The outlook for the Australian beef and cattle industry for the remainder of 2011 has been downgraded from the bright set of opportunities that lifted cattle and beef markets to all-time highs throughout early 2011, in MLA’s half-yearly industry projections document released just minutes ago.

The outlook for the Australian beef and cattle industry for the remainder of 2011 has been downgraded from the bright set of opportunities that lifted cattle and beef markets to all-time highs throughout early 2011, in MLA’s half-yearly industry projections document released just minutes ago.

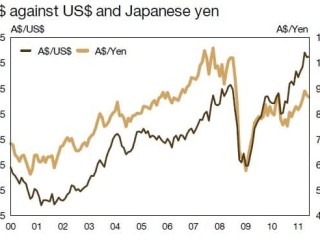

A very high A$, contraction in global beef prices, increased competition from US beef in North Asia and weak returns from the Japan market have all contributed to a more subdued outlook for the remainder of 2011. Added to these issues is the uncertainty that will continue to plague Australia’s live cattle trade.

“However the same global market fundamentals that buoyed beef markets during the first quarter of 2011 have not vanished – they have just been eclipsed by another round of global economic concerns,” projections author Tim McRae says.

“Global beef cattle herds continue to liquidate, especially in major exporting nations like the US, Argentina and New Zealand, while the amount of beef exiting Brazil has been curtailed by a robust domestic market,” he said.

On the demand front, while global beef demand and prices are expected to maintain their upwards trend, increased volatility is also anticipated, framed by the continuing concerns around economic conditions in advanced nations. The fact that there are major economic and consumer concerns in the US, Japan and Europe accentuates the impact on the beef trade – as they are all major importing beef markets.

Reflecting on the fallout from the Global Financial Crisis in 2008-09, global beef prices and demand retreated, as consumers in major importing markets, including Japan, the US and Europe, all ‘traded down’ in meat preferences, favouring lower priced meals and cuts.

“Given the renewed global economic concerns in mid-2011, there is the real possibility of this occurring again over the short term, given the extent of the economic issues facing many advanced nations,” Mr McRae said.

One of the main positives that will continue to underpin confidence across the Australian beef and cattle industry in the second half of 2011, and possibly well into 2012, is the much better seasonal conditions. Flooding and unseasonably heavy rain continued into autumn 2011 in some regions, making it almost 18 months of above average falls.

While creating some major logistical issues for the movement of livestock in 2011, the past twelve months have been the wettest and most welcome in many decades for many producers, enabling some longer-term decisions to be made regarding herd rebuilding. However southern WA is the exception to this, with recent falls hopefully the start to a run of better years.

-

More detail, analysis of MLA’s Half-Year Projections on Beef Central later today.