This project was undertaken by consultant John Reeve from AgRee, having received funding from the Australian Government’s Future Drought Fund. This item is a reflective thought-piece from the author of the project report.

![]()

THROUGH a Future Drought Fund grant, we were able to model the potential value of transferring livestock price and rainfall (a proxy for volume) risk to the investor/insurance community.

Under our proposed model, a Contingency Interest Factor Loan (CIL) – a tailored construction of commercially-relevant price and rainfall data – would support livestock producers in tough times such as drought and/or disease. But effective commercial benchmarks and awareness are needed.

CIL supports sustainability and the industry’s strategic vision and goals. The main barriers to development and deployment are commercial cattle benchmarks (data) and awareness.

Key questions the project sought to address were:

- What is the potential value and benefits of risk transfer within the context of Australian beef cattle grazing?

- What are the barriers within and external to the supply chain to executing, and how can technology enable this initiative?

- How would greater cashflow stability strengthen the wellbeing and social capital of rural, regional and remote agricultural-dependent communities?

- How may greater beef income and cashflow stability support sustainability/natural capital initiatives in landscapes?

Adversarial supply chain

The history of the Australian beef cattle sector is that of processors downstream and landowners upstream. There is little in the way of industry-accepted commercial price data benchmarks or awareness (mechanisms) to ‘separate pricing and supply’ by agreeing volume commitments but pricing independently via an agreed benchmark.

The industry is described as an ‘adversarial supply chain’ that impacts negatively on risk & drought management and financing. Many reports by the likes of AMPC, MLA, ACCC and NFF have highlighted the lack of price transparency, but culture and vested interests seem to prevent progress – despite the industry being acutely exposed to disease and drought risk.

Better-supported commercial benchmarks would allow for improved co-operation between producer and processor in managing cattle to obtain better ESG, financial and risk management outcomes.

International perspective

Internationally, a lack of price data is resolved by either government mandates or private data firms collecting data.

Interestingly, in the last 12-24 months, Argus Media (a private UK based firm) has hired staff in Dalby to collect key commercial feeder steer data from willing participants. Argus owns this valuable data and reportedly now need to start charging for access.

Other jurisdictions where Argus Media step-in like this include the Black Sea, China and Brazil; so it seems irregular for this to be needed in an industry with the resources of the Australian beef cattle industry.

In the US, the Federal Government mandates relevant price reporting, no questions are asked.

Another thought is that – major multi-national corporations and their tax advisors, have more latitude to exploit opaque commodity markets via practices such as Transfer Pricing and other tax tricks that are finally now being more actively investigated by government and the media in Australia.

Increasing volatility

As the industry is well aware this year, volatility is increasing – both climate and price risk – so the need to have data benchmarks that enable risk transfer is more important than ever in this context.

Lumpy Skin Disease lurks just off our borders and our beef industry is dependent on export markets for 70pc of its production.

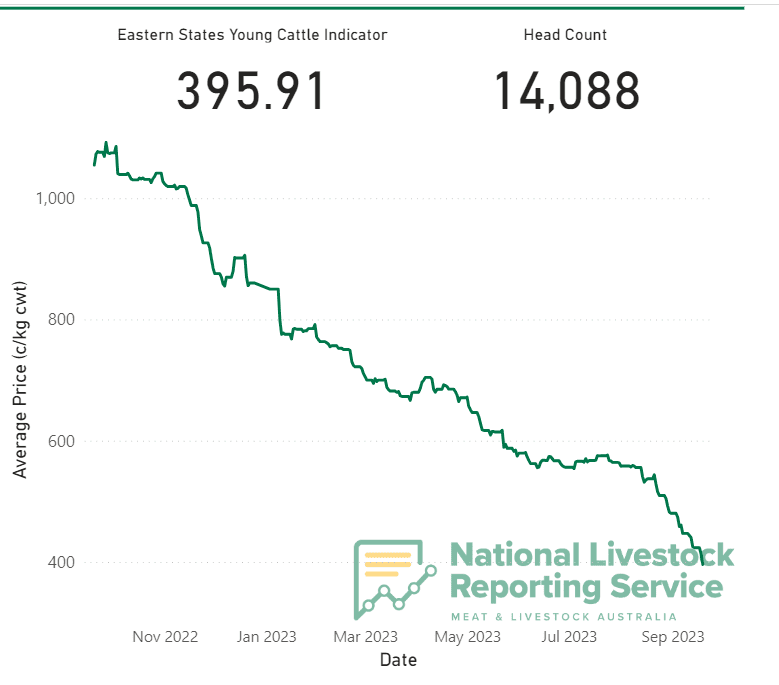

Our domestic market is too small to absorb any significant expansion in supply, even if we wanted to. The below EYCI chart illustrates how cattle prices have halved in the last year, with more downside pressure from a confirmed El Nino climate pattern and, god forbid, a disease outbreak.

Source: MLA, 19 September 2023

Looming climate risk reporting mandates and trade

Imminent Australian Government mandates, starting July 2024, relating to emissions and climate risk disclosure will bring transparency to the climate/emissions in Australia.

Similarly, the Australian Government has announced that Australia may impose a carbon boarder adjustment mechanism (CBAM). It would be constructive to also have cattle price risk transparency addressed at the same time, given the ecological scale, financial vulnerability and human labour dependency of the sector – that would all benefit from a more coordinated supply chain.

“Future focused customers and investors, domestic and international, are increasingly using ESG analysis, including carbon, as part of their decision making. Price transparency of agri produce is therefore important to measure and report embedded carbon values within underlying agri products and other future ESG metrics. Consumers also expressed that price stability is as important as price itself when considering supply partners.” USQ & NFF On-Farm Risk Report[1], Page 7.

Of course, genuinely vertically integrated supply chains have less of a need for such cattle price data and transparency, but most cattle change ownership title at some stage, and most of this data is not made public.

Model grazier case study description

The data set used to prepare the preliminary case study is taken from a ‘typical’ Australian grazing family based in one of Queensland’s prominent grazing regions. Typical of many of their peers, the family is in an ongoing transition of ownership and succession from the elder generation (late 70s) to the younger operating couple (mid 50s). During this process additional debt has been required to meet the retirement needs of the parents and additionally siblings.

The underlying operating business has not fundamentally changed to facilitate the additional borrowings. Whilst technically from a bank credit risk perspective, their equity levels would be considered ‘sound’ or ‘appropriate’, the succeeding couple recognise the additional risk borne by adding debt.

Such risk (droughts, livestock prices etc) are, to an extent, unable to be mitigated. The commonality of this scenario is evident across the Australian agricultural landscape, including outside the cattle sector.

Ultimately, at a time where they have the human capacity too, this family has the ability to grow their grazing business should risk be able to be controlled.

The correlation in this model strongly exhibits the impact of seasonal conditions on livestock turnoff volumes and prices – major drivers of economic, social and environmental sustainability.

The Contingency Interest Factor Loan (CIL) product endeavours to reduce the risk of such succession, start-up or growth events in Australian farming enterprises – starting with the cattle sector due to its size and vulnerability. Thereafter driving a more resilient future for Australian agriculture.

We have explored the application of this initiative in similar sized grazing operations in New South Wales and Victoria and believe there is a similar benefit in these markets.

This type of risk management strategy may be particularly useful for small and medium-sized cattle enterprises that may be more vulnerable to economic, social, and environmental risks.

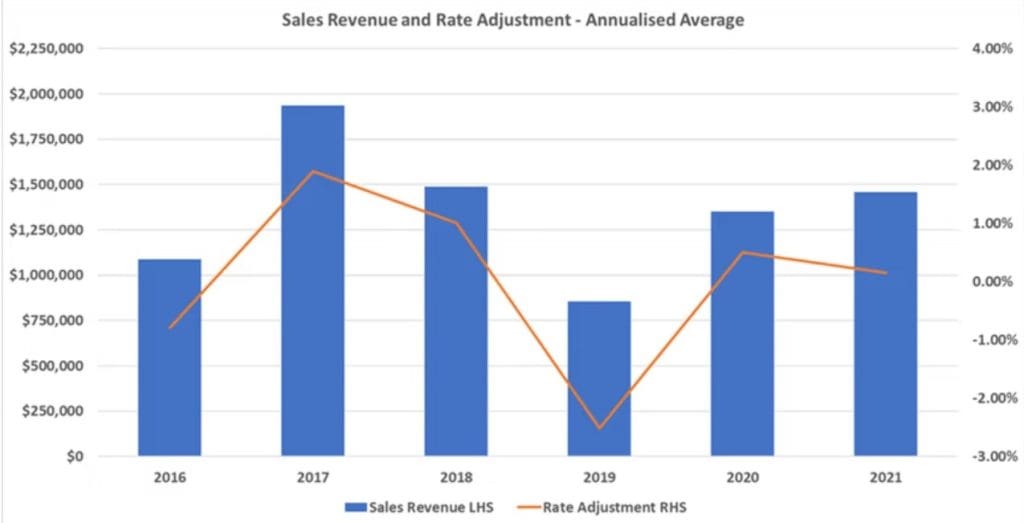

Pricing model description

The graph compares the CIL interest rate adjustment percentage to sales revenue. As can be seen, in worse revenue earning years the rate is decreased to alleviate cashflow pressure on the business.

The effectiveness of the cashflow hedge solution can be checked by two methods:

Comparing the performance of the hedge to the performance of the risk it is meant to protect against. For example, the contingency interest loan is linked to a standard precipitation index and steer pricing data, so the movements in these indices to the changes in the loan’s (adjustment factor) value over time will be compared. If the loan’s (CIL Factor) value moves in the opposite direction of the indices, it may indicate that the hedge is working as intended.

SPI correlation is 95pc, Steer correlation is 87pc. Both are well within the (80)~(125)pc hedge effectiveness requirement (CME Group, 2022).

Calculating the hedge’s contribution to the overall performance of the business. By comparing the business’s financial performance with and without the hedge in place, it can be determined if the business performs better with the hedge in place which may be an indication that the hedge is providing some level of protection against risk. This will require building an enterprise model for the business to estimate revenues and borrowing costs with and without the CIL (future recommendation).

Recommendations

- Survey relevant government, financiers/banks, producers and processors as to their willingness to support CIL and the recommendations in this report

- Financial literacy and improved risk management awareness – with pre and post measures that link to improved business risk management and potentially on farm performance

- Cattle price data – engage independent commercially experienced subject matter expert e.g. review the recent DAWE Workshop on Price Transparency

- ‘Close-out’ mechanisms need to be discussed with producers and buyers of their cattle to ensure the timing of the cattle price element of the CIL and physical cattle sales are better aligned

- Who owns the CIL product (government or private sector etc), sponsors to move forward – DAWE officers overseeing RIC products may be best placed with commercial partners such at Stable, supported by BoM and reputable cattle price data providers (MLA, Argus, Auctions Plus etc).

- Individual Business Integrated Climate, Risk and Accounting Model (Applied Climate + Commodity and Financial Risk + Financial/Accounting Model) – to predict, identify and model risks to better support risk planning and product innovation

- The four recommendations in the Pricing Model Description section (above) for further model development

- Developing template / visualisation and risk reporting tools to help rapid risk diagnostic assessment and recommend a tailored CIL factor

- Work with accountants to normalise financials back many years to allow for back testing/gamification and product testing

- Ability to scenario and back-test climate events (historical, hypothetical and forecast), existing & new tools and strategies to manage risk

- Potentially delivered online to allow for simulation/gamification.

About the author:

John Reeve grew up in the Arcadia Valley and Darling Downs in and around grazing, lotfeeding and branded beef exports. In his professional career he pioneered long-dated agri hedging in Australia at Rabobank and CBA, then went on to build out agri income stream hedge platforms globally via the franchises of UBS, Standard Chartered and Goldman Sachs. AgRee has most recently consulted to RDCs, including MLA & AMPC, NFF, Australian (DFAT & DAFF) and State Government departments (QDAF), global engineering firms (KBR & Jacobs), startups and global commodity trade houses.