Simon Quilty

Independent analyst Simon Quilty weighs-up the drought and flood challenges currently facing the Australian beef industry with other variables such as changing global meat prices, high feed prices and an unpredictable A$ to try to predict Australian cattle and meat prices during 2019.

NEVER in 30 years of meat trading and analysis have I seen so much uncertainty and challenges faced by all sectors of the meat and livestock industry. From extreme drought in southern QLD, NSW and VIC to record-breaking rain and floods in northern QLD, it is a truly challenging time as the producers try to come to terms with losses. I sincerely wish them well.

Below, I have tried to outline what these challenges, along with other variables such as changing global meat prices, high feed prices and an unpredictable Australian dollar will potentially have on individual enterprises – in particular to try and objectively assess what impact these extreme events could have on Australian cattle and meat prices during 2019.

My analysis can be best summed up by outlining what I believe is the ‘good news’ and the ‘bad news’ for 2019.

The good news

The first good news is that global beef prices in 2019 are expected to be four percent higher than 2018, on the back of continued growth in the Asian middle-class and the likely protein shortage caused by African Swine Fever in China. ASF is expected to spread into other regions of Asia and there is potential for mass liquidation of the hog herd in China and other Asian regions. In addition we are seeing Asian consumers moving away from pork to beef and chicken.

Australian cattle prices I believe will bottom (and may move sideways for 2-3 weeks) this month and then improve for the remainder of the year – with or without rain. The herd liquidation that has occurred due to drought and recent flood losses in northern QLD has seen national cattle numbers drop to a critical level. I subscribe to the theory that ‘you can only kill them once’, and the result I believe is less cattle numbers coming forward with or without rain for the balance of 2019 (read below).

The long-term trends of an above normal rainfall year in 2019 is starting to unfold and is looking more likely (see graphs below). This is not unusual after a critical dry year like 2018 with localised rain events starting to occur, particularly in northern QLD. If history should repeat itself, it would see a regular wet winter return to southern Australia with an exceptionally wet monsoon period in late 2019 and early 2020 for northern NSW and QLD.

Should history repeat itself and 2019 evolves into a wet year, then steer prices could improve by 12-20pc on average across the eastern seaboard and depending on the region, cattle type and genetics could see some cow prices improve by 20-50pc.

The bad news

The bad news is the unfortunate loss of livestock in recent weeks due to flooding in northern Australia has acerbated the liquidation of the Australian herd in a way that is deeply concerning.

The losses in northern Australia have been across all breeds, male or female, and all genetics both good and bad – flood loss is non-discriminatory and as a result the ability for northern producers to rebuild is going to be very difficult.

In comparison their southern neighbours in drought will also find it difficult to rebuild and have been desperately trying to hold on to quality breeding animals to ensure the best chance of recovering when the drought breaks. The flood victims unfortunately have now had this unenviable choice taken away, as much of the worst affected region was breeding country.

Elsewhere on the bad news side of the ledger, grain and fodder prices are expected to remain high for most of the year, with or without rain, due the timing of the growing season and the severe lack of grain and fodder at the moment.

The flooding in northern QLD and the desperate need for fodder will undoubtedly see a short-term tightening of fodder supplies as emergency rations are distributed. The benefits of these rains in the north may not materialise for another 6-8 weeks until the land has had time to dry out. During this period fodder prices could move higher and as northern pastures improve, the pressure on buying fodder will get less but none the less higher fodder prices are expected to last until October this year.

A survey of financial market analysts has predicted that the Australian dollar will rise between now and the end of the year. This would normally be negative on cattle prices, particularly in an over-supply market whereby participants in the supply chain are always reluctant to give up any commercial gains should the A$ fall.

But in a tight supply market (which is what we may soon see) the positive benefits of currency are normally passed back, and should there be a rising A$, the disadvantage of this in a tight supply market are often absorbed by supply chain participants as they are desperate to buy meat and or cattle. This was the case in 2016 (as explained below). Without rain and ongoing cattle supply, the predicted rise in the A$ is likely to be passed back to farmers.

The five key areas of risk I have looked at in greater detail are as follows:

- Drought – what are the consequences if drought breaks and/or it doesn’t this year?

- Feed/grain prices – will these remain high?

- Cattle prices – are they likely to go higher or lower?

- Global meat prices – are global meat prices likely to get stronger or weaken and what will be the impact on Australian cattle/lamb prices?

- Australian dollar – will this go higher or lower and what is the likely impact on livestock prices?

I believe that with any enterprise and the hard decisions made at critical points in all production cycles, the best person to understand your risk is yourself and part of the evaluation process is doing good research on all the scenarios that could affect your operation. I would encourage all readers to seek professional advice on all the matters outlined in this paper before making any commercial decisions.

Drought in Australia – where are we at?

This is the most difficult question in today’s market for any livestock producer, lotfeeder or meat processor in Australia, and the answer to this question will vary from region to region.

Last week Australia’s Bureau of Meteorology released its monthly drought statement and revised forecasts. In brief they described 2018 rainfall as exceptionally low over the southeastern quarter of the mainland with many regions in the lowest 10pc on record. Interestingly, the annual rainfall for the Murray Darling Basin was the seventh lowest on record (since 1900).

The February to April 2019 BOM outlook indicates a drier than average three months is likely for western and southern Australia and parts of the northeast. In this same period the expectation is for warmer than average temperatures for both days and nights. BOM’s report spells out clearly that there is now an elevated chance (50pc) of an El Nino event developing during 2019 which typically results in warmer and drier than usual conditions and a late Autumn break in southern and eastern Australia.

Independent forecasters’ views

Ex CSIRO meteorologist Peter Nelson, (based in Victoria and retired) is forecasting 2019 to be a wet year for outback QLD, NSW, VIC and TAS. His views are based on an 80-year weather cycle with 1914 and 1938 being similar years to 2018, that saw wet years that followed. Peter believes that 2020 could be another dry year that might start wet, but taper off to be dry in the back half.

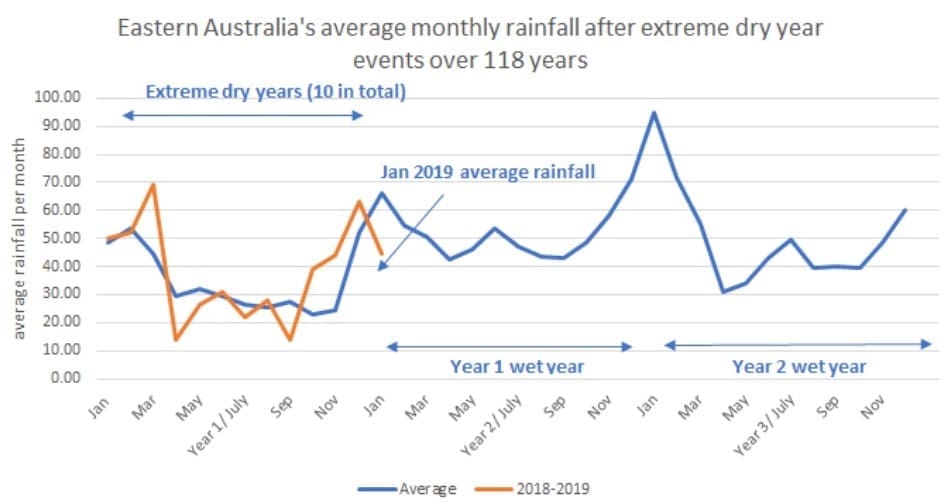

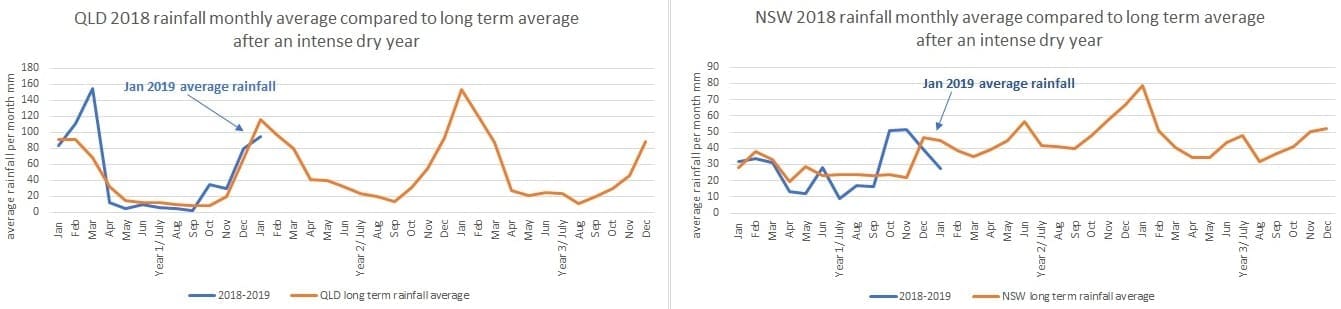

Does history repeat itself? My own analysis based on 118 years of rainfall data found 9 previous extreme dry years and compared to 2018. I put this discussion paper out in December and I have updated below the January rainfall for Australia’s Eastern seaboard and then looked at the individual states with some surprisingly accurate levels for NSW and QLD, although VIC’s December and January rainfall was well below and above the historic average for each month. But interestingly, the rainfall across both months averages out to be in line with long term trends.

The following were the past extreme dry years that were similar to 2018 – these are the driest average rainfall years in Australia’s recorded history for QLD, NSW and VIC. I looked at what happened after each of these previous extreme dry years and in each instance the rainfall was higher in year 2 & 3, and as stated, 2018 is showing a similar trend.

Table 1

Table 1

Click on graphs for a larger view

There are three very different views outlined in this section, with BOM believing an El Nino could develop in 2019 which would see ongoing dry conditions; Peter Nelson has outlined a wet 2019 but dry 2020; and I have looked at history as a guide which says that two wetter years normally would follow a dry year like 2019. It just says to me you need your own independent views on the weather outlook from professionals.

Flooding in northern Australia

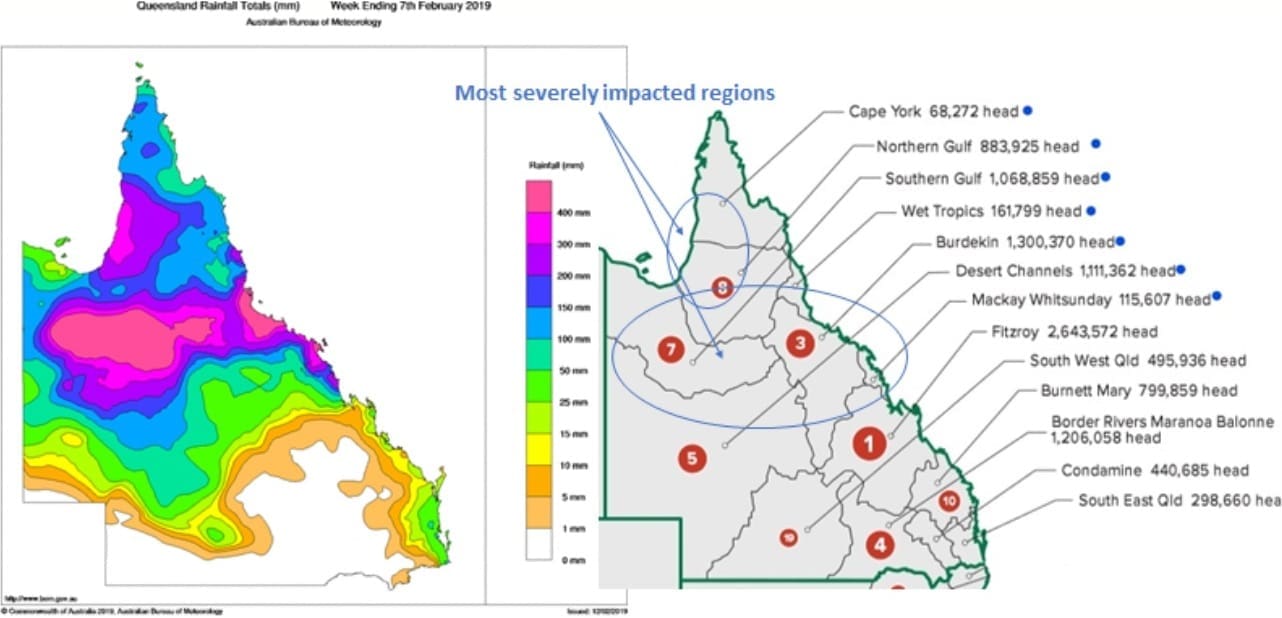

The situation so far in northern Australia and the impact of flooding is still very unclear and is expected to take at least 2-3 months before any accurate figures on livestock losses are known. We do know that in regions that have flooded, that there have been numerous reports of 40-50pc losses so far (in places much higher), with Julia Creek, Cloncurry and Richmond being some of the more serious areas.

When estimating the cattle population in the flooded regions based on rainfall received of 300-400 mm or more, I estimate close to 2.7 million cattle reside in these flooded areas. The current estimated losses of 500,000 head account for approximately 20pc of the adult cattle population in those regions.

What is not clear is the deaths of unbranded calves, given that the calf drop was about four months ago and that many of these young animals are extremely vulnerable. The tragedy is that two generations of cattle may have been lost by these floods.

The immediate challenge is to try to ensure that more animals that have survived the flood don’t die from malnutrition, hypothermia, bogging or potentially contaminated water with cattle producers very aware of the ongoing animal welfare issues and environmental issues that occur with such large losses.

When talking with pasture experts in the region, it is expected that it will take 4-6 weeks for the pastures to respond and that damage to pastures hopefully has been kept to a minimum due to Mitchell grass dominating the heavy clay soils of this region. I am told Mitchell grass has a deep root system of 1-1.5 metres and can sustain being underwater for up to 14 days without too much damage. Last week pasture regions I am told were underwater for 7-10 days and therefore hopefully have avoided too much damage.

The real issue is infrastructure, and this will take time to fix. Fencing, water/feeding facilities, yards could take 3-6 months or longer to address for many properties, and in the meantime ensuring cattle have water will be the immediate challenge.

There are also concerns about restocking the impacted land too quickly, with one grazier saying to me that the land needs 4-6 months to fully recover and for pastures to respond. Given cash flow issues, there will be a desire to get cattle back onto impacted properties as soon as possible.

Another positive is that the Great Artesian Basin received a much needed boost in reserves with critical recharge areas receiving good rain. In December torrential rains in North East Victoria saw many springs start to flow again as underground water supplies were replenished. Let’s hope the same holds for northern QLD.

Potential northern scenarios

The flooding and loss of livestock I believe will see several scenarios play out: firstly, those producers unable to afford to restock are likely to lease or agist their properties as a means of maintaining an income; and secondly, producers who can afford to restock will look to buy breeding animals and steers in the next 4-6 weeks as cattle are affordable in drought stricken areas.

Whether leasing land or restocking their own land, the emphasis will be on purchasing females, but there could be a push for young steers as well. This, I believe, is for cash flow reasons and creating an income by finishing these animals off.

The third scenario is that producers who have drought-stricken cattle in other regions will look to relocate these cattle onto flooded properties where pastures are likely to rebound. Either way, the flooded regions will produce grass and will I believe see a lift in cattle prices as producers look to replenish their herd numbers after the severe losses of the floods.

It should be noted that SE QLD, NSW and many parts of Victoria still remain extremely dry and restocking from these regions is expected.

Feed/grain prices – will these remain high?

The likelihood of grain prices remaining high for the balance of this year looks to be high, as both the winter and summer crop yield estimates are both expected to be lower. Winter crop production is expected to fall 23pc in 2018/19 to 27.12 million tonnes, while summer crop production overall is expected to fall 12pc with sorghum production up 6pc, which has been offset by a dramatic 44pc fall in cotton seed production.

Advance Trading grain forecasts

Advance Trading put the following forecasts together with three scenarios looked at:

- No rain in 2019 on the Eastern seaboard and in WA

- Good rain throughout 2019 (the drought breaks) and

- History repeating itself with good winter rains in Southern Australia and a wet October to April at the back end of 2019 and start of 2020 in northern NSW and QLD.

In brief, under scenario one, where no rain occurs both east and west coast, Advance Trading has forecast that grain prices would rise through the entire year increasing by $50 to $ 140 depending on the grain type most expected by Q4 to exceed $500 per tonne. The only exception is cotton which has started the year high at $575/tonne, which may fall to $520/tonne by Q4. None the less, these are very high prices on all grains.

Under Scenario 2, Advance Trading would see still strong prices for Q1 to Q3 but once the new crop becomes available, under this scenario would see Q4 pricing ease $150/t on most grains with sorghum expected to fall only $110 in Q4 but as the summer crop comes off, a further fall in Q1 of 2020 could be expected.

Under Scenario 3 (History repeating itself with a wet winter in the southern regions of Australia and a significant wet period in northern NSW and QLD in late 2019 and early 2020) Advance Trading’s forecast would see strong grain prices for Q1 to Q3 with Q4 easing but not to the same extent as scenario 2, with winter crop levels predicted to fall by $60/t and sorghum falling by $110/t.

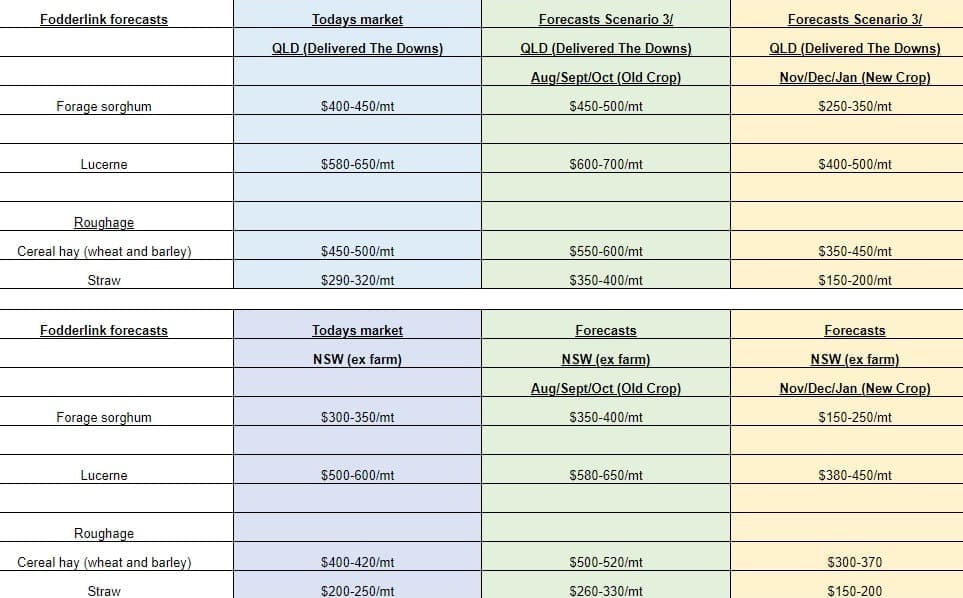

Fodder Link fodder forecast prices

I also spoke with Fodder Link on their views of where fodder prices are likely to head this year given recent events in northern Australia and the ongoing dry elsewhere.

In the last week, cereal hay prices jumped $50/t and are now trading at $270-350/t ex-farm on the basis of emergency fodder being bought for both the northern QLD flooded regions and for ongoing drought in other parts of Australia. These prices are being paid by charity fodder groups that have created a floor in the market (for all the right reasons). In addition, high irrigation prices are also keeping fodder prices firm.

Fodder Link provided the following forecasts based on the long-term trend (scenario 3 above) of a traditional wet southern winter and a very wet monsoon season for northern NSW and QLD in the back half of 2019 and early 2020, with history repeating itself. It should be noted that due to both the floods in the north and the continued dry elsewhere that they expect a spike in the short-term in fodder prices across the board, with the peak occurring in Aug/Sept/Oct (see below) due to the limited availability of ‘old crop’.

Should good traditional rains occur as outlined, then a dramatic fall in fodder prices in Nov/Dec/Jan is expected by Fodder Link as the expected good spring growth in pastures in southern Australia is likely to replenish the market with good supplies. Note that Fodder Link believe straw prices are likely to remain in the $150-200/t range post the rain due to less cotton seed hulls available and is now used as an important roughage provider in feedlots.

In each scenario outlined, the common element is the expectation of strong prices for winter and summer grains and fodder with or without rain. The critical period is Q4, and with rain will potentially see prices ease, and without rain prices are expected to go significantly higher. Should history repeat itself and the southern regions drought breaks first, then the upward pressure on feed prices is likely to ease after October.

Scenario 2 (though I think unlikely) If this should occur with good rain throughout all of Australia starting now then once again the desire to retain females increases and could see those areas that have missed rain step up and continue to buy fodder in Q2 and Q3 knowing full well that cattle prices are likely to go up significantly. So with good rain, it might see even stronger prices for fodder in Q2 and Q3 as restockers and breeders chase cattle hard once again knowing that by Q4 cheaper grain prices and good spring growth will ease overall feed costs.

So the take home message is that grain and fodder costs in Q1, Q2 and Q3 will remain firm no matter what. Fodder costs in the near-term might spike with a second peak in pricing to occur again in Aug/Sept/Oct , should traditional southern winter rains occur both grain and fodder prices are expected to ease in Q4.

Cattle prices – are they likely to go higher or lower?

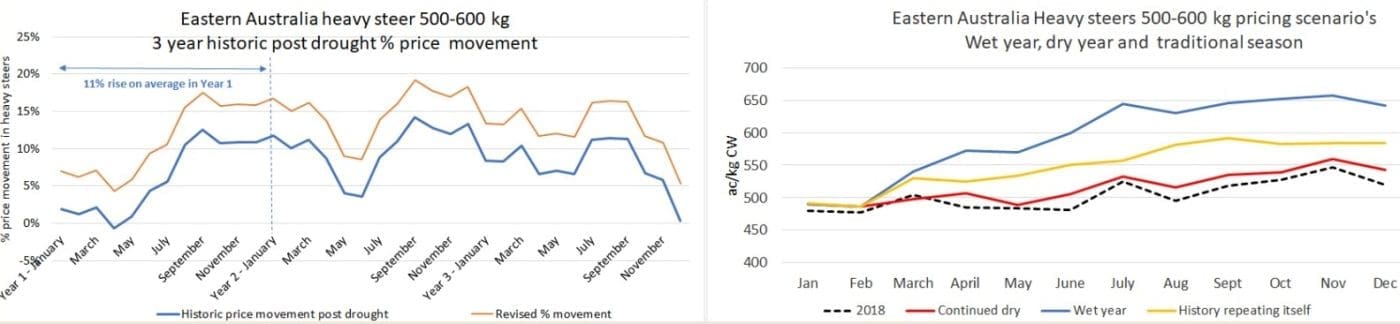

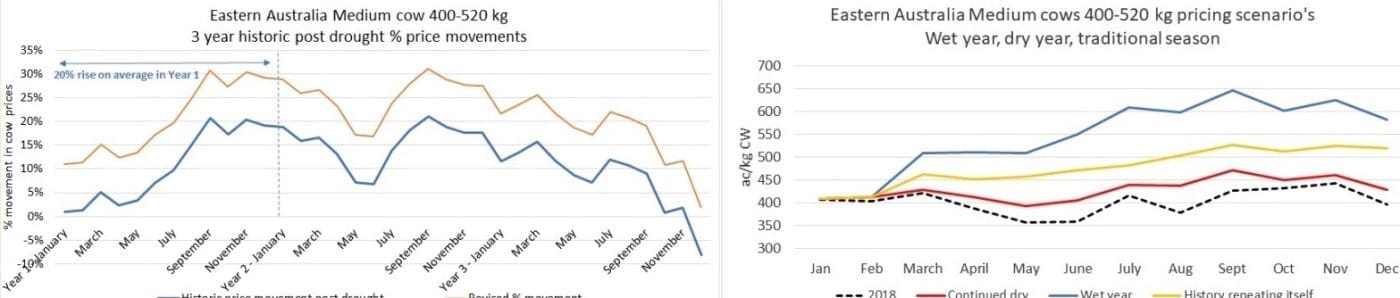

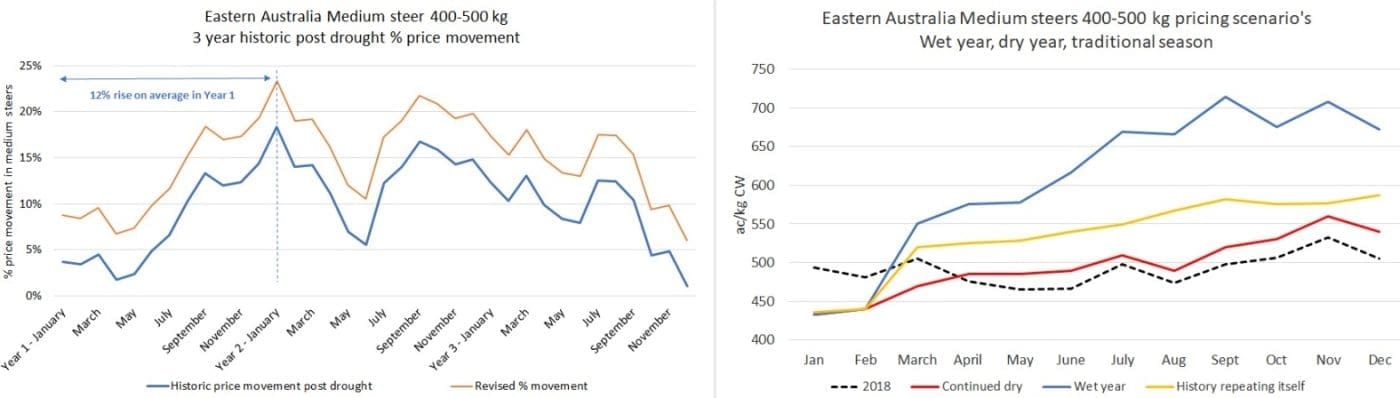

The impact on cattle prices under the three weather scenarios outlined above will vary depending on cattle type. I have done my best to map some potential pricing outcomes – these are my personal views and I would encourage sellers and buyers to seek independent advice from their local livestock agents.

I have looked at three cattle types – feeder steers, cows and heavy steers – and some of the potential price scenarios under three scenarios: no rain throughout 2019 and the drought to remain; a wet 2019 whereby the eastern seaboard receives excellent rain for the entire year; and thirdly, the scenario of ‘history repeating itself’ after an extreme dry year like 2018 whereby some initial storm related weather in northern Australia followed by a traditional wet southern Australia winter followed by a very wet monsoonal season at the end of 2019 and early 2020.

The following are my key beliefs in cattle prices for 2019.

The worst of cattle prices I believe are over, with this month being the likely low in prices for 2019. This is due to the high slaughter rates of 2018 which I initially believed would see the herd move to a critical low number of 26.3 million head by the end of 2019, and now with recent flood losses in northern QLD and cattle death estimates close to 500,000 head, this could see the Australian herd size fall further to 25.8m head. The last time Australia’s herd was at this level was 25 years ago in 1994 and 1995.

I believe the scenario of the eastern seaboard being wet for all of 2019 with widespread drought breaking rains beginning very soon is unlikely. It can be argued the northern QLD rains in the last week are drought breaking for this region though unfortunately southern QLD, NSW and VIC has seen almost no rain by comparison.

Given the lowest Australian herd size in 25 years at an estimated 25.8m by the end of 2019, I have added an additional 5pc in price rises for both heavy steers and medium steers and an additional 10pc increase in cow prices in my estimates, should the drought break this year and history repeats itself.

All cattle types will be impacted by the floods of the north, and the need to restock will likely see demand for breeding animals firstly, and to a lesser extent steers, which is likely to seeing buying commence in the next 4-6 weeks as northern pastures respond.

Cow prices are expected to increase the most, should the drought break this year. I have outlined a 20pc on average increase, but as stated in previous reports, this could be as high as 50pc should the losses in the north be greater than expected and the southern winter rains and northern monsoonal rains be sizeable.

It should be noted that these estimates are an average only and on a regionalised basis could see substantially greater (and lesser) price movements.

Medium steer prices are predicted to rise close to 12pc on average in year 1 post-drought, but prices have been known to rise overall by 22pc by year’s end.

As stated there might see good demand in the next few months as northern producers look to restock as pastures come on, and should a traditional southern winter occur more demand from southern growers who will also look to restock.

Global meat prices – are they like to remain firm?

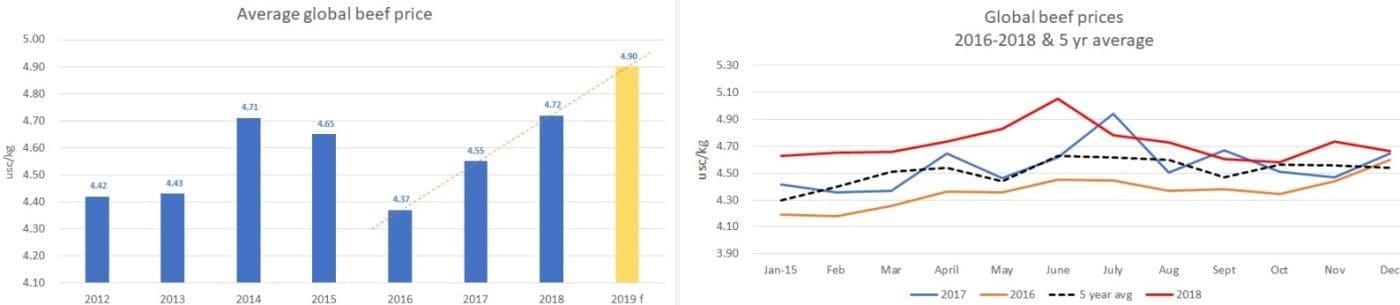

Global meat prices were 3.7pc higher in 2018 which has been driven mainly by demand out of Asia and in particular China. This has seen global meat prices reach a record high for 2018 in both monthly as well as yearly average price levels with a monthly high of US$5.05c/kg in June and a 2018 average of US$4.72c/kg. Should demand remain strong as expected, then 2019 will post a new record high in global beef prices reaching a yearly average of US$4.90c/kg.

These record beef prices are in spite of the global trade wars that continue with high China tariffs on US pork and beef and a revised NAFTA trade deal that is still to be ratified by respective countries. Should these issues be resolved during 2019, this will give more support to global beef prices.

The reasons for the strong demand can be attributed to the following factors:

- Continued growth of the Asian middle class

- The growing presence of African Swine Fever in China which has seen substitution for pork with increased chicken and beef consumption

- The crackdown on the grey trade into China which has seen Indian buffalo shipments fall in volume and an increase in direct beef imports from Australia and many other export countries that have China-approved meatworks.

- Strong demand from our traditional markets Japan, Korea and the US.

Will this strength in global beef prices continue in 2019? I think the answer is yes, with the current strength in demand from Korea, US and Japan likely to continue and the ongoing impact of African Swine Fever in China likely to see pricing for beef within China remain firm.

What could well drive beef prices higher in 2019 is if ASF should spread to other surrounding countries in Asia such as Taiwan, Korea, Thailand and Japan. This would have likely a two-fold effect (as we are seeing in China) of a large liquidation of the pig population either because of the disease or due to culling as a means of controlling the disease. The net affect would be a huge deficit in pork/protein supply. The second impact would be consumers moving away from pork to chicken and beef as consumer sentiment toward pork would turn negative (as we have seen in China).

When assessing global beef supply in 2019, herd expansion has slowed in key beef export countries such as the US, New Zealand and Canada – with Brazil, Australia and Argentina all expecting herd reductions which could see collectively 5 million fewer cattle from key export countries in 2020.

This would be price supportive – the challenges are really this year with global beef production expected to increase by 1.4pc to 69 million tonnes CWE, close to 17pc of this volume is traded globally.

Global beef demand is expected to grow 4pc which will more than offset the increase in supply. I have forecast the 2019 global beef price at US$4.90c/kg, or up 18c/kg which when spread across global meat production would raise total beef values by a staggering 12.5 billion US$ globally.

Foreign exchange – what is the outlook for the Australian dollar?

Bloomberg news service in recent months conducted a survey among 72 foreign exchange market participants including banks and economists asking for their views on where they expect the Australian dollar to be over the next 12-24 months.

Australian dollar forecast

Source: Bloomberg

The overwhelming view is for the A$ to rise on average by 200 points and to be at US74c by the year end, but it should be noted that the predicted highs have a potential 600 point upside, with US85c quoted by the majority of survey participants and on the downside only a 200 point fall with a potential low of US65c by Q4.

For many industry participants these forecasts are taken with a grain of salt, but it is worth noting what the likely influence a rising or falling A$ has on meat and cattle prices.

Should the A$ fall by 400 points, then in today’s market on a typical load of grinding meat, CFH 90’s (205 CIF EC) this would add US33cc/kg to the value of the meat, which in turn might add $6300 to a container of CFH 90’s (20 footer). This would equate to an increase of A12c/kg live weight on a cow in the saleyard in an ideal world.

The issue of who gains the benefits or disadvantages of a fall or rise in the A$ is not always clear.

To me it depends on whether there is over supply or under supply in the meat/cattle market and also whether demand is strong or weak. For example if the drought should break this year, then cattle and meat supply is likely to get very tight. And if the forecasts of strong global meat demand should be true, then this is the perfect environment for any falls in A$ to be passed-back down the supply chain to farmers. Should the A$ rise, the negative impact on cattle pricing is often slow or non-existent, as the impact from other variables like higher bids from any country can outweigh on any day the impact of currency.

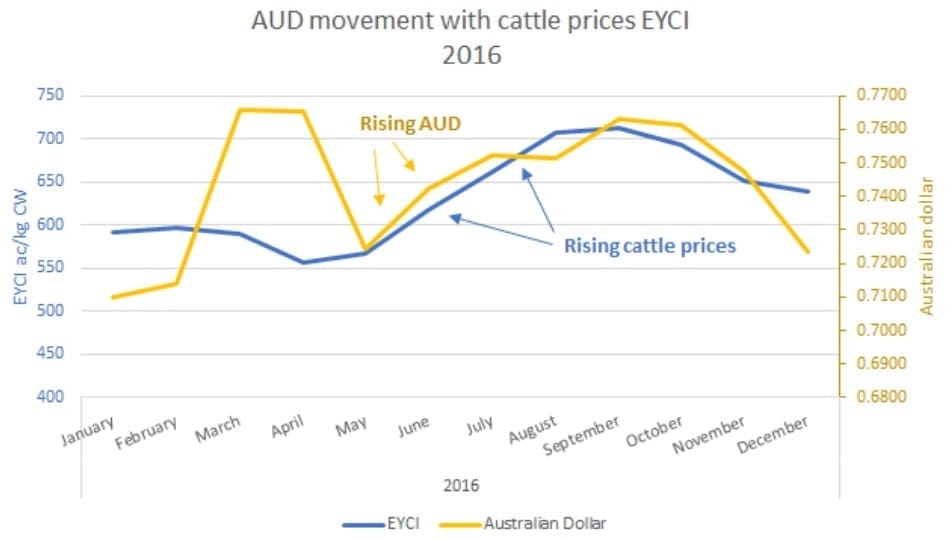

This was most obvious in 2016 when cattle supply was extremely tight and the A$ rose 400 points from May to September that year, and also saw a 145c/kg carcase weight increase (or 78c/kg liveweight gain) in cattle prices.

In other words, a 5.5pc rise in the currency saw a 25pc gain in cattle value – the complete opposite of what should have happened with a rising A$, where cattle prices should have fallen. So it tells me that the impact of other variables such meeting contract/customer needs, global beef prices and meeting minimal abattoir throughput levels have a far greater influence often on cattle prices than changes in the currency.

It would not surprise me if we saw similar currency and cattle price movements occur again over the next two years, with both cattle prices and the A$ potentially moving higher as it did in 2016.

It should also be noted that a high or low currency in a tight cattle supply market might not impact the volume of Australian cattle slaughtered, as producers are likely to rebuild their herds no matter what, and bring them to market when ready. But a low currency might influence certain sectors such as the grainfed market – whereby due to our low A$, Australia might be more competitive on grainfed beef compared to the US and this might see more cattle go on feed at the time.

In summary, the impact of currency is likely to be minimal in a tight supply market on influencing farmers to sell more or less, but a low A$ might make one sector (like grainfed) more competitive than another depending on what competing supply countries’ currencies are doing at that time. So volumes of cattle slaughtered would not necessarily change but the mix of cattle might due to the currency.

Summary

While the three weather scenarios outlined above are very different views, there are some common threads in this summary that could occur under any of these three.

Firstly, grain and fodder prices will remain firm for Q1-Q3 no matter what; secondly, the Australian herd size will be at a 25-year low by year’s end; thirdly, with or without rain, cattle prices are expected to rise; and finally, global meat prices are expected to rise by 4pc this year.

I have done my best to outline how grain, fodder and cattle prices might look under each of these weather scenarios, in the hope that it will assist readers in making better decisions themselves by doing their own research or seeking further advice.

Given the variables outlined in this paper and the potential upside in the market it’s well worth the effort.