There’s a growing stockpile of beef in cold storage in Australia’s key Asian export markets – due largely to the slowdown in local economies – and in some cases it might take six months to clear.

All three key Asian markets for Australia – Japan, Korea and China – are impacted, and the overhang is likely to have implications for Australian export beef demand.

That’s the assessment of independent analyst Simon Quilty from Global Agritrends, who has addressed a series of industry seminars recently, including an Elders agency network gathering in Rockhampton.

That’s the assessment of independent analyst Simon Quilty from Global Agritrends, who has addressed a series of industry seminars recently, including an Elders agency network gathering in Rockhampton.

In recent weeks global markets had looked slow, Mr Quilty said, and with that slowness came the concern of larger inventories building up, which anecdotal reports suggested is happening.

If overseas inventories failed to decline or disappear, Australian livestock prices could move even lower as exporters struggle to place meat products, he said.

But conversely, if overseas inventories cleaned up, this could lead to higher export prices and market support in Australia, Mr Quilty said.

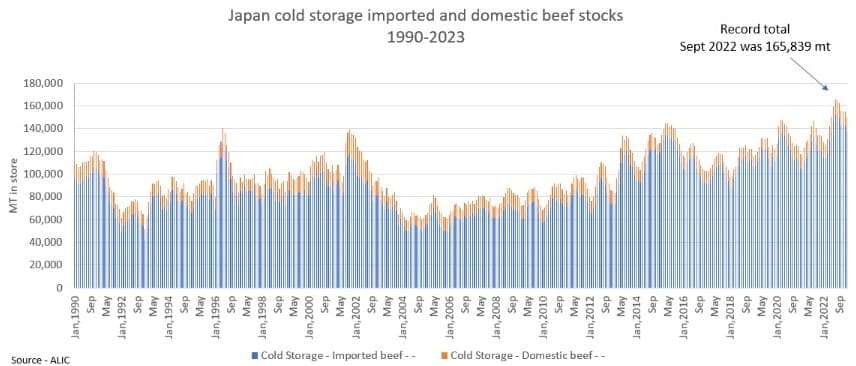

Japan’s cold stores at record levels

Latest data out of Japan has Japanese beef stocks moving higher as the challenges of Asia’s large inventory intensified, he said.

“In the last few days, new April data from Japan’s Agriculture and Livestock Industries Corporation has shown that beef stocks, both imported and domestic, have jumped 7pc on the previously published figure, and now sit 21pc above the five-year average,” Mr Quilty said.

This beef inventory figure was the fourth largest in Japan’s history at 160,000t, with the peak occurring last September at almost 166,000t.

“What is concerning is the trend reversal of falling beef stocks over the last six months and the spike in beef inventories in April,” Mr Quilty said.

“This points to ongoing challenges in Japan of retailing beef in a slowing economy.”

He suggested the recent beef inventory figures for Japan showed it was likely to be at least six months before any sign of a significant reduction of beef stock will occur, with April’s volume increase implying it could be closer to nine months before any actual reduction in volume takes place.

When looking at imported and domestic Japanese beef stocks since September last year, storage levels had been at record levels for the last ten months, Mr Quilty said.

The worst was felt in January, and as a result, shipments were delayed, containers were held at ports, and demurrage became commonplace.

The extensive inventories meant Japan’s ability to take additional beef would be limited, Mr Quilty said.

“There are minor signs of cold stores starting to reduce volumes, but it’s very marginal, and the concern is that Australia’s increased beef supply will outstrip demand. Some of the congestion has been cleaned up in the last month, and the product is moving easier, but the market remains subdued,” he said.

In addition, beef consumption in Japan had remained low, falling close to a 33-year low at 178g/head/month, almost three times less than chicken and pork consumption, reflecting beef’s high costs compared to the chicken and pork.

As a result of the backlog, Japan importers were buying hand-to-mouth, hoping that import prices will ease, domestic demand will pick up, and more space will become available.

“So far, Japan’s domestic demand remains quiet. Higher US beef export prices and less US beef export volume work in Australia’s favour, but Japan buying interest remains subdued and is likely to be this way for the next three to five months,” he said.

When asking a Japanese importer what would turn Japan’s market around, Mr Quilty said his answer was ‘China’; for several reasons:

- China would take any excess product from Australia, create additional competition, and tighten global beef supplies

- This, in turn, would see Japan work through its inventories without additional stock pressure and give it time to restore balance to its inventories.

Korea’s cattle inventory at near record levels

Similar stories were evident about Korea and heavy cold storage stocks in the country, Mr Quilty said, although hard statistical data was hard to come by.

“However the lack of bids being fielded by Australian exporters, and the buying hand-to-mouth supports the high-frozen stocks theory,” he said.

What was known is that Korean cattle inventories are high and up 25pc in volume since 2016, with the total herd peaking last September at 3.7 million head.

As documented in the last few months, a government incentivised herd liquidation program has been implemented.

With such a high inventory in early 2023, Korea’s Ministry for Agriculture, Food and Rural Affairs (MAFRA) announced it wanted to cull 140,000 head of Hanwoo cows from the national herd. The reduction plan was then allocated to different provinces, with the culling to occur among farms with more than 100 cows. There have been two cullings to date, totalling about 30,000 head.

There was still 110,000 head to be culled, which would not occur in the February to June window and is likely to be extended to the end of the year, placing more pressure on the high-end beef market, Mr Quilty said.

The immediate culling impact had seen more Korean people afford to buy Hanwoo at the retail level, and prices have also been subsidised by the Hanwoo Association, making it more affordable.

However, the macro factors surrounding meat sales in Korea had also been significant, Mr Quilty said, with a slow economy that has not favoured general consumption.

In the past, business entertainment was also an important market for high-end beef, but since and during COVID, this business has been subdued.

Korea’s Development Institute (KDI) revised the nation’s economic growth in 2023 downward, from 1.8pc to 1.3pc due to high inflationary pressure.

Korean import volumes from Australia and the US recently had been healthy, but cheaper.

“A slow economy has dampened consumer demand and is seeing a need for lower priced imports,” Mr Quity said.

China’s inventory issues are at ports and potentially within

Elsewhere among Asia’s ‘Big Three’, exporters to China continued to talk of slow demand and high beef inventories that are seeing slow movement in imported beef, he said.

There were two inventory issues in China: Brazilian beef containers sitting at ports that cannot enter China, and excessive volumes of excess stock within China itself.

Recently, Brazil’s President Lula asked China’s President Xi Jinping to clear an estimated 70,000t of stranded Brazilian beef sitting at Chinese ports.

The stranded product is a direct result of the BSE case reported in February this year, and a self-imposed embargo was placed on Brazilian beef into China, which lasted 28 days.

“The issue is that the stranded product dates before the BSE notification date, which continued to be shipped at the time,” Mr Quilty said.

All product post this date was being shipped and received without issue.

The 70,000t of product that has yet to be entered has also not been paid for, creating cash flow problems for exporters who own stranded cargo, he said.

Large frozen inventories within China

Anecdotal reports of several million tonnes of frozen beef sitting in warehouses had not been substantiated, Mr Quilty said, as food stocks within China were a secret closely guarded by the Chinese government.

“But China-based beef analysts have said they have heard similar numbers. In addition, they said that stock was putting great pressure on the existing spot market for beef – especially that there was lots of frozen stock with a shelf-life of more than one year. Some supply chain financing companies must clear stocks at a lower price,” he said.

“Market participants say that bids out of China remain low and that importers are reluctant to bid too far forward.”

The slow China economy and the unexpected lack of ‘revenge’ spending had seen a slow food service sector in China for the last six months.

In recent weeks prices had improved from the lows experienced in February this year, but from a low base after a 27pc fall since July’s high last year.

“A slow economy has been attributed to much of this price fall,” Mr Quilty said.

US cold store volumes are low

On the other side of the Pacific, US cold store volumes in April were low – down 6pc from the previous month and 16pc compared with April last year, he said.

This reflected lower imports and exports into and out of the US this year.

This year’s beef imports from all destinations to the US are down 5.7pc compared to 2022, and US global exports were down 9.5pc for the same period. Both imports and exports rely on cold storage facilities.

“So the issues of high cold storage inventories that Asia is experiencing are different in the US, where inventory numbers are down, and excess capacity exists on the US west and east coasts,” Mr Quilty said.

Unlike Korea, the US had been significantly liquidating its cattle herd for the last three years due to drought, and is likely to see close to record lows in the US cattle inventory over the next three to four years when rebuilding occurs.

“The market is waiting for the rebuild to start, and with that, an expected tightening of supply and a dramatic need for imported meat to fill the domestic void,” he said.

“But the role of the US as both a customer for Australia and a competitor globally cannot be understated. In some respects, the tightening of US exports into Japan, Korea and China will potentially impact Australia more than the lift in the US domestic market alone. Australia and the US dominate the grainfed space globally, and when US grainfed supplies tighten, only Australia has the volume to fill that void.”

So, as US export beef supplies tighten, it is assisting in taking the supply pressure off the key markets of Korea, Japan and China and creating market space for Australian beef. This has been occurring this year and will likely continue for several years, Mr Quilty said.

“When will the US beef rebuild occur? This is the 64-dollar question, and it depends very much on rain, but what’s clear is that the area of impact has shrunken considerably, and now only 16pc of the US is in drought. Unfortunately, that is mainly in cattle regions.”

It was worth noting that the recent drought exceeded 40pc of the US land area for a record 132 weeks during 2020-2023. The next closest extended drought period was 68 weeks in 2012-2013 and 65 weeks in 2002-2003.

The other important phenomenon was that herd liquidation may continue in the US even after rain, Mr Quilty said.

This was seen in Australia in 2020 when female kills remained above 47pc for almost another year. Several reasons have been attributed to this: record cattle prices were experienced then, and farmers needed the cash flow given the large amounts of money and debt from the high cost of feeding over the previous three years.

“In short, they needed to pay the bank back. Secondly was the non-performing breeding stock due to the severity of the drought. In the first 12 months after any severe drought, the reproductive ability of animals is still recovering, so ‘empties’ were not uncommon, and these also went to market.

Should this also occur in the US, it may prolong liquidation by another three to six months, Mr Quilty said.

Importance of China as an alternative to Japan and Korea

Mr Quilty said the US (customer) market could only fix some problems when taking surplus product out of Australia due to the current stock build-up in Asia – but not all.

“There are certain items that Asia takes, and the US does not, or it is in very small quantities. So should Japan and Korea remain quiet for the balance of 2023, China will play a crucial role in taking any surplus product – in particular, blades, brisket, chuck roll, shin/shank, outsides and knuckles.

The US played a crucial role in manufacturing meat and high-end items such as striploins, ribeyes, rumps and tenderloins, but, they could only take some items.

Global meat beef prices have firmed

The latest Food and Agricultural Organisation meat prices have shown a continued lift, with May prices lifting 1pc, the fourth consecutive month of rises this year.

One of the key drivers has been poultry prices, with strong demand in Asia and limited supply due to Avian Flu outbreaks, Mr Quilty said.

Pork prices also rose for the fourth month in a row, albeit at a moderate pace, as global supplies tighten. Global bovine prices also edged higher with tightening export prices from the US, keeping beef prices slightly elevated.

“The issue is that these prices reflect a broader spectrum of items, including the cheaper and more expensive ends, and may therefore indicate a greater demand for ground beef but less demand for expensive items,” Mr Quilty said.

Even with this improvement in beef prices on a global basis, this is driven by China coming off its lows, and the US. Exporters were saying that Korea and Japan prices still remained flat and subdued, he said.

Impact Australian cattle prices?

On the surface, it would seem that three of Australia’s key export markets out of four are currently ‘not firing’, and were ‘full’, Mr Quilty said.

The added concern was that with potential drier conditions in Australia and increasing beef shipments, these markets will not be able to absorb this additional beef – in other words, supply outstripping demand.

“The supply tightness in the US is inevitable. It is just a matter of timing, this could occur within three months or, worst case scenario, by the end of the year, but either way, 2024 will see prices start to move significantly higher,” he said.

The evidence in Japan and Korea pointed to three to six months of working through inventories and cleaning up excess stocks, whether boxed beef or excess cattle (such as in Korea).

“If we relied on the US as the only saviour, Australia would be vulnerable with too many eggs in one basket,” he said.

“But as said earlier, the US cannot take all products, and therefore China must remain in the picture as a buyer.”

“China remains the critical player. Should its inventory be lower than expected, its ability to pull products away from Japan and Korea will be critical in ‘cleaning-up’ these markets.”

“The 70,000t on the wharf is a concern, but the slowing down of monthly Brazilian shipments, since this dispute began, will help tighten supply in China.”

Mr Quilty said he saw two possible scenarios:

- Worst case scenario: China, Korea and Japan remain full and take the balance of 2023 to clean themselves up, while Australia’s beef exports continue to increase as dry conditions prevail. The US drought liquidation continues due to continued dry conditions in cattle areas and possibly a need for cash flow even if the rain does come. “This is the worst case, and Australian cattle prices could take another leg down due to oversupply in critical markets if this plays out,” Mr Quilty said.

- Best case scenario: The US drought breaks soon, the rebuild starts immediately, and supply tightens in all markets. China cleaned up its excess beef quickly and starts to fire, and Korea and Japan also started to buy again. “In this scenario, cattle prices will hold. I don’t think they will rally but hold until late 2024,” he said.