BIG changes have occurred over the past decade in the way the US beef industry sells feedlot cattle, US economist Ted Schroeder told yesterday’s Australian Meat Processor Corporation conference in Sydney.

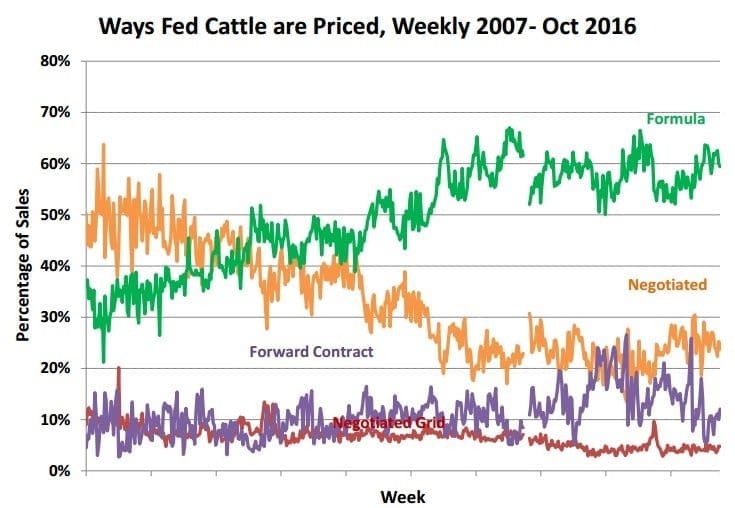

As the accompanying graph shows, so-called ‘formula’ price arrangements(green line), involving longer-term supply agreements of some kind for finished cattle sold by feedlots to packers, has grown from around 30 percent of total fed cattle sales in 2007, to around 60pc today.

The discussion was one of numerous references made during the AMPC conference about the need for greater value-chain integration across the red meat industry.

Prof Schroeder said what motivated the move in the US industry was a need to better coordinate what’s happening at the feedlot with the needs of the packer.

“Ten years ago, those same feedlots and packers were in a much more adversarial relationship, in terms of pricing. But the most important thing that has emerged from formula marketing relationships has been a more collaborative environment between packers and feedlots.”

Prof Schroeder said what got displaced in the rise in popularity of ‘formula’ pricing in the US over the past nine years was ‘negotiated’ selling (yellow line on graph), which has fallen from about 50pc of all fed cattle sales to 20pc over the same period.

“What ‘negotiated’ refers to in the US, typically, is when a feedlot lists its market-ready cattle out on a ‘show-list’ each week to prospective buyers, and then tries to attract packers to make bids on those cattle,” he said.

“By the end of the week the feedlots hope to have secured a bid on those market-ready cattle that’s acceptable, and the cattle are delivered the following week. It’s a system that’s been used in the US industry for many years, to exchange cattle with dollars.”

But while there were some good aspects to ‘negotiated’ selling, it also had its challenges.

“Firstly, it engages both the buyer and seller in price discovery. Feedlots and packers are talking with each other, day-to-day, and negotiating price. Much information is flowing into that process. As a seller or a packer buyer, you can’t afford not to be informed. Anybody who is not, does not last very long, in a very competitive industry.”

But over time, many US feedlots started seeing ‘negotiated’ selling as a costly and cumbersome process, Prof Schroeder said.

“Some weeks they might not get their cattle sold, and when that happens and they are on full-feed, next week the cattle are 25 pounds (12kg) heavier, and suddenly the leverage swings to the buyers. Feedlots found it cumbersome, and when caught with backed-up cattle, processors could take them to the cleaners.”

“Feedlot started to say, I can find a better way to do this, that’s not so costly, and does not leave them with the worry about whether their steers are sold this week or not. Especially as the industry was in a long decline in herd size, packers, also, were finding it costly and inefficient to rely on ‘negotiated’ cattle.

So they moved from negotiating week-to-week, to forging longer-term agreements to purchase all a feedlot’s cattle, with a negotiated long-term price formula, including premiums and discounts on quality.

“In many cases it was a whole year’s transactions, with both sides knowing how many cattle are delivered every week or fortnight,” Prof Schroeder said.

“It made a lot of sense, and the feedlots recognised that by doing this, partnerships could be formed whereby quality premiums and discounts could be built into the pricing relationship. The opportunity was there to get paid more for that relationship, because the feedlot had figured out how to produce cattle targeted specifically at that packer’s grid.”

This increased coordination had had substantial impact on the US fed cattle industry –both positive and negative, Prof Schroeder said.

One of those trade-offs has become very acute right now.

“What happens when you start formula pricing so many cattle, that your cash-negotiated price that is used as the base price, becomes so thinly traded?” he asked.

“That happens to the point where sometimes, stakeholders do not even trust the negotiated price as a good representation of what the market supply and demand fundamentals that week are. We are currently in that phase,” he said.

“Texas, the largest US feedlot state, for example, currently has no price discovery, for this reason. They formula price everything.”

In Kansas, another very large US feedlot state, negotiated cattle serving as the reference price are currently at about 15pc – very thin.

“But this transformation has dramatically changed the US industry. Through this process, producers now realise they can go downstream, and create their own relationships with food service and food distribution companies – and they have. As soon as they did that, packers started to become, in some cases, cost centres in the whole vertical supply equation – not necessarily the driver of the whole process.”

Prof Schroeder said he thought this development would continue to have major ramifications for what the US beef industry looked like, how it produces beef, and who it produces for.

Regulatory scrutiny delivers uncertainty

He, however, that right now, the ‘formula relationship’ that had developed across the US industry was under some ‘subtle’ regulatory stress.

The USDA’s GIPSA regulatory body is responsible for regulating the competitiveness of the livestock industry. Current US law says that if a feedlot and a packer get in a marketing relationship, and other feedlot contends that that relationship is in some way harming their interests, they have to legally prove that their market is being negatively impacted in order to mount a case.

But if a proposed change to regulatory arrangements comes into play, there will no longer be any need for a complainant to legally prove damage, in order to sue for damages under such a claim.

“In particular, our USDA currently has a policy that is in development that could put these relationships at significant risk,” he said. “So what this movement looks like two years from now, I don’t know – it is going to depend upon the regulatory outcomes that emerge from the new Trump administration.”