FOOD and livestock prices have been singled-out for special scrutiny in an upcoming Federal government competition review, conducted every ten years.

During a recent meeting of federal and state agriculture ministers, the deteriorating seasonal conditions and impending drought over parts of regional Australia were recognised by the ministers in attendance.

They noted that these conditions were contributing to sharply declining livestock prices impacting farming businesses, their families and regional communities.

They noted that these conditions were contributing to sharply declining livestock prices impacting farming businesses, their families and regional communities.

During the meeting the ag ministers encouraged the consideration in forthcoming Commonwealth competition reviews of the impact of competition on commodity (livestock and crop), food and grocery prices.

Much has been said about the relationship between this year’s collapsing livestock prices and relatively stable retail meat prices over the past six months.

Recently, the Federal Government launched a review of competition policy settings through the Federal Treasury, to “help build a more dynamic and productive economy.”

The Commonwealth Competition Review is routinely conducted every ten years.

Federal agriculture minister Murray Watt said the review would focus on whether farmers and livestock producers were being paid fairly for their produce.

In an earlier statement, Federal treasurer Jim Chalmers said greater competition was critical for lifting dynamism, productivity and wages growth, putting downward pressure on prices and delivering more choice for Australians dealing with cost-of-living pressures.

“Australia’s productivity growth has slowed over the past decade, and reduced competition has contributed to this – with evidence of increased market concentration, a rise in mark-ups and a reduction in dynamism across many parts of the economy,” he said.

“Australia’s productivity growth has slowed over the past decade, and reduced competition has contributed to this – with evidence of increased market concentration, a rise in mark-ups and a reduction in dynamism across many parts of the economy,” he said.

“We need to ensure our competition policy settings are fit for purpose in the face of the big shifts underway in our economy, so we can make the most of digitalisation, the growth in services, the net zero transformation, while supporting our nation’s most vulnerable,” Minister Chalmers said.

The review will look at competition laws, policies and institutions to ensure they remain fit for purpose, with a focus on reforms that would increase productivity, reduce the cost of living and boost wages, the government said.

Two-year process

A Competition Taskforce was established in Treasury to conduct the review, which will be progressed over two years and involve targeted public consultation.

The taskforce will provide continuous advice rather than a formal report, so progress can be made over time, the government said.

The Taskforce will be supported by an expert panel with members including the chief executive of the Grattan Institute, Danielle Wood, and former Chair of the ACCC, Rod Sims.

Other related reports

The Federal Government’s Inter-generational Report, due for release later this month, will highlight the critical role of competition for revitalising productivity growth, the Government says.

The importance of competition for strong labour market outcomes will be further explored in its forthcoming Employment White Paper.

“The Federal Government is focused on tackling cost of living pressures now and laying the foundations for future growth – and making our economy more competitive is critical to both of these goals,” it said in a statement.

Questionable outcomes

Australian Meat Industry Council chief executive Patrick Hutchinson said clearly, the issue of retail versus livestock pricing at present was “exceptionally topical”, but he was doubtful about what any Treasury investigation into competition and pricing was going to find – other than market forces (simple supply and demand) at work.

“AMIC recognises the sheer, near-vertical increase in livestock prices that occurred in 2020-22,” Mr Hutchinson said.

“We also recognise the sheer vertical drop that’s occurred in 2023. Both are at record levels – and even the small ‘rebounds’ that have occurred in recent weeks due to rain in some segments, have hit records.

“So we’ve seen record highs, followed by record lows, followed by a record single-day jumps in an indicator. It shows just how volatile this market is, and has been – across all commodities and indexes.”

“But the circumstances have to be viewed very, very carefully – probably through a number of lenses. It is not a binary issue that’s being talked about – with influences from exchange rate to weather, international demand, inventory in cold storage and builds-up in livestock supply, through to workforce challenges and other issues.”

“When we saw the three-year build up to record increase in livestock prices in 2022, everything was quiet, because the system was perceived to be ‘working.’ Now, all of a sudden, the system does not ‘seem to be working,’ so some people feel it is somehow broken, and needs to be rebuilt.”

“Nothing has changed, apart from supply and demand.”

Price lag

In a recent commentary, Meat & Livestock Australia noted that while livestock prices for cattle and sheep have declined significantly this year following historic highs in 2022, the reduction in average retail price of red meat lagged prices paid to producers by approximately eight months.

“This is due to the amount of livestock supply available, demand for Australian red meat in export markets, and rising input costs through the value chain,” it said.

In the 12 week period to 13 August, retail prices for beef and lamb had declined significantly, following a trend that has continued throughout 2023, demonstrating that the fall in livestock prices had started to impact the price paid at the checkout, MLA said.

Appearing on the national Sunrise morning TV program, MLA managing director Jason Strong recently addressed the lag in pricing between livestock and retail meat prices.

In an earlier MLA item published on the service delivery company’s website last month, industry insights and strategy manager Scott Cameron said the performance of Australian lamb and beef in the domestic market remained solid, with both proteins growing in sales volume and overall value.

When comparing the June quarter with the same period last year, value growth for beef was 1.8pc and for lamb, 4.2pc.

Data from the Nielsen HomeScan retail surveys showed a 7.3pc reduction in the price consumers were (last month) paying for lamb compared to a year ago, which was supporting a 12.4pc increase in volume of lamb purchased at the cash register.

“The price reduction is translating to increased purchasing frequency for several cuts,” Mr Low said.

“This is especially the case for the most popular cuts like lamb legs and chops, which are up 20pc compared to a year ago.”

“Consumers see these price reductions, and purchase more as a result. As this happens, retailers are looking to bring in customers with competitive pricing through catalogue promotions, and increased stock on the shelf,” Mr Low said.

For beef, Nielsen Homescan last month reported 7.1pc growth in volume in the previous quarter, compared to the same period last year, with an average retail price decrease of 4.9pc. Frequency of purchase and volume per purchase are both up in the latest quarter as well.

“Tracking commissioned by MLA on behalf of industry, said that consumers see both beef and lamb as increasingly worth paying more for due to their high quality and taste,” Mr Low said.

Relationship between livestock and retail meat prices

Historically, data on supply, pricing and consumer demand showed that it takes about eight months for livestock prices to translate to the retail shelf, Mr Low said.

“The last time in recent history that beef prices dropped considerably was in 2012, with the lag to shelf arriving eight months later, with those lower prices remaining for about nine months,” he said.

“For lamb, which has seen a drop in prices in the fourth quarter of the calendar year every year since 2018, it experienced significant price drops in 2012-13 and 2016-2018. Correspondingly at this time, retail pricing took about nine months to fall.”

As well as additional supply chain pressures occurring currently, there are a variety of factors that drive pricing in the retail market,” Mr Low said.

“Livestock prices are only one component of retail meat prices. Producing retail meat requires investment in energy costs, transport and freight costs, labour costs, packaging and disposal costs, retailer margins, processor margins, PPE and hygiene, all of which have increased in price over the last year, along with almost everything else.”

“This is important to remember when considering when livestock prices increased as they did to historical highs last year. When saleyard prices were at those highs a year ago, retail prices increased but not at the same rate.”

“What we are seeing now is that same trend, just in the opposite direction. Consumers need a degree of certainty for their shopping basket and retailers smooth the retail pricing impact over the longer term, rather than sharply increase or decrease the price of meat in accordance with livestock prices.”

Do the ‘big two’ really dominate the fresh meat market?

Since attention started to surface four or five months ago on the growing gap between livestock and retail meat prices, words like ‘oligopoly’ (a state of limited competition) and ‘duopoly’ (a state in which two suppliers dominate the market) have frequently appeared in stakeholders’ opinions in reference to Coles’ and Woolworths’ fresh meat market share on social media, Beef Central reader comments and elsewhere.

However information published by the Australian Beef Association this week suggests the two national retailers’ share of fresh meat sales is not as dominant as what some may have suggested.

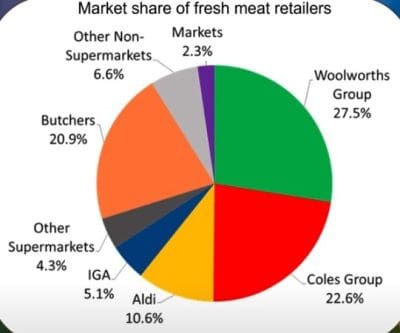

In this pie-chart published by ABA, the combination of Coles (22.6pc) and Woolworths (27.5pc) represent barely 50pc (50.1pc, to be exact) of all fresh meat sales, by volume.

In this pie-chart published by ABA, the combination of Coles (22.6pc) and Woolworths (27.5pc) represent barely 50pc (50.1pc, to be exact) of all fresh meat sales, by volume.

All other outlets represent a 49.8pc share –virtually the same as the ‘big two.’

In comparison, the combination of independent butchers (20.9pc) and Aldi (10.6pc) represent a market share significantly larger (31.5pc) than either Coles or Woolworths on their own.

Independent butchers have gradually lost fresh meat market share over the past ten years, Nielsen Homescan retail data has shown, but much of that has been absorbed by growing second-tier supermarket groups like Aldi, IGA, Costco and others, rather than Coles or Woolworths.

Woolworths market share for fresh meat appears to have changed little in the past ten years, while Coles has gained a percentage point or two, compared with early last decade when Beef Central still had regular quarterly access to Nielsen Homescan reports.