Click on image for a larger view

THE term ‘Burger economics’ aptly describes the current Australian slaughter cattle pricing situation, where meatworks cow values are now closer than they have ever been in percentage terms to the value of premium grass finished bullocks.

Multiple large regional saleyards selling centres across the eastern states this week have recorded heavy cow prices peaking at 440c/kg. They included Bairnsdale, Wagga, Wodonga and Roma, with Ballarat not far behind on 436c. At a generous dressing percentage of 52pc, that values those saleyards cows at 846c/kg carcase weight where they stand, before freight. Some of those Roma cows were bought by buyers where big freight bills are involved to get them home.

Compare this carcase weight c/kg price with grainfed 0-2 tooth 100-day ox being forward sold for November delivery this week at 730c/kg. Saleyards cows 116c dearer than grainfed ox? Hard to believe, but true.

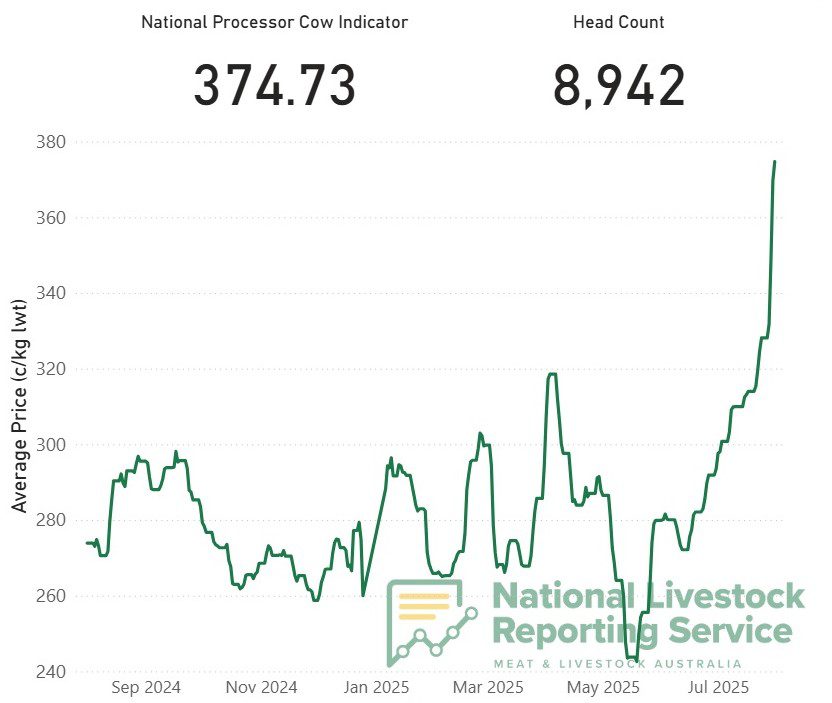

Yesterday’s NLRS processor cow indicator price of 369.3c/kg was up 45c/kg in a week, and almost 100c/kg higher than this time last year. Compare this with yesterday’s NLRS restocker heifer indicator at 362.6c, and for possibly the first time in history, heavy cull cows were worth more, c/kg basis, than heifer replacements.

NLRS Processor Cow indicator – July 2024-July 2025. Click on image for a larger view

The all-time record for the NLRS processor cow indicator came in October 2022, when the national beef herd was in full-on rebuilding mode and cows were as scarce as hens’ teeth. Today’s cow indicator level (374.73c) is just 3c/kg shy of the 2022 record (378c), yet cows in the north, at least, are reasonably plentiful.

The point is, cow prices at their current level are not an aberration happening at a single sale after a tussle between a couple of meatworks buyers – it’s somewhat consistent across sales in three states. Rain in the south has clearly added to the momentum. The large offering of about 1300 cows 520kg or heavier at Roma on Tuesday averaged an incredible 396c/kg liveweight. The top-priced pen of 600kg Santa cows from Glenolive, Injune sold for $2757 a head.

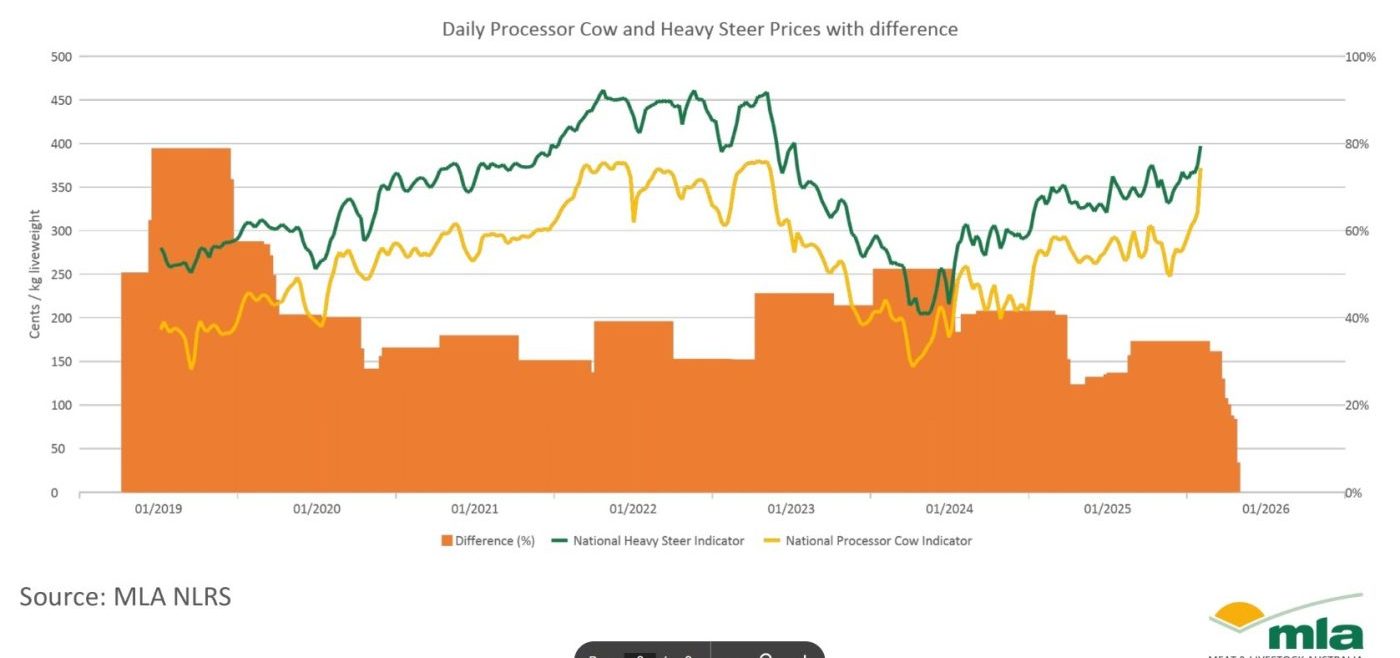

Beef Central asked MLA analyst Erin Lukey to prepare the graph published above, plotting the NLRS processor cow indicator (all cows +400kg sold to processors via NLRS reported saleyards) versus the heavy steer indicator.

It graphically shows that over the six-years covered in the graph, cows this week are the closest they have ever been to grass heavy steer values, at just a 7pc variance, worth around 40c/kg. What the graph does not show is that the steer-over-cow ‘premium’ is in fact at its lowest point in history – covering all NLRS data stretching back 25 years, to 2000.

The orange shaded area at the bottom of the graph reflects the percentage price difference between meatworks cows and grass heavy steers, falling away to just 7pc this week.

All this suggests one thing: quality is currently secondary to simply ‘getting meat in the box.’

‘Four legs and a tail’ beats meat quality

So how can processors be paying so much for meatworks cows in saleyards at present, in comparison with younger, heavier four-tooth grass ox, for example?

The best explanation for the current phenomenon we’ve heard was this succinct summary:

“In times like this, the processors’ specification changes. The animal they buy must have four legs and a tail,” one exporter contact said yesterday, with a touch of irony.

Effectively, what he is saying is meat quality is currently being trumped by “simply getting a carcase on the rail.”

“Southern processors, particularly, need a body on their kill chain, and they have very few to choose from at home. There’s money to be made simply in weight, so their best choice is the cheapest body they can buy – and right now, that’s still cows.”

“The attitude is: we just need to kill SOMETHING; bone it, and put it in a box. But when too many processors pile-on, like they are at present, it forces up the cow price, relative to other categories like grass heavy steer and bullock.”

Lean trimmings price continues to surge to records

Clearly supporting the momentum in cow prices at present is the 90CL imported beef price in the US, which last week for the first time in history broke through A1100c/kg, in response to the growing shortfall in domestic US beef production.

“While the US beef industry is doing what it’s doing, it’s a pretty simple business: meat in box. And the big declines seen in the past two months in Brazilian beef exports to the US, ahead of Trump tariff intervention tomorrow, is only supercharging that,” the export trade source said.

Illustrating the impact of northern-sourced cattle on southern kills at present, Victoria’s seven-day NLRS kill last week of 27,200 head was up more than 24pc on the same time last year, despite the severe shortage of local killable cattle.

Illustrating the impact of northern-sourced cattle on southern kills at present, Victoria’s seven-day NLRS kill last week of 27,200 head was up more than 24pc on the same time last year, despite the severe shortage of local killable cattle.

Northern cows are a big part of that rise. While its true that all states last week were higher in production, year-on-year, none were anywhere near as high as Victoria. Victoria’s female slaughter ratio last week was 76.6pc, and has remained above 75pc since mid-June.

Southern states meatworks buyers have operated over the last week as far north as Clermont and Charters Towers sales in North Queensland, despite the fact that both are in ticky country.

There’s a lot of cows being pushed onto the northern market at present, not driven by any great seasonal influence or desire to sell-down, but simply because the money is so good, vendors cannot resist sending a few to market.

“If a northern cattle producer is deciding whether to put a cow around again for another year as a breeder, or sell her into the strongest slaughter market seen in four or five years, they are clearly taking advantage of the price,” MLA analyst Erin Lukey said.

In summary, all this represents one of the craziest phases in the Australian beef supply/demand cycle that Beef Central has seen in the past 14.5 years this business has been running.

- MLA’s Erin Lukey will present on the current state of the cattle market at Townsville’s Young Beef Producers seminar on Friday.