AUSTRALIAN beef and sheepmeat is far less exposed to a narrow basket of international markets than other Australian ag commodities, or indeed, competing red meat export industries overseas.

That was one of the points to emerge from a marketing webinar held this afternoon by Meat & Livestock Australia, under a series built around the concept of industry resilience.

General manager of international markets Andrew Cox said from a markets perspective, resilience was defined by focusing on the customer and the consumer – competition from end-users, including retailers, food serviced operators and consumers – for available beef, lamb and goatmeat that drives meat and livestock prices.

“Without the money that is coming into the top of the funnel from these people, our industry doesn’t exist,” he said.

Mr Cox said one simple way to measure resilience was determining how much competition we have for our product.

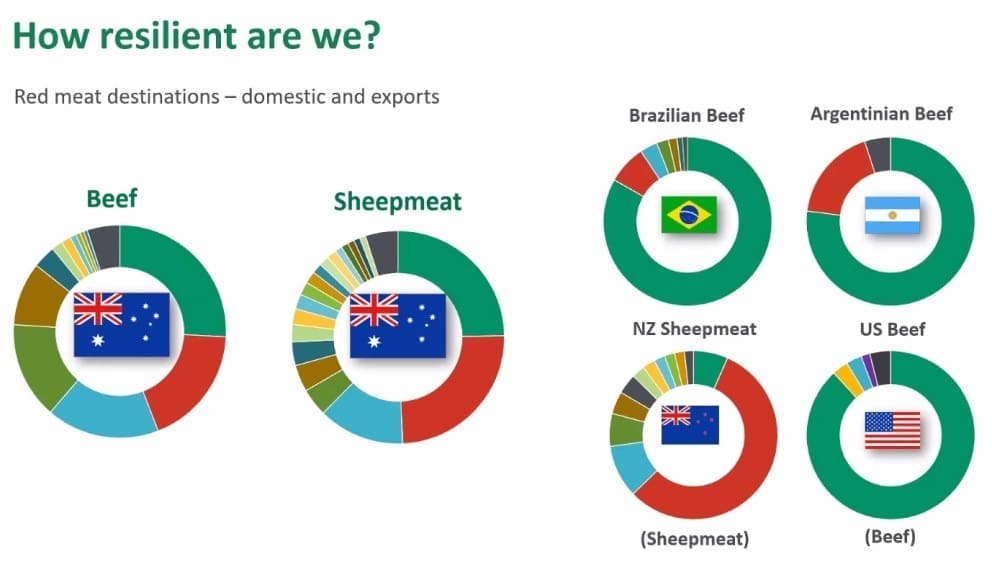

On the graphic below, Australian beef and sheepmeat export destinations and break-up are compared to other Australian export commodities, including barley, wool, cotton, wine and iron ore.

Click on images for a larger view

“Taking sheepmeat as an example, there are 19 export destinations that together account for 95pc of Australian exports. Sure there is a large market share for sheepmeat in China (marked in red on the circle), but there are a host of other markets across the world, from the Middle East to Asia and elsewhere. It’s a diversified wagon-wheel,” Mr Cox said.

“Beef is somewhat similar, with 12 export destinations accounting for 95pc of exports – with the top three (US, Japan, China) all very close in terms of size. With a host of smaller markets, it means we have great diversification in beef exports.”

This contrasts with the commodities represented on the right-hand side of the graphic, which are all much more reliant on a single market – China. Iron ore relies on just three export customers for 95pc of its exports, with barley, five, and cotton/wool, six each.

“Their wagon-wheels are a lot less diversified,” Mr Cox said. “Arguably that opens up a lot more reliance on a single market – therefore, higher risk.”

He said one of the great benefits for Australian beef and sheepmeat exports was that they had been able to grow markets across the world consistently, and diversify the export mix, for decades.

In a second comparison, Mr Cox compared Australian beef and sheepmeat (this time including domestic sales marked in green, as well as exports), with other major exporting nations including Brazilian, Argentinean and US beef, and NZ sheepmeat, in terms of market concentration/diversification.

“In those three major beef exporting nations, they have a strong reliance firstly on their domestic market (green), which obviously exposes them to political and economic risk within that market. But even when you look at these countries’ export markets, they tend to be much less diversified than Australian beef. Both Argentina and Brazil have a heavy reliance on China (red).”

In sheepmeat comparisons, NZ has a similar diversified market spread as Australia, but without a large domestic market at its disposal.

“Under a classic definition of resilience, Australian red meat actually looks quite good, in terms of market diversification, with less risk on a single market,” Mr Cox said.

Similar principles applied to customer diversification. No one customer had the ability to dictate to our industry, so on this measure of resilience, we looked quite good, he said.

He suggested there were four factors the Australian red meat industry had to look at, in building future industry resilience in the international market space.

The first was consumers and competition.

“We really need to make sure we understand consumers globally, but we also need to look closely at our competitors. Pork and chicken, for example, remain very popular globally, and both industries have the ability to increase production rapidly, efficiently and cheaply if the market demands it. We need to make sure we are well positioned against those products, and understand what our benefit and proposition for purchase are.”

The second was trade influences.

“It’s something we have no direct control over, but of course we need to make sure we are continually monitoring the trade dynamic and are aware of it. As an industry we’re always advocating for free and fair trade – open access to markets and consumers globally. We’ve had tremendous success with that over the past decade, but of course the future remains somewhat unclear in certain markets, and we need to make sure that we are together, as an industry, in advocating for access to these markets,” Mr Cox said.

The third factor was the economy, and economic influences.

“Even before COVID set in in March, the global economy appeared to be slowing down, but obviously the pandemic has now brought whole sectors of the economy to a halt. For us, that means customers who are exposed to events, like hospitality and tourism, are struggling badly, but also many consumers globally have less money in their pocket and are worried about their financial security. When it comes to resilience, we know Australian beef and lamb is not the cheapest product – so if consumers are looking to save pennies they might drop imported beef. So we need to make sure we continue to demonstrate the equity that we have in our brand, why our products are worth paying more for, and helping customers make money from our products via education over use of alternate cuts or novel techniques.”

The fourth factor was about resilience in supply.

“Resilience in our supply is also of vital importance to international customers, who want consistent access to a product. We need to make sure that we have resilience in terms of our systems, and are always focussed on providing a high quality item into international markets.”

Mr Cox said once information was gathered on what would dictate future resilience, the industry needed to know what to do with that information.

An example was the emerging middle class in Asia, which has driven our industry for the past couple of decades, and will continue to do so – and not just in Japan, Korea and China, but Indonesia, Malaysia, Thailand, Vietnam and the Philippines.

“We need to understand those consumers, what makes them tick, and how our product might fit into their lives,” Mr Cox said.

There was also a need to look at global trends that were influencing consumer purchasing.

“An example is the huge explosion that’s occurred over the past few years in Japanese and Korean barbecue restaurants across Asia, and globally. That’s actually become a wonderful driver of Australian beef and lamb exports, so we need to understand consumers, and what makes them tick.”

Understanding technology was also important. Marketers needed to be aware of technology trends, and how this was engaging with customers. MLA had recently used the Tic-Tok social media platform to engage with consumers, for example, and had recently run digital trade seminars with overseas customers, to continue to engage and communicate with customers while travel restrictions were in place.

Signs of COVID recovery delivers ‘great platform’ for domestic market in 2021

In a separate address in today’s webinar, MLA’s recently-appointed general manager for marketing and insights, Nathan Low, said 2020 had been a ‘year like no other’ for consumers in the face of the COVID pandemic, which had dominated over the past six to eight months.

“COVID has definitely changed us all, and changed consumer mindset,” Mr Low said.

“Prior to the pandemic, top of mind was always the economy – whether that be house prices or interest rates. Now, our minds are very much dominated by thoughts related to health care, whether that be COVID directly, or simply health and wellbeing and living healthy lifestyles.

“Health is now very much top of mind. Economic concerns now tend to relate to unemployment and what that means for long-term economic recovery.”

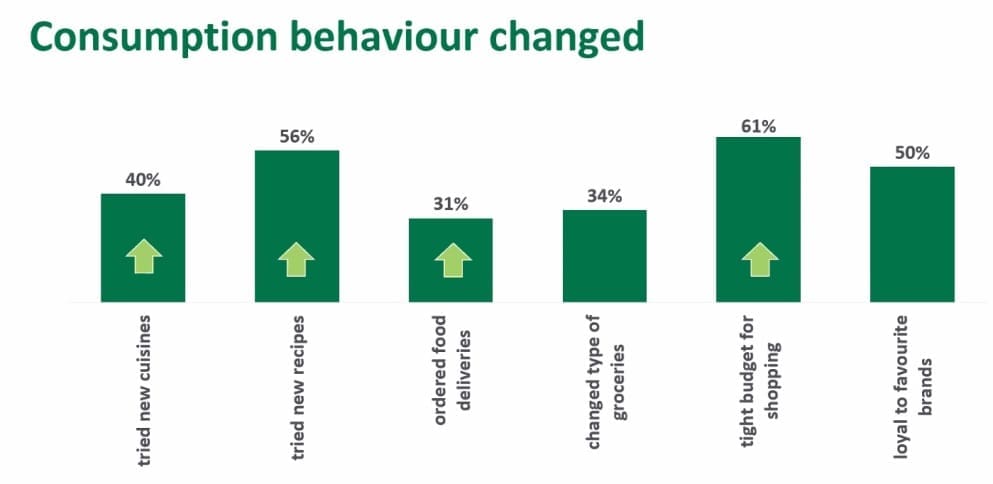

As people spent a lot more time at home, through lockdown and travel restrictions and border closures, consumption behaviour had changed, Mr Low said.

“Spending more time at home, consumers were looking for ways to entertain themselves. Within the food categories, that means consumers were trying more new cuisines than ever before, trying new recipes, and the use of online ordering and delivery went up significantly, with many people trying it for the first time (see graph).

“But equally, consumers’ mindsets was around belt-tightening, with budgets during shopping,” Mr Low said.

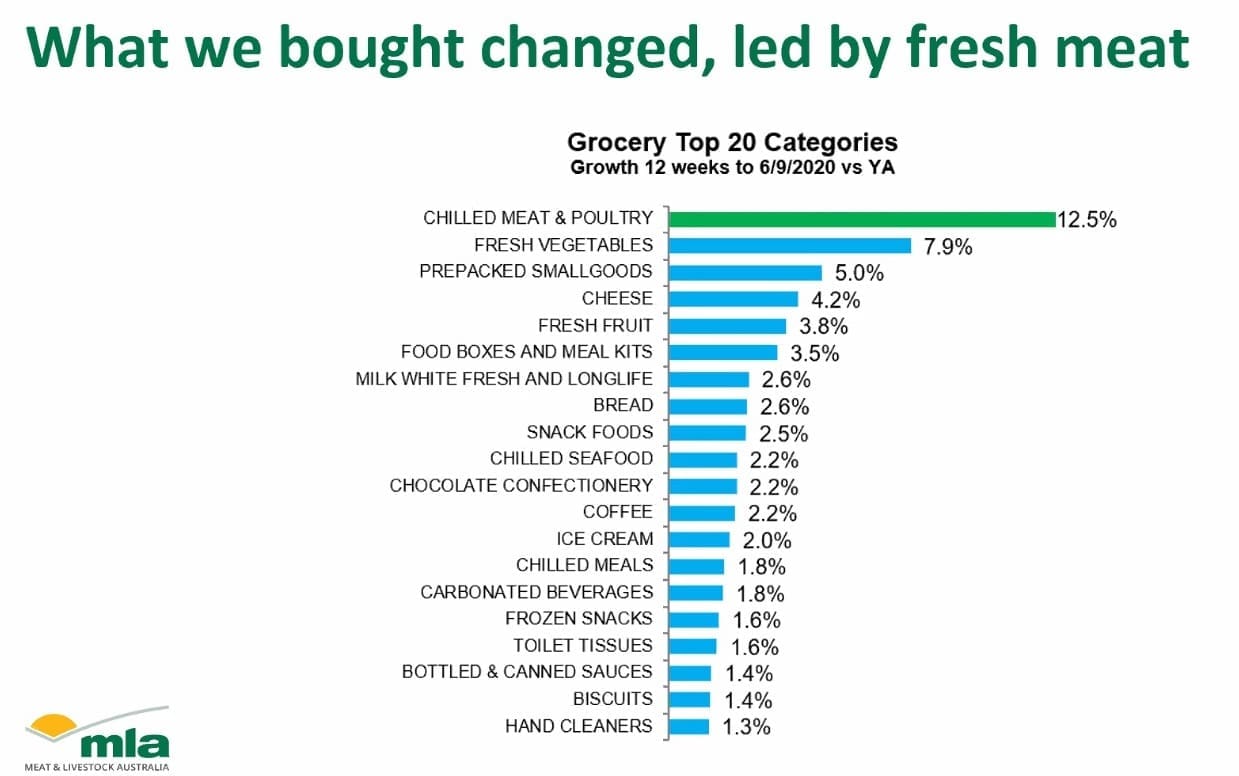

“What we bought also changed. For the 12 weeks to early September (post the initial panic buying phase), quite remarkably, fresh meat was the fastest growing category at retail – significantly higher than all other segments in the supermarket. That’s even more impressive, and cannot be under-estimated, because we are also the biggest category in the retail space. Invariably, the bigger you are, the harder it is to grow faster than smaller categories. That’s a vote of confidence in the fresh meat category, and the role it plays in a healthy diet, in that they voted with their wallets when they did their shopping.”

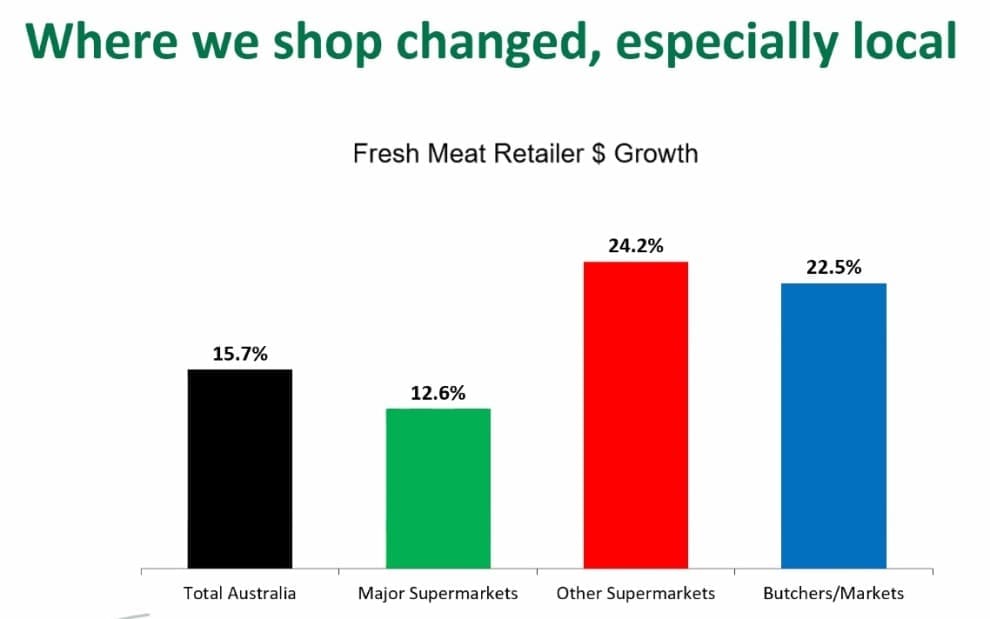

“Where we shopped did change, though, as a result of COVID. Total retail sales for fresh meat showed double digit growth, but consumers actually shopped local a lot more.

“Local IGA’s and independents out-performed the majors in Coles and Woolies. And the trusty local butcher – a channel that’s been declining for a number of years on fresh meat sales, actually saw really significant growth, above 20pc, as people became increasingly concerned about supporting local businesses, as well as looking for environments that held a lot of ‘trust and information’.”

Total food service sales (restaurants hotels and cafes) was significantly down, however, but within the greater food service sector, online delivery did increase significantly, rising 12pc. It is now a segment of the industry worth $750 million annually.

As a consequence of the consumer changes outlined above, MLA had shifted its marketing emphasis – especially as a chunk of the 2020 campaign was geared around the postponed Tokyo Olympics, Mr Low said.

“We had a strong opportunity to tap into that home-cooking trend. We leveraged the number one rating TV show, Masterchef, which gained even higher ratings than usual, because more people were at home, watching TV. We gave them an education about new and innovative ways with affordable beef cuts to use in their increased home cooking repertoire.”

MLA also used the ‘star power’ of TV host Jessica Rowe to showcase and elevate the trusty local butcher as a convenient source of red meat, expertise and cooking tips, driving the advocacy of beef and lamb’s quality credentials to consumers.

Demand, prices rise

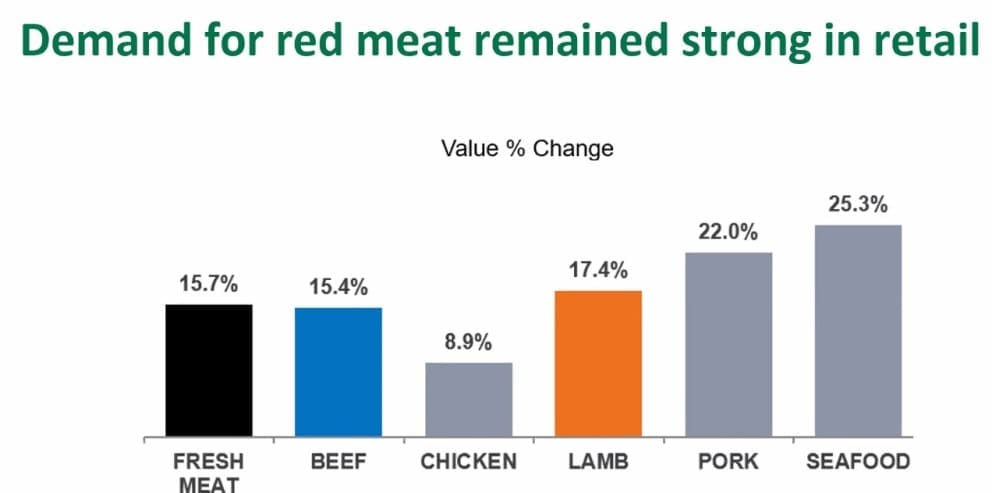

As a result, with everything that was happening under COVID, demand for red meat remained incredibly strong in retail, with beef (blue line) growing in line with the total category (black line), and lamb (orange) growing slightly faster.

“Interestingly, people were not so excited to be eating chicken during COVID – so relatively, a great result for beef and lamb,” Mr Low said.

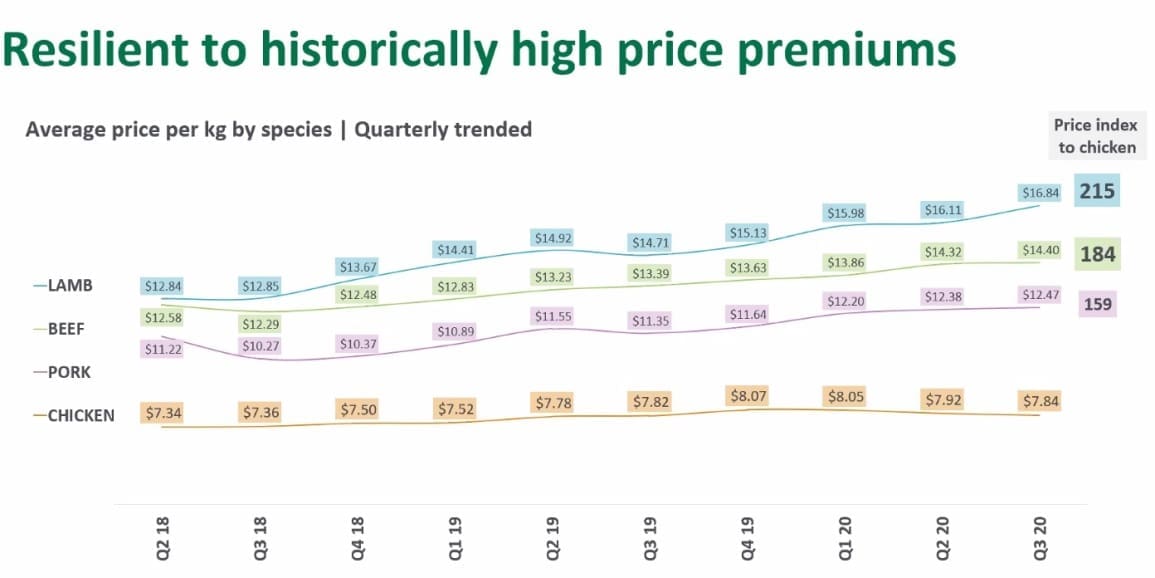

Even more remarkable, given the historic higher price premiums for beef and lamb over other proteins within the retail channel, has been price performance. Chicken since COVID has remained relatively stable, while lamb and beef have recorded growing premiums this year, with demand remaining strong, despite higher ‘budget consciousness.’

“That’s a further vote of confidence in red meat and show the resilience in the marketplace,” Mr Low said.

“Those results meant red meat held and grew market share this year. Beef has remained sold at a 36pc share of retail fresh meat sales, while lamb grew slightly to 12pc,” he said.

Positive outlook for 2021

Mr Low said as the industry stated to look to 2021, the economy was already starting to improve, with the expectation that by the end of next year, the Australian economy will be almost back to pre-COVID levels.

“In certain states, economies have already started to recover. Retail spending is up, across the board in Australia. It’s really only been the impact of prolonged lockdowns in Victoria that has subdued some of the growth in retail environments,” Mr Low said.

Despite the impact of prolonged closures in Victoria, retail spending in cafes and restaurants is already back to 80pc of what it was pre-COVID.

“As borders start to open, Victoria starts to normalise, business and holiday travel starts to resume, we will see continued growth and recovery in the food service channel,” he said.

Despite all this, Australian consumers were ‘forever changed’ by the COVID experience, Mr Low said.

“Health and wellbeing is very much at the forefront of peoples’ minds, which presents great opportunities to showcase the role that red meat plays in a healthy and balanced diet.

“Importantly, consumers are also much more considerate about empathy and inclusion, and they are looking for marketers and brands to reflect that.”

“As we move into 2021, consumers are looking for us to come together a lot more than we have, and that is an opportunity for brands to showcase some of the great Australian values that we all know and love, which make us proud to be Australian.”

A Christmas “like no other”

Given the sense of isolation that has occurred, Christmas 2020 was likely to be a “Christmas like no other,” Mr Low said, as many families come together around a dining table for the first time in a ‘very, very long time.’

“It’s an opportunity for marketers and brands to tap into that sense of togetherness that people are looking for – and MLA’s upcoming marketing campaigns tap into that sentiment, in one way or another,” he said.