Mid-year forecasts out of the United States continue to suggest the US will be a significant net beef exporter in 2011, after a 2010 year when the country’s exports and imports were almost identical.

Mid-year forecasts out of the United States continue to suggest the US will be a significant net beef exporter in 2011, after a 2010 year when the country’s exports and imports were almost identical.

By June 30, US beef imports continued to track well below levels seen for the same period last year and forecasts are for US beef full-year exports to surpass imports by about 187,000 tonnes.

To put that into perspective, consider that in 2011, US Department of Agriculture expects total US beef disappearance (technical term meaning beginning inventory plus production plus imports, minus exports and ending inventory) to be 11.8 million tonnes, 1.4pc or 163,000t less than a year ago. In other words, the decline in overall US beef supply availability in the US domestic market is largely a result of the shift in US beef trade patterns and, to a lesser extent, lower beef production.

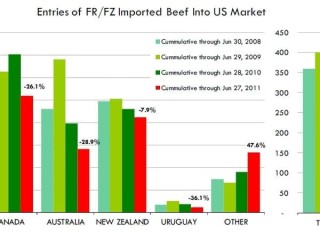

The chart on this page, which can also be viewed below in larger format, summarises the latest statistics for US imports for fresh/frozen beef product. By June 27, total beef imports from all countries were down 14.8pc from a year ago.

Worst hit was Australia, which is down 28.9pc compared to the already low levels in 2010 and a whopping 59pc lower than in 2009. That is mostly due to the depreciation of the US$ versus the A$. To put it into context, in 2009, Australian beef exporters shipping product to the US received back a little over A$1.50 for every US$1.00 worth of product they sold. Today, US$1.00 only brings Australian exporters about 95c in Australian money.

Demand for Australian product in other markets, particularly Asia and Russia, remains strong, tempting Australian exporters to do business elsewhere. Russia has emerged as a significant buyer of Australian beef, as Argentina and Brazil – traditionally two large beef suppliers to the Russian market – have cut back on exports.

“The shortages of South American beef in the global market has supported to this point the upward trend in US beef exports this year, while limiting US beef imports,” US analysts Len Steiner and Steve Meyer said in their Livestock Report last week.

“In the case of Argentina, beef exports are down sharply in part due to the significant liquidation of the cattle herd that took place over the last couple of years, but also because of government policies that have sharply curtailed beef exports.”

Brazilian beef exports in the first five months of 2011 were down 16pc compared to the same period a year ago.

“Brazilian producers are trying to rebuild their herds while at the same time trying to meet growing domestic demand. The value of the Brazilian currency has also risen sharply in the last two years given strong rates of economic growth and the influx of investment money,” the Daily Livestock Report said.

Also important to note in the chart appearing on this page is the sharp decline in US beef imports from Canada. The decline reflects smaller cattle inventories and the negative impact of a strong Canadian currency, which currently trades at a premium to the US$.

“The only reason US imports of fresh and frozen beef are not down even more is because we are currently importing more beef from Mexico (up 75pc on last year) and from Central America (up 29pc),” Mr Steiner said.

The absence of cooked beef imports into the US has also impacted on overall US beef supply this year.

Data to the end of April shows that even though cooked US beef imports accounted for just 4pc of overall import trade, they contributed about 22pc to the overall decline. Imports from Brazil in the first four months of 2011 were down 90pc while total cooked beef imports were down 54pc from last year.

This has supported the value of some leaner beef cuts in the US and contributed to overall recent high US cow and steer carcase values.