At some point, the run of improved seasonal conditions and herd rebuilding across Australia was always going to result in greater numbers of heavier cattle and increased supplies of beef.

At some point, the run of improved seasonal conditions and herd rebuilding across Australia was always going to result in greater numbers of heavier cattle and increased supplies of beef.

The big question was how that additional supply would be digested by an export market already under pressure from a high A$ and lacklustre consumer confidence in key importing countries.

In its major annual beef forecast released today, ABARES has put some figures around what it believes the answer will be, and the result can basically be summarised as a general easing trend for beef prices in the short to medium term.

The Government commodity forecaster says the ongoing grass-fuelled herd expansion will translate into higher slaughter rates and increased beef production from next financial year.

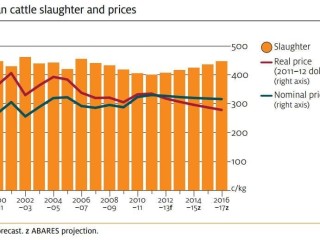

After averaging an expected 330c/kg this financial year due largely to historically low slaughter rates, ABARES expects saleyard prices to ease slightly to average 325c/kg next financial year.

That figure will be propped up by what ABARES expects to be sustained strength in young cattle prices during 2012-13 on the back on continued strong restocker demand, which it bases on an assumption of favourable seasons continuing next year.

However prices for all other categories of cattle are tipped to fall in 2012-13, due to higher slaughter rates and beef production putting downwards pressure on prices, and lower average prices in export markets.

Australia is expected to export more beef in 2012-13 but a greater proportion will be to lower valued frozen beef markets, as it loses ground in key higher-value chilled beef markets to US exports, which are likely to continue to be aided by a lower US lower dollar.

Much also hangs on whether Indonesia decides to increase its annual import quota of 283,000 cattle announced for this year, down from 500,000 head last year.

If it does not, the balance of lighter steers and heifers produced for the trade in northern Australia will need to find alternative markets, and could well end up adding to supply on domestic markets.

The medium term outlook, influenced primarily by expectations of gradually increasing supplies and sustained competition in Japan and Korea, is for saleyard cattle prices to average 275c/kg in real terms in 2016-17.

Cattle numbers will be 5pc higher this financial year to 27.6m head, and will then rise by 4pc next financial year to 28.8m head, before peaking at around 29.1m in 2012-14 – assuming relatively favourable seasonal conditions.

Herd numbers would then decline gradually as slaughter levels increase – “contributing to projected lower saleyard prices in real dollar terms over the medium term”.

Slaughter rates are forecast to fall by 2pc in 2011-12 to 7.9 million head, before increasing to 8.1m head in 2012-13.

Female slaughter is also expected to gradually increase from 2012-13 as producers begin to turn off surplus breeding stock.

Beef and veal production is forecast to rise by 1pc in 2011-12 to 2.1 million tonnes, before increasing by 2pc in 2012-13 to 2.2 million tonnes.

Production levels will be driven higher by a greater proportion of adult males in the total turnoff, resulting in higher average carcase weights.

Production growth will gradually slow as the higher proportion of females and calves returns, and lowers average carcase weights.

Export volumes are forecast to rise by 2pc in 2011-12 to 955,000t, before increasing further to 970,000t in 2012-13.

Japan: Demand for Australian beef is expected to fall as a result of stagnant per person beef consumption, and increasing competition from US beef.

Exports are forecast to fall by 4pc to 338,000t and a further 2pc to 330,000t in 2012-13.

US exports are expected to take an increasing share of the higher-value chilled beef market, which mainly supplies household consumers. Australia's share of the frozen cuts market, which mainly supplies the food service sector, is expected to continue growing.

Australia’s share of grainfed beef imports into Japan fell to 40pc in the first five months of the 2011-12 year, down from 26pc in 2010-11, a result of strong competition from marbled US beef.

Korea: Growth in beef consumption, and reduced supplies of locally produced beef in the wake of the late-2010 FMD outbreak will continue to drive demand for beef from Australian and the US.

Australian beef exports to Korea are forecast to rise by 5pc in 2011-12 to 145,000t , before falling by 2pc in 2012-13 to 142,000t, as competition from US beef increases, aided by a competitive US exchange rate.

Over the medium term Australian exports to Korea will decline as Australia faces greater competition from the US as a result of tariff-reductions facilitated under the recently signed Korea-US Free Trade Agreement, and from Canada, which has recently been approved to recommence exports to Korea for the first time since 2003.

US: High exports of US beef to Japan and Korea and lower supply of domestic beef available to US consumers is expected to drive a small recovery in exports of Australian beef to the market.

The US herd is currently at 90.8 million head, its lowest level since 1958. US import demand for beef is likely to remain relatively high in the next several years as a result.

However, Australia also faces increased competition in the US from Canada, which has lower freight costs, and Mexico, which has lower production costs. Canada’s share of the US beef import market has risen from 30pc to 35pc since 2008-9, while Mexico’s share has increased from 2pc to 8pc.

Australian exports to the US are forecast to rise by 6pc in 2011—12 to 170,000t, and by a further 6pc in 2012-13 to 180,000t.

High US demand for manufacturing beef is expected to provide favourable returns for imported beef in the market.

Emerging markets: Australian exports to emerging markets will increase by 6pc in 2011-12 to 302,000t , and by a further 5pc in 2012-13.

ABARES nominated the main growth areas as the ASEAN markets, due to high income growth and growing demand for beef, and the Middle East, where demand for packaged beef, as opposed to freshly slaughtered beef from live cattle imports, is rising.

Beef exports to emerging markets are expected to account for 35pc of all beef exports by 2016-17, up from 30pc now.

However, average prices will be lower than those in Japan and Korea due to the larger proportion of frozen beef exported.

To view ABARES full outlook for all commodities report click here