YESTERDAY’S release of Australian Bureau of Statistics beef slaughter data provides the clearest signal yet that the national beef herd has moved back into liquidation phase, driven by rapidly encroaching dry conditions across large parts of eastern Australia.

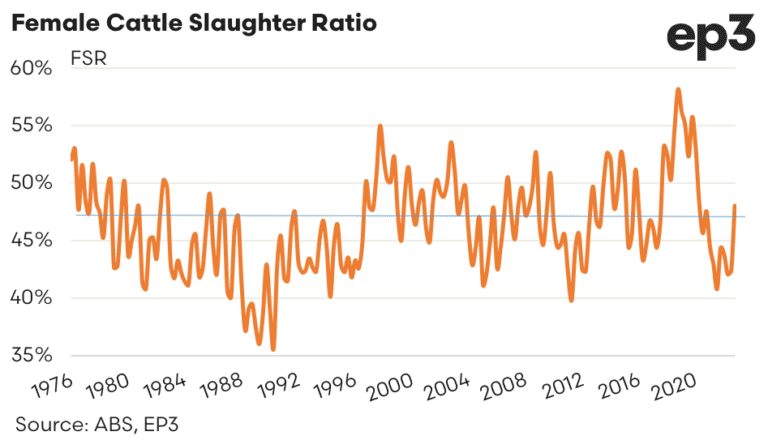

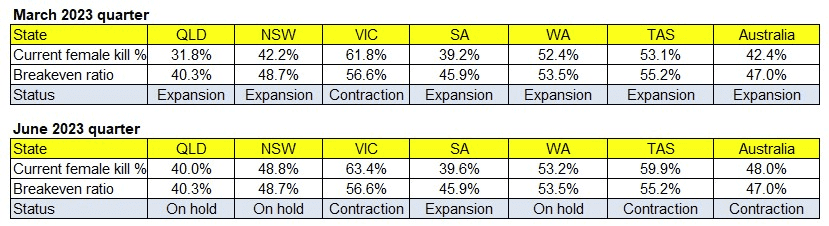

Forty seven percent females in the makeup of any period of adult cattle slaughter is the theoretical tipping-point between herd contraction and expansion. ABS’s June quarter data released yesterday suggests female kills last quarter have in fact reached 48pc.

Mat Dalgleish

The trend is clearly seen in the graph below, produced by Episode 3 analyst Matt Dalgleish.

The Female Slaughter Ratio (FSR) for the June 2023 quarter came in at 48pc, which is the highest it has been since quarter four of 2020, signalling that we may be in herd liquidation now,” Mr Dalgleish said.

“This increase to the FSR over the June quarter brings the annual average FSR for 2023 to 45.2pc, so on an annual basis we aren’t quite at liquidation phase….yet,” he said.

Beef Central first wrote about the looming prospect of a return to herd liquidation in this article published back in July, when NLRS weekly national slaughter data for the first time in three years produced a weekly female kill of above 47pc. The trend has been growing for the past three months.

Meat & Livestock Australia acknowledged the trend, but told Beef Central it was not yet ready to adjust its industry projections outlook, until the third quarter female slaughter result (ending 30 September) followed the same trajectory.

“We knew that a lot of those extra (older) cows that powered the herd rebuild during 2021 and 2022 would have to hit the market at some stage, but if the FSR stays like this in quarter three, we will have to revise our projections forecasts,” MLA market information manager Stephen Bignell said.

“But we’re not ‘calling’ a liquidation cycle at this point. It needs to be considered that different states are still operating differently. Queensland’s FSR, for example, is still only 39pc, suggesting its dry cycle is not as advanced as regions further south.”

“But we’re not ‘calling’ a liquidation cycle at this point. It needs to be considered that different states are still operating differently. Queensland’s FSR, for example, is still only 39pc, suggesting its dry cycle is not as advanced as regions further south.”

Historically, Queensland’s FSR is lower than other states, because large number sof export feeder cattle (steers only) are drawn from southern states, as well as Queensland.

The big turnoff of all cattle types in NSW – cows and young cattle included – was clearly telegraphed in this feeder cattle price summary published on Wednesday.

“Yesterday’s ABS female kill ratio figure is an important lead indicator, but we’re not yet in full-blown liquidation,” Mr Bignell said.

Other key points raised in yesterday’s ABS slaughter data:

- Quarterly cattle slaughter was 1.728m head – the highest quarterly number since September 2020, as the drought subsided

- FY 2023 saw 6.29 million adult cattle slaughtered

- Adult cattle slaughter has reached 3.27 million head for the first six months of 2023 – 15.6pc above the (very low) 2022 levels

- Adult carcase weights averaged 315kg during the quarter – a drop from 2022

- Cattle farmers made $3.3b in receipts for the quarter – the same they made in 2021 when receipts were high

- For FY23 cattle farmers made $14.28 billion from the sale of slaughter animals (ABS started surveying revenue from livestock in 2019)

- Over the same period lamb and sheep farmers made $4.8b from the sale of animals to processors; pork farmers made $1.6b and chicken farmers $3.67b

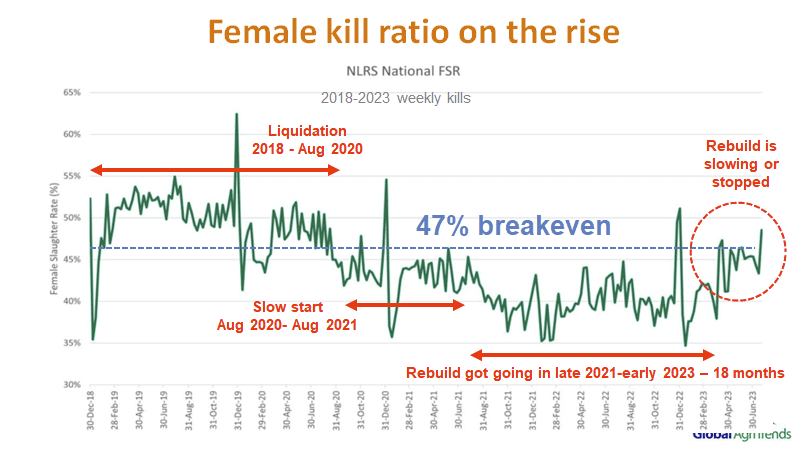

Independent analyst Simon Quilty has produced his own female slaughter ratio history graph, covering the period from late 2018 to June this year.

Click on image for a larger view

It illustrates the liquidation period during the drought from late 2018 to August 2020, followed by the slow start to rebuild over the next 12 months, and the rebuild in earnest from late 2021 to early 2023, bookended by the latest rise in female slaughter ratio.

Simon Quilty

“To many market participants this is no surprise given the heavy kills witnessed for the last five months, given these figures reflect the NLRS weekly ratios, the next quarterly figures are expected to show and even greater liquidation with female kill moving considerably higher in the last eight weeks,” Mr Quilty said.

The other key point to note was the relatively small number of females slaughtered to reach this liquidation ratio which pointed to a much smaller herd size, he said.

Which states are liquidating?

New South Wales has been the state that has shown the greatest female kill in the NLRS weekly figures, but when looking at ABS numbers, it would imply VIC and TAS are in a more concerning situation, Mr Quilty said.

“What is very clear is that Australia’s rebuild has stopped, and with areas getting drier as we move into an El Nino it will see more contraction of the herd as female slaughterings move higher.”

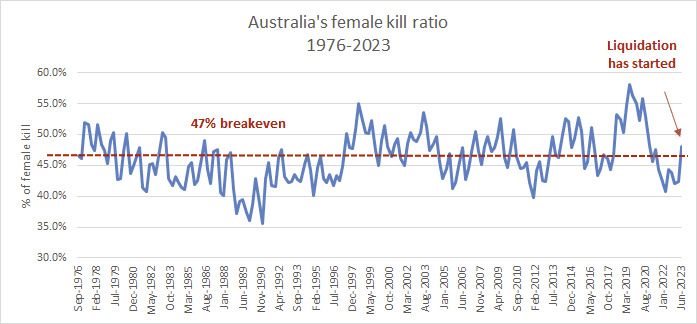

“It is at this point in time that a much clearer picture of the herd size can be estimated at what is best described as ‘the turning point’, whereby the ratio of the herd and female kill ratio line up (see graphs above, and longer-term, below).

Set out below are the breakeven ratios per state. It shows that one state (South Australia) is expanding; two are contracting in size due to liquidation and three (QLD, NSW and WA) are ‘on-hold’ – neither expanding or liquidating. As observed earlier, more recent weekly NLRS kill data suggests that NSW has now moved into a much greater liquidation phase in the last 12 weeks.

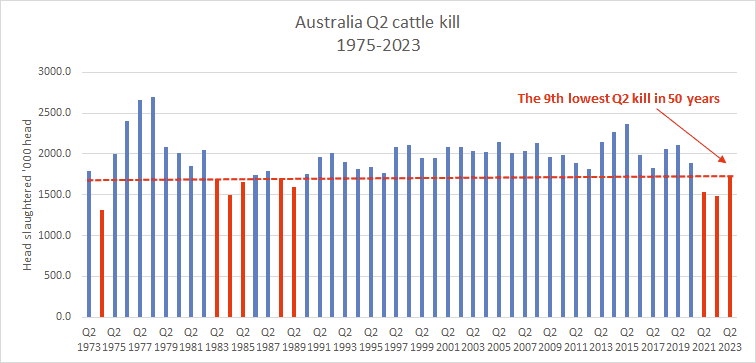

How does this year’s Q2 slaughter compare with other years?

Australia’s Q2 kill was 1.728 million head, the ninth lowest kill in 50 years since 1973 (see graph below).

“This once again reflects a smaller herd size. When the Australian herd was at 28.4 million head in 2006, the Q2 kill was at 2.015m or 17px higher than today, a far cry from today’s lower numbers,” Mr Quilty said.

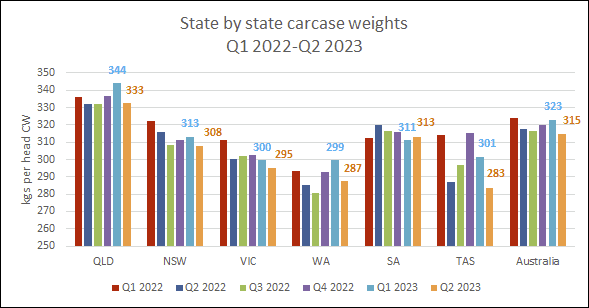

Carcase weights

Carcase weights have fallen since Q1 this year based on the drier conditions felt across all states, with lower levels recorded with the only exception being South Australia which lifted moderately, by 2kg. Australia’s overall carcase weights fell 2.5pc from 323kg to 315kg last quarter, reflecting the drier conditions.

“What is interesting to note is that even with the increase in Australian cattle on feed for the June quarter which was at 1.256 million head, carcase weights fell in Queensland, easily the largest feedlot state,” Mr Quilty said.

“This fall would indicate that pasture-fed slaughter cattle are losing condition quickly, outweighing the larger cattle on feed number turnoff. Another explanation is there is more opportunistic short-term feeding and less larger longfed program beef being turned off, which has led to lower carcase weights. The true answer maybe a combination of these reasons.”

Beef Central will next week look into reports that a number of lotfeeders have launched cow-feeding programs, designed not to produce GF cipher beef, but simply to put weight onto poor cows before slaughter.

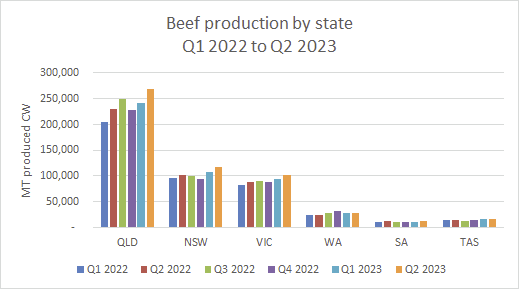

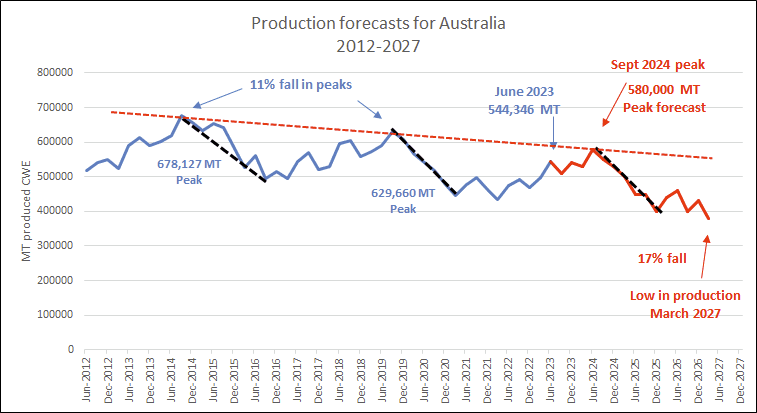

Beef production increases on the back of increased slaughterings

Australia’s beef production has increased in Q2 on the back of higher slaughterings, and not on any increase in carcase weights. Dry conditions have led to higher turnoff which has driven production higher, with Queensland, NSW and Victoria being the three states that have contributed the most. Mr Quilty expects this increase in production to continue until Q3 2024.

This increase in production in the June quarter of 544,346t was inline with Mr Quilty’s forecasts, which he expects to peak in September 2024 at 580,000 head before Australia moves into the next cattle cycle and production falls away with the low in production expected in 2026 and 2027.

Domestic beef share in decline, as production grows

The Australian beef industry’s reliance on the domestic market decreased in the June quarter, with exports back to almost 70pc of total production.

“This is no surprise with an increase in overall production, there is only so much that can go domestic. The other key point is that the Australian domestic market like so many other markets is super-saturated with meat and additional product needs to go export,” Mr Quilty said.

“The other key point to note is that the headaches of COVID and logistics have lessened, and freight rates have fallen, which has also seen the ability to export become easier.”