That activists can effectively blackmail “skittish financial organisations” to withdraw financial services to law-abiding businesses is of grave concern to Australia’s economy, a joint Parliamentary Inquiry was told yesterday.

The joint standing committee on Trade and Investment Growth, which is conducting an inquiry into the prudential regulation of investment in Australia’s export industries, has held public hearings in Canberra over the past two days.

The issue of financial organisations that choose at the behest of activist groups not to lend to certain law-abiding businesses, such as those operating in the livestock export, intensive farming or coal mining sectors, has been a key topic of dicussion during the hearings.

Red meat industry representatives have told the committee that banks and financial service providers who selectively choose not to lend to legitimate, law abiding businesses should also lose their privileged right to taxpayer guaranteed deposits through their banking license.

Thin edge of the wedge

John McKillop appearing via video link to yesterday’s public hearing.

Red Meat Advisory Council independent chair John McKillop said the issue was extremely important for the red meat sector, because, without access to finance and financial services products, “we cease to exist”.

But the broader economy should also be concerned about minority groups trying to dictate who can and who can’t do business.

“Minority groups will move on to the next issue and the next issue until there is no livestock sector, and when there is no animal husbandry left in Australia, they will move onto the next target,” he said.

“We need to sort this out as a nation before it gets to that point where minority groups are dictating policy.”

Australian Livestock Exporters’ Council CEO Mark Harvey-Sutton said members were reluctant to speak on the record for fear of future reprisal from financial providers but anecdotally had documented many cases where they had been unable to access finance, insurance or even to open a holding account.

“Some of the companies are NAB, CBA, ANZ bank and surprisingly even Telstra,” Mr Harvey Sutton said.

“We are firmly of the view this is the outcome of an activist agenda that is utilising the ESG investment trends as a vehicle to drive these policies.

“Generally the advice that we have seen that informs these ESG investments us misinformed and developed without the input of industry.

“Last time I looked there was nothing unethical about underpinning livestock prices, supporting regional communities and supplying food security to thousands of people in our markets.”

‘Last time I looked there was nothing unethical about underpinning livestock prices, supporting regional communities and supplying food security to thousands of people in our markets’

One company that was prepared to speak publicly was livestock shipping operator Wellard which called out the actions of Australia’s banking institutions in a strongly worded written submission to the inquiry.

Wellard criticises bank ‘hypocrisy’

“It is of grave concern that given the importance of exports to Australia’s economy, coalitions of activists can effectively blackmail skittish financial organisations to achieve their ideological agendas through both the withdrawal of funding and provision of financial services,” Wellard executive chairman John Klepec wrote.

The live export industry operating in Australia was legitimate, lawful and regulated to the world’s highest standards, but companies such as Wellard had experienced first-hand where certain financial institutions had refused to conduct business with itself and other livestock exporters.

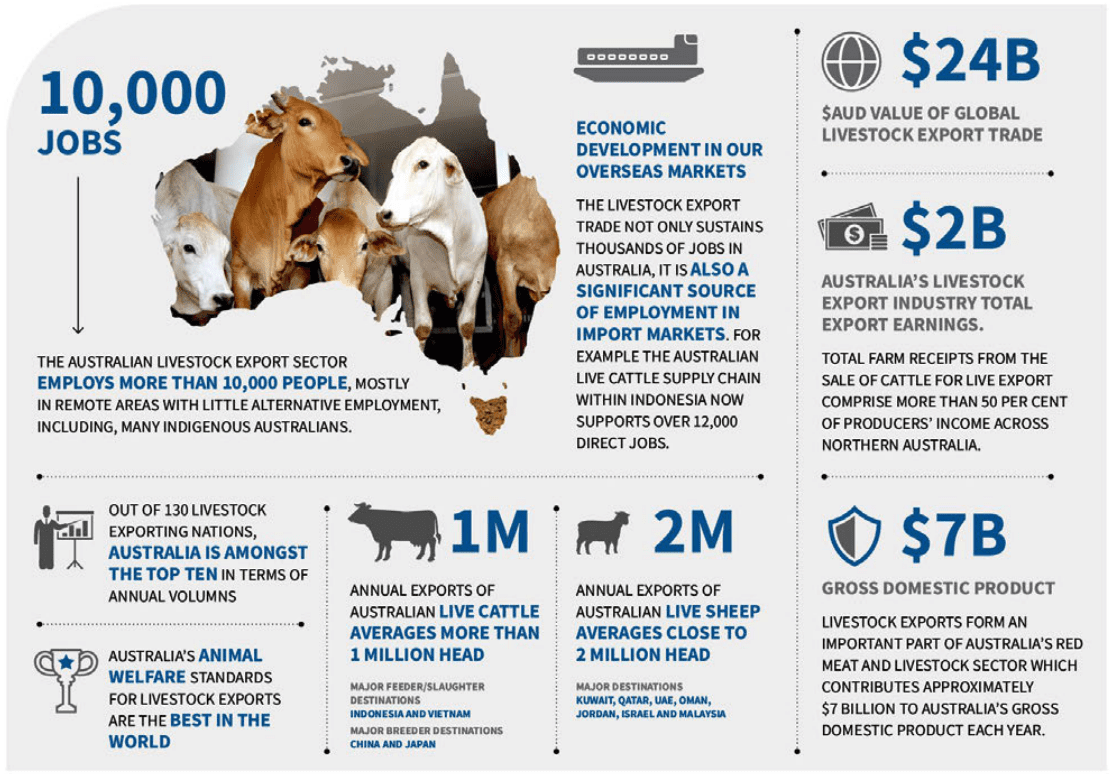

An infographic included in the Wellard submission outlining the economic importance of live exports to the Australian economy.

In 2018 he said the company was provided notice by CBA that within 12 months, it would no longer extend credit to Wellard. Additionally, Wellard was required to close its everyday banking facilities, including trading accounts and credits cards at CBA.

“Our Company was experiencing some financial difficulties at the time, so the refusal to extend credit could be characterised as a business decision.

“It is clear to Wellard, however, that the withdrawal of all banking services by CBA was clearly a choice made by the bank based on the type of industry in which Wellard operates.

“Wellard’s discussions with other Australian banks – including NAB, Westpac, ANZ, and BankWest (owned by CBA) – all resulted in a refusal to service the Company with even an everyday operating account.

“It was clear in each of these discussions that the refusal was based on each bank’s credit committee and policy settings, which specifically exclude live export.

“It should be noted that when Wellard was interacting with these Australian banks, it had conducted a very extensive financial restructure, and was cash-at-bank positive, with zero bank debt.

“Notwithstanding this, many Australian banks would not open an account and accept a cash deposit from Wellard.”

Mr Klepec said it was “incredibly frustrating” that financial institutions effectively positioned themselves as “moral arbiter”, refusing to do deal with legitimate, legal businesses.

“There is considerable hypocrisy attached to that position. Financial institutions proudly proclaim their agribusiness heritage and market share in rural areas, providing bank and finance to farmers and station owners whose income is generated in part or in whole from supplying the live export trade, but then refuse financial services to companies involved in that sector’s supply chain logistics.”

ALEC CEO Mark Harvey-Sutton speculated that banks feared “perception from community” but disappointingly did not appear to be prepared to take on further information or industry input to inform their policies and decisions.

Mark Harvey-Sutton

When challenged, banks tended to engage in “virtue signalling” by pointing to their considerable investments in Australian agribusiness.

However, he said, this view carried a certain hypocrisy because it ignored the extent to which the live cattle sector underpinned much of their huge agribusiness portfolios.

Wellard’s recommendation, similar to RMAC’s recommendations (outlined below), is that in return for that Government support, there should be a Universal Service Obligation (USO) whereby Authorised Deposit-taking Institutions (ADIs) must provide a minimum level of service to Australian taxpayers and corporations who are conducting legal business in full compliance with Australian laws.

It also of the view that activists seeking to impose their ideologies on financial institutions are effectively engaging in secondary boycott conduct, which is prohibited under section 45D of the Competition and Consumer Act 2010, and urged the Australian Government to direct the ACCC to investigate the issue. (RMAC wrote to the ACCC requesting an investigation earlier this month).

“It is important that financial institutions are not coerced or weaponised in the campaign by animal activists to shut down a legal, law-abiding industry which is so important to rural Australia, but that they do not accept,” Mr Klepec wrote.

In its submission to the inquiry RMAC on behalf of the Australian red meat sector suggested the committee consider three specific recommendations:

– the Commonwealth Government ceases commercial dealings with financial service providers that don’t support law-abiding businesses;

– the Commonwealth Government issues a statement of intent to be a financial service provider of last resort for law-abiding businesses in instances of market failure; and

– the Commonwealth Government annually reviews all financial service providers who are reported to have refused service to law-abiding businesses.

Mr McKillop also put forward that if financial service providers want to selectively choose to whom they lend, then they should not have the taxpayer guaranteed deposits through their banking license.

“The issue really comes around that mutual obligation,” he said.

“If as tax payers we are obliged to support the banks through the guarantee of their deposits then I think that needs to be reciprocated with their obligation to support law-abiding businesses, rather than picking or choosing.”

Is this curtailing free markets?

In response the Deputy Chair of the committee, ALP MP Ged Kearney, challenged that position by asking “surely that is just an indication of how the free market works?”

Mr McKillop said every bank, or any other business, had the right to choose who they do business with and who they don’t.

But the difference in this case, he said, was that this was a business (a bank denying service to a law-abiding business) that relied on taxpayer’s guaranteeing its payments.

“Therefore, when you are issued with a banking licence in Australia, it’s a privilege that comes with some obligations.

“So I would be more than happy to support them not having a banking licence with a bank guarantee and choosing to do business with who they wish to, but, if they want the privilege of that guarantee, they need to come back and have that mutual obligation.”

Mr Harvey-Sutton added that there was “no intention to curtail the free market here”.

“All we’re asking for here, in my view, is for transparency to be applied to how these internal policies and decisions are made. As an industry, quite rightly, there’s a high expectation of transparency from us. All we ask is that that works both ways.”

Bank Association challenges guarantee perspective

In an earlier session Australian Banking Association CEO Anna Bligh challenged suggestions that if banks are not funding certain sectors they should not get access to an Australian government guarantee.

Anna Bligh

“I think it’s really important to understand which guarantees banks have,” Ms Bligh said.

“Firstly the deposit guarantee, which is a guarantee by the federal government, is not a guarantee to banks; it is a guarantee to depositors.

“It basically means if the bank that you bank with falls over then you will get from the Australian government a maximum of $250,000 depending on what deposit you have. So it’s a protection for the depositor, not for the bank..”

Asked if there was an obligation in other countries where the guarantee exists for banks to lend to every sector, Ms Bligh said she was not aware of any jurisdiction where there is a legal obligation on banks to lend to any business or any sector.

“Certainly, all of the countries with whom we would trade—particularly, the countries in the OECD—are based on a risk based system that makes an assessment on the basis of the creditworthiness, the commercial viability and the serviceability of the customer, and I think they would all be very alarmed if Australia were to move away from that.”