Image: Shutterstock

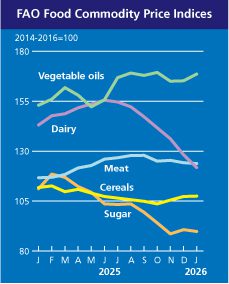

THE measure of world food commodity prices declined in January for the fifth consecutive month, led by lower international quotations for dairy, sugar and meat products, according to the Food and Agriculture Organisation of the United Nations (FAO) benchmark report.

The FAO Food Price Index (FFPI), which tracks monthly changes in the international prices of a basket of globally traded food commodities, averaged 123.9 points in January, down 0.4 per cent from December.

Declines in the price indices for dairy products, meat and sugar more than offset increases in cereals and vegetable oil, marking the fifth consecutive monthly decline of the index.

The FFPI stood 0.8 points (0.6pc) below its level one year ago and as much as 36.4 points (22.7pc) down from the peak reached in March 2022.

FAO Food Commodity Price Indices

The FAO Meat Price Index averaged 123.8 points in January, down 0.5 points (0.4pc) from December, but still 7.1 points (6.1pc) above its level a year earlier.

The decline mainly reflected lower international pig meat prices, while quotations for bovine and ovine meats remained broadly stable. By contrast, world poultry meat prices increased.

Pig meat prices dropped largely due to softer quotations in the European Union amid subdued international demand and ample supplies, including the clearance of backlogs associated with temporary abattoir closures during the end-of-year holidays.

Despite relatively tight supply conditions, world ovine meat prices remained largely stable, as seasonal demand softened following high end-year purchases.

Bovine meat prices were also broadly stable, amid shifts in Brazilian exports to other destinations following the rapid exhaustion of the United States of America tariff-free quota and the subsequent application of the 26.4pc out-of-quota tariff.

Shipments were increasingly redirected toward China, where importers accelerated purchases to secure volumes ahead of the announced beef safeguard quota, offsetting potential downward pressure on Brazilian prices.

The FAO Cereal Price Index averaged 107.5 points in January, up marginally by 0.2 points (0.2pc) from December but remaining 4.4 points (3.9pc) below its level a year earlier.

World wheat prices were broadly stable in January, declining by just 0.4pc from December.

Upward pressure stemming from strong export sales by Australia and Canada, along with weather concerns affecting dormant crops in the Russian Federation and the United States of America, was offset by an overall comfortable global supply situation.

Expectations of good harvests in Argentina and Australia, together with high global stock levels, continued to exert downward pressure on prices.

International maize prices also continued their downward trend, easing by 0.2pc from December.

Although weather-related concerns over planting conditions in Argentina and Brazil, combined with strong ethanol demand in the United States of America, provided some price support, they did not offset the generally bearish market sentiment driven by ample global supplies.

Among other coarse grains, world barley prices recorded a modest increase, supported by robust demand for Argentinian supplies, while sorghum prices mirrored movements in the wheat market, easing slightly.

By contrast, the FAO All Rice Price Index increased by 1.8pc in January 2026, reflecting firmer demand, especially for fragrant varieties.

The FAO Vegetable Oil Price Index averaged 168.6 points in January, up 3.4 points (2.1pc) from December and standing 10.2pc above its level a year earlier.

The increase reflected higher world prices of palm, soy and sunflower oils, which more than offset lower rapeseed oil quotations.

International palm oil prices rose for the second consecutive month, underpinned by seasonal production slowdowns in Southeast Asia and firm global import demand driven by improved price competitiveness.

Meanwhile, world soy oil prices rebounded on tightening export availabilities in South America and expectations of robust demand from the biofuel sector in the United States of America.

Regarding global sunflower oil prices, after declining for two successive months in late 2025, they also recovered, driven by continued supply tightness in the Black Sea region, where farmer selling remained limited.

The FAO Dairy Price Index averaged 121.8 points in January, falling by 6.4 points (5.0pc) from December and standing 21.3 points (14.9pc) below its level a year ago.

This marked the seventh consecutive monthly decline of the index, driven largely by lower world cheese and butter prices, which more than offset modest increases in the quotations of milk powders.

International cheese prices registered the sharpest drop in January, reflecting heightened global competition.

Ample supplies in Europe and the United States of America exerted downward pressure on quotations, outweighing firmer prices in New Zealand.

Whole milk powder prices rose only modestly, as demand remained below historical levels, limiting the extent of the increase.

The FAO Sugar Price Index averaged 89.8 points in January, down 0.9 points (1pc) from December and 21.4 points (19.2pc) from its value a year ago.

The decline was driven by expectations of increased global sugar supplies in the current season, largely underpinned by a significant production rebound anticipated in India and favourable prospects in Thailand.

In addition, despite a reduction in the share of sugarcane allocated to sugar production, the overall positive production outlook for the 2025/26 season in Brazil contributed to bolster global supply expectations, reinforcing the downward pressure on world sugar prices.

Source: Food and Agriculture Organisation of the United Nations