to dine out again after lock-downs.

While there had been some slowing in overall supermarket inflation, the trend was category dependent, Mr Francis said.

Within the fresh category (including chilled red meat, pork and poultry), a different set of industry dynamics was in play.

While generally, meat protein price inflation in the domestic retail segment over the past five years was slightly lower that the CPI inflation figure, higher inflation in red meat had been driven by beef and lamb export demand, US tariff impact and herd rebuilding, Mr Francis said.

“That strong export demand means that domestic prices have been kept high,” he said.

Click in graphs for a larger view. Click twice to enlarge even further.

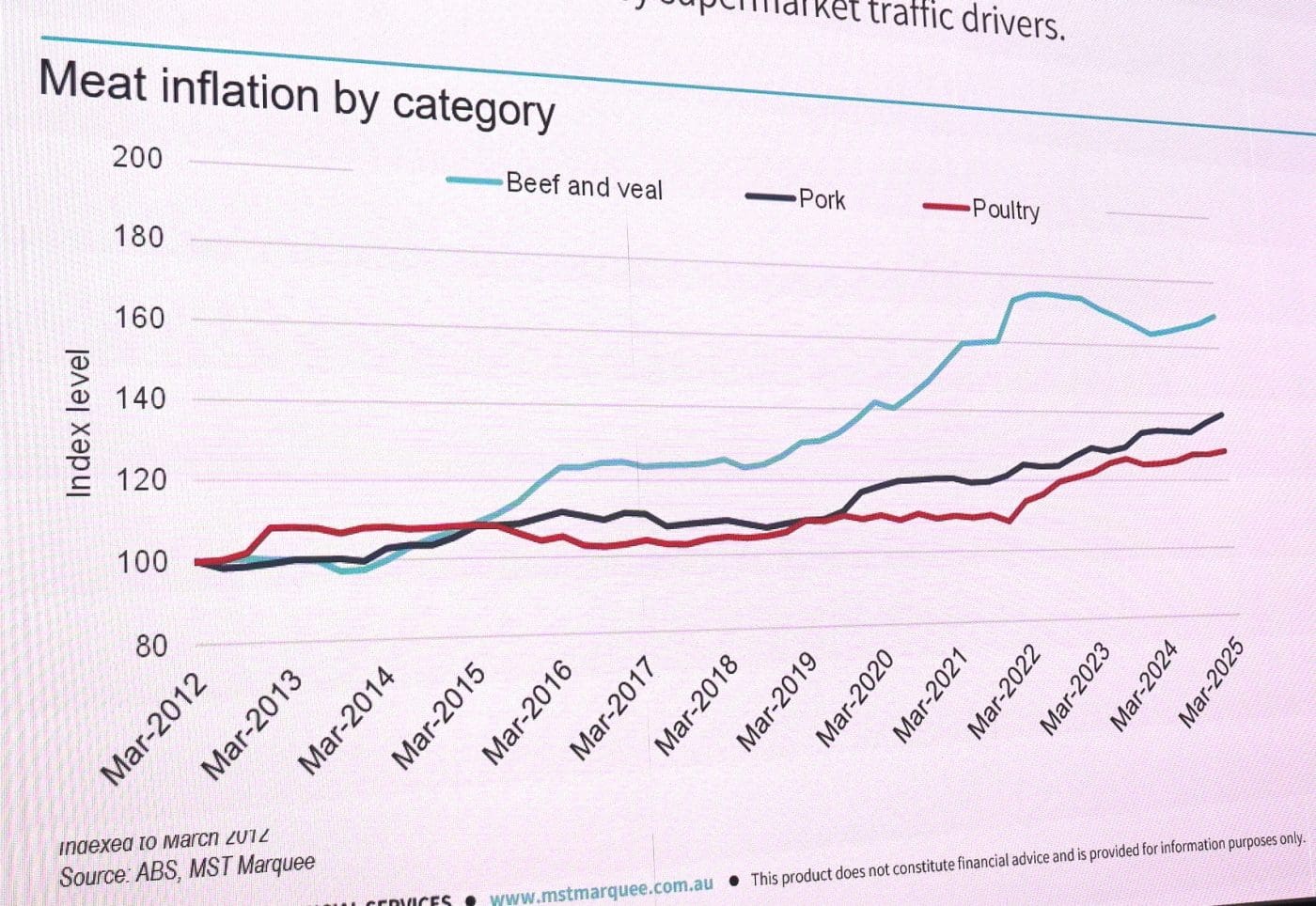

The MST graph published here shows beef and veal price inflation at near record highs in March this year, at an index figure (basis 100 in 2012) of around 170. At the same time poultry and pork prices, neither of which are impacted much by export, showed much lower inflation – pork at an index figure of 140, and chicken at 130.

Red meat foot traffic driver

“But Australian supermarket retailers see meat categories as key customer traffic drivers,” he said.

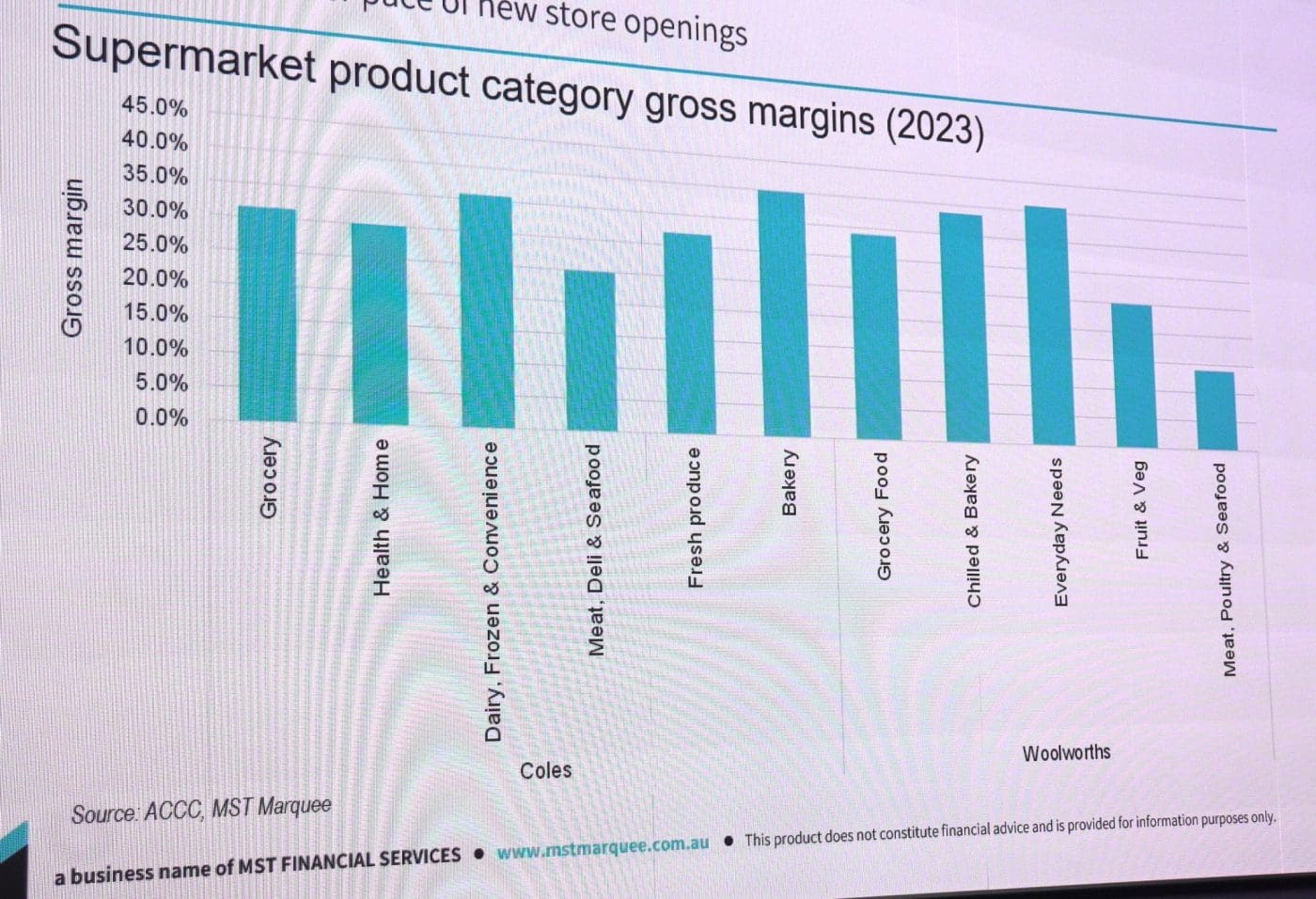

“Fresh meat is a cross-subsidiser of other categories, because it generates fantastic foot-traffic for big retailers,” Mr Francis said.

He illustrated this using the slide below, tracking supermarket gross margins for different product categories. It shows for both Coles (left hand side) and Woolworths (to the right), that the meat, poultry and seafood category had the lowest gross margins of all major food and grocery categories in 2023 trading.

For Coles, the figure was about 25pc (Vs 35pc for dairy, frozen and convenience and 40pc for bakery); and for Woolworths, less than 10pc (Vs 40pc for chilled and bakery, 25pc on fruit and veg).

With Australian beef exports up 16pc in value last financial year and ABARES estimating 12pc growth in the 2025 year, the export market remained more lucrative for both beef and sheepmeat processors, and was likely to keep upwards pressure on domestic prices, Mr Francis said.

“We’ve definitely seen wholesale meat pricing increases recently as a result of export demand pressure,” he told Beef Central after his presentation.

“But when we’ve looked at what’s happened inside the supermarkets (chilled cabinet retail prices) we have not seen that price increase reflected. Our consideration is that the major supermarkets are actually wearing that margin loss.”

Part of that may be the pressure supermarkets have come under since the ACCC and parliamentary inquiries into supermarket practices last year, he said.

“But the other part is that the major retailers realise what a traffic driver fresh meat is to attract customers in-store. For that reason, commercially, it makes sense to keep fresh meat prices lower, to drive foot traffic into stores – especially when other categories are missing out.”

Tipping point?

Asked whether there would be a ‘tipping point’ at some time when pent-up international demand for Australian beef would force major domestic retailers to lift retail prices (and/or margins) on fresh meat, Mr Francis said the domestic market could enter a time where that may have to happen.

Pointing to the recent price discounting campaigns announced by Woolworths, and already responded-to by Aldi and other competitors, he acknowledged that red meat was only very lightly represented among the 400 most recently discounted items.

“It looked like Woolworths was more strategic around private label products for the campaign,” he said. “But just how far this goes, in terms of a potential price discount war, is anybody’s guess at this point.”

Asked whether MST was seeing signs of trading down (out of more expensive steak cuts into beef mince, or from beef into cheaper protein options like chicken/pork) Mr Francis said it was evident, but what was also noticed was changes in the way the supermarket was laid out.

“Chicken has been brought to the front; and beef pushed further back. That’s clearly designed to drive the value perception,” he said.

There were fewer beef specials evident, in favour of chicken and pork in the fresh department.

Retail sales now ‘normalising’

Mr Francis said domestic retail sales suffered in 2024, but were now seeing some normalisation.

“We do see a better year in 2025, than 2024 for retail,” he said.

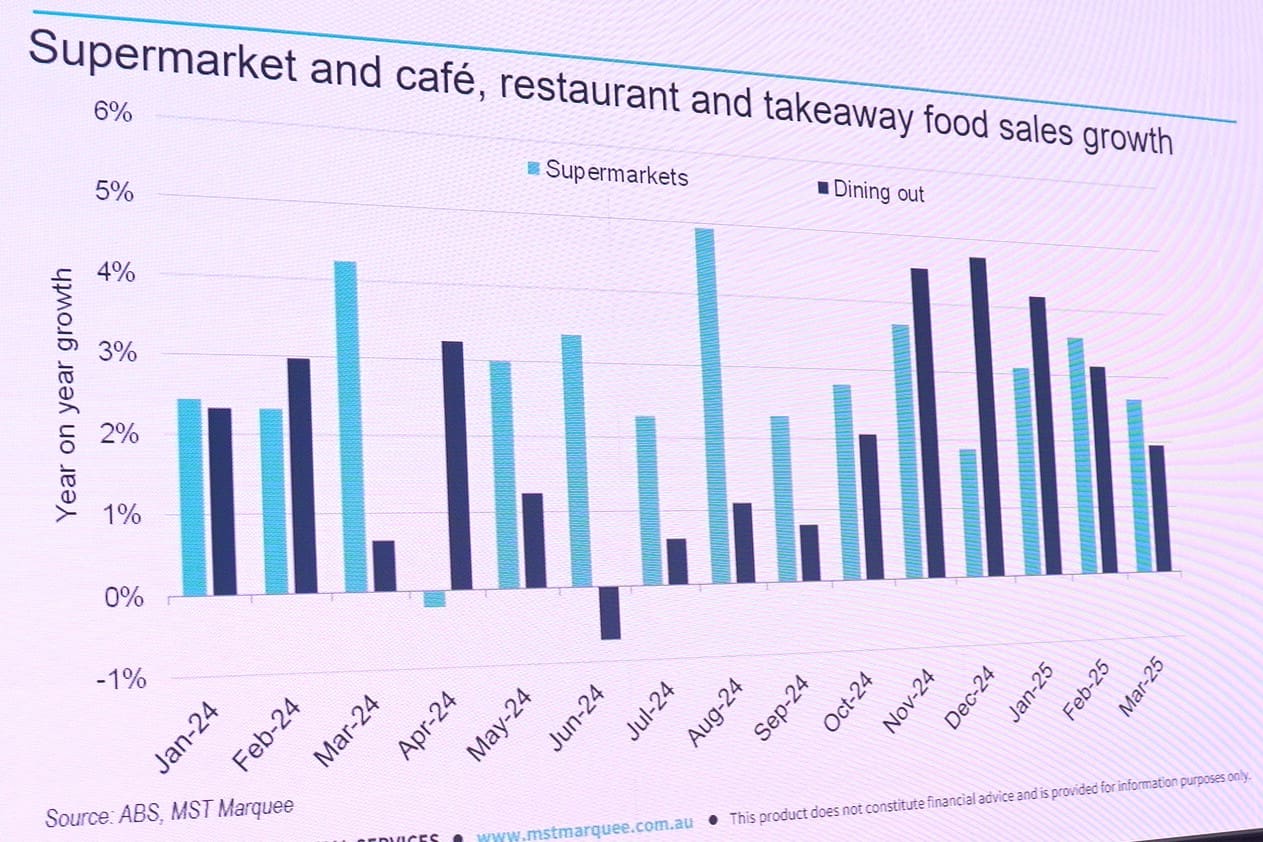

His graph published here showed that both supermarket retail and the dining out segments had done quite well this year, with supermarkets growing at 4.1pc, with dining out 3pc.

“Post COVID, we all jumped back into restaurants and dining out, while we got our takeaway breakfasts at quick service restaurants. Some of that has structurally remained solid, and not got back to pre-COVID levels from a dining out perspective,” Mr Francis said.

In terms of Australian retail sales, most growth rates were 3-4pc prior to COVID, but showed a huge pickup during the COVID period, as consumers were forced to eat at home. But by 2024, retail suffered as consumers travelled and ate out more.

“We are now seeing a period of normalisation in retail, with more typical growth evident. Volumes have also stabilised on most categories, with price inflation likely bottoming out.”

Mr Francis forecast flat growth in retail by December this year, compared with the same period last year. Positives included volume improvement and interest rate cuts, while negatives were lower wage rate growth, a savings lift, population growth slowdown, higher unemployment and inflation easing back.

Most of the wallet shift back to pre-COVID norms had now run its course, he said, however the budget-conscious consumer continued to dominate the market.

“Retailers are still seeing a greater proportion of sales made on discount, and promotional events are seeing large volume spikes.”

Australian householders currently have a savings rate of 3.3pc, below where it has been historically.

“That means the consumer is being a little more careful in how they spend their money. It means they are going for that value product, and will continue to do so for the next couple of years.”

“While we do expect some growth in supermarkets and restaurants, both are facing headwinds from price inflation,” he said.

MST has sales growth for retail food sales next year at 4.4pc, and for the cafes, restaurants and takeaway sector, up 3.7pc.

Online retail activity on the rise

Online retail was also making a comeback, after a post COVID slump.

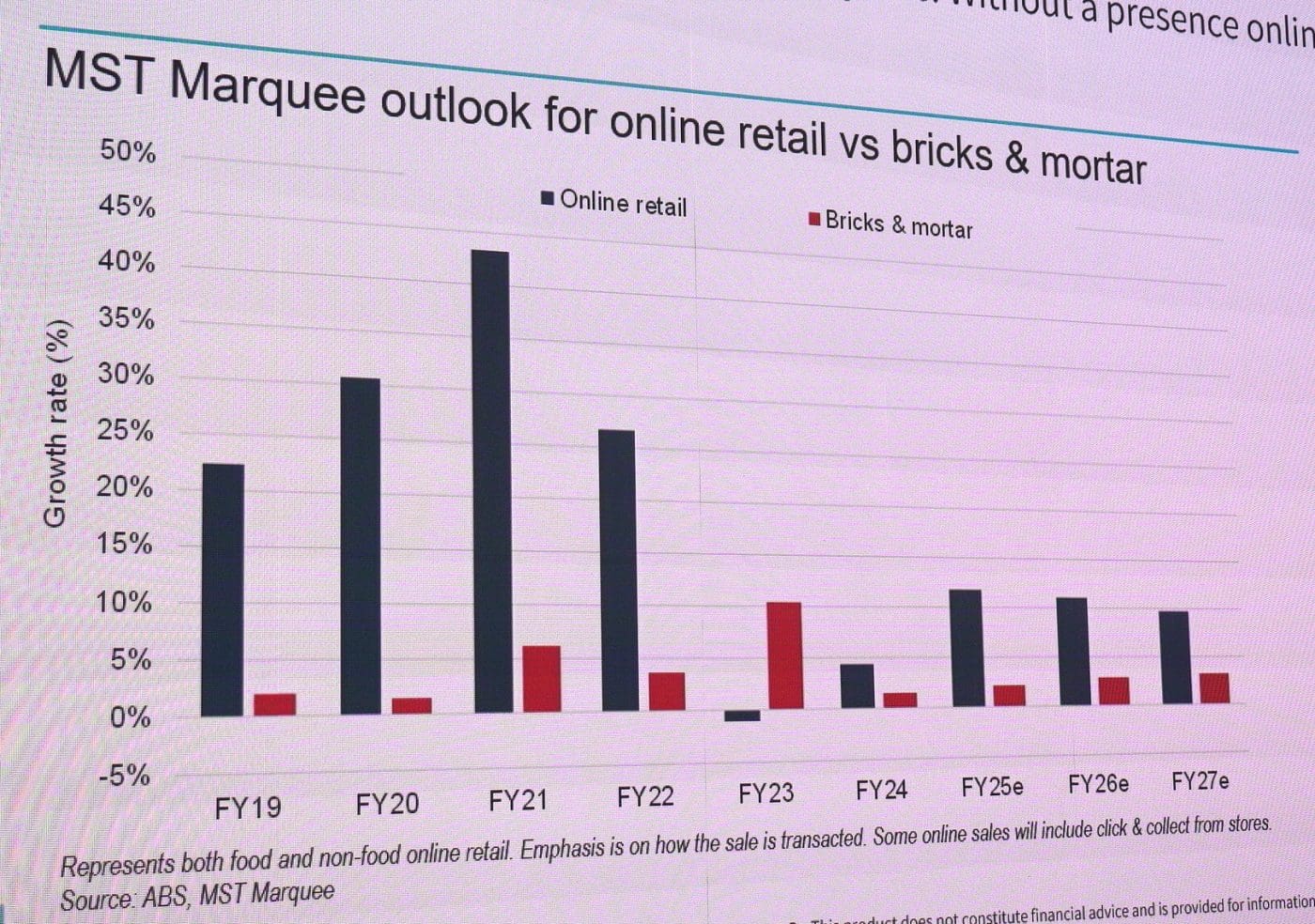

As the graph below shows, online retail growth soared to +40pc in the 2021 financial year, before going into negative territory in 2023, and showing recovery since then. Online spending growth is up 9.9pc for the three months to the end of February this year, and MST anticipates 10-12pc online retail growth in the next few years.

Interest rate cuts were supportive of retail spend, but MST’s expectation for the current rate cut cycle is that it will be a shallower cycle than what’s been seen historically.

“Part of the reason for this is that we have a pretty low starting rate (interest rates wise), at the start of the down cycle, and low unemployment,” Mr Francis said.

Food and supermarket spending tended to be slower to respond to interest rate cuts than other segments.

The US bought 400,000 tonne of beef for $3,000,000,000 USD which equates to AUD $11.86 per kilo

Are Mums and Dads trying to raise a family subsiding the US

Keep in mind that much of Australia’s beef trade into the US is in frozen trimmings (grinding beef), Raymond. On that basis, an average price of $11.86/kg (assuming your figures are correct) does not look too bad. Editor

Great article. BUT what about the pathetically low prices the poor beef farmers are getting. The costs of vet, transport, feed, land maintenance, inflation etc. is not even covered by the price per kg for our live cattle sales. It costs $3.80 to $4.50 per kg just to break even, and that does not cover the full labour costs. Why are the processors and other parties allowed to coordinate the low, low prices at the sale yards?. Why isn’t there a royal commission?. I’ve just bought $21k worth of Lucerne just to keep my 47 cows through winter in NSW Riverina. Work that out and tell me why I should continue to make massive profits for the processors and the retailer’s? Deeply disappointed. Tane

Prices are going to go up cost of cow and lamb have gone up at the farm gate