Two months after the Reserve Bank of Australia cut rates to a historic low of 2.75 percent, the RBA Board has today opted to again keep the official interest rate on hold.

Two months after the Reserve Bank of Australia cut rates to a historic low of 2.75 percent, the RBA Board has today opted to again keep the official interest rate on hold.

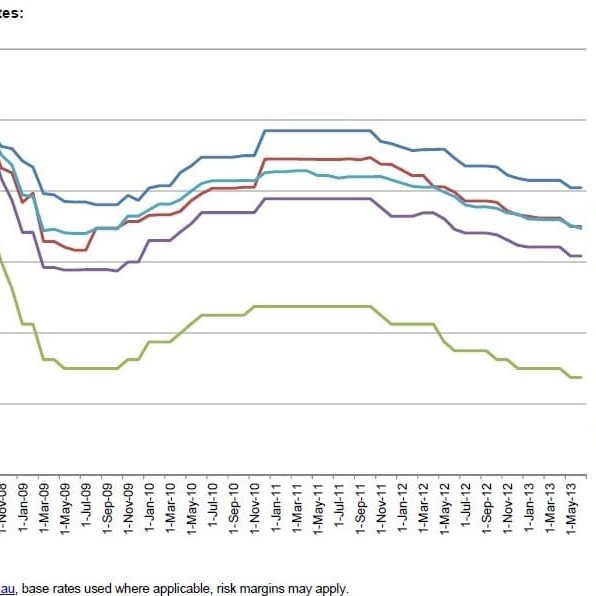

Today’s RBA decision came as the National Farmers Federation released its June Agribusiness Loan Monitor, which shows that only one bank passed on a rate cut during this month – Bendigo Bank, with a rate cut of 0.25 percent for its term loan and agribusiness customers – following rate cuts from all other financial lenders in May.

NFF chief executive Matt Linnegar said the Federation was pleased to see that all banks had now passed on at least some of the RBA’s earlier rate cut, with the majority of lenders passing on the full 0.25 percent.

“Even though the RBA today left rates on hold, the rate cuts from the banks following the May interest rate reduction, combined with the fall in the Australian dollar over the past two months, brings with it some relief for the farming sector,” Mr Linnegar said.

“As Australia exports 60 percent of its agricultural produce, Australian farmers watch the financial markets almost as closely as they watch the weather.

“As the dollar value reduces, Australia’s farm exports become more competitive on the global market, which is why we’re pleased to note that the Australian dollar is today sitting at 92c against the US dollar, after dipping below parity in mid-May.

“Of course, it’s a double-edged sword, with farmers also relying heavily on many imported inputs – like machinery and diesel – the costs of which will go up with a weaker Australian dollar,” Mr Linnegar said.

His comments come as farmers patiently await detail from the Federal, State and Territory Governments on the Farm Finance package, announced in late April.

“Two months after the Federal Government announced that financial assistance would be made available to farmers facing hardship, we are still yet to see any of the State or Territory Governments sign up to the package,” Mr Linnegar said.

“This means that two months on, not a single dollar has been passed on to a farmer in need. We urge the respective governments to put the politics aside and get on with delivering the policy.”

On the inflation front, NAB economist David de Garis said the RBA still expected inflation to be consistent with its target over the next one to two years, this time adding the provisio: “notwithstanding the effects of the recent deprecation of the exchange rate,” in its commentary.

“This has allowed the RBA to retain its easing bias given the ‘below trend’ economy,” Mr de Garis said.

“The RBA continues to see the A$’s decline as a helpful development to re-balance growth. Commodity prices have declined, the terms of trade while high, is in decline, and the currency will provide some buffer here.”

In that sense, there was an implicit ‘green light’ to a further decline in the A$ value from the RBA, with the currency dipping half a cent in the immediate wake of this afternoon’s 2.30pm announcement.

“We expect the A$ to decline further, over time,” Mr de Garis said, “and we continue to expect that a further widening in under-performance of the Australian economy will see the RBA come back with another easing in interest rate before the end of the year.”

- The NFF’s Loan Monitor is compiled each month by money market monitor Canstar and published by the NFF as a tool for all Australian farmers.