Simon Quilty

In this discussion paper, independent analyst Simon Quilty looks at the impact of drought on the cow market – both livestock and meat.

AS THE drought has intensified in the last few months I have been asked a number of questions on what impact this drought will have on various parts of Australia’s cow market – both as livestock in the saleyard as well as in boxed meat in our export markets.

I’ve tried to answer the following difficult questions:

- What is the likely cost for a breeder to buy back cows once the drought has broken?

- Is the Australian drought going to see cheaper cow meat go to the US market?

- Have cow markets been impacted by the global trade war?

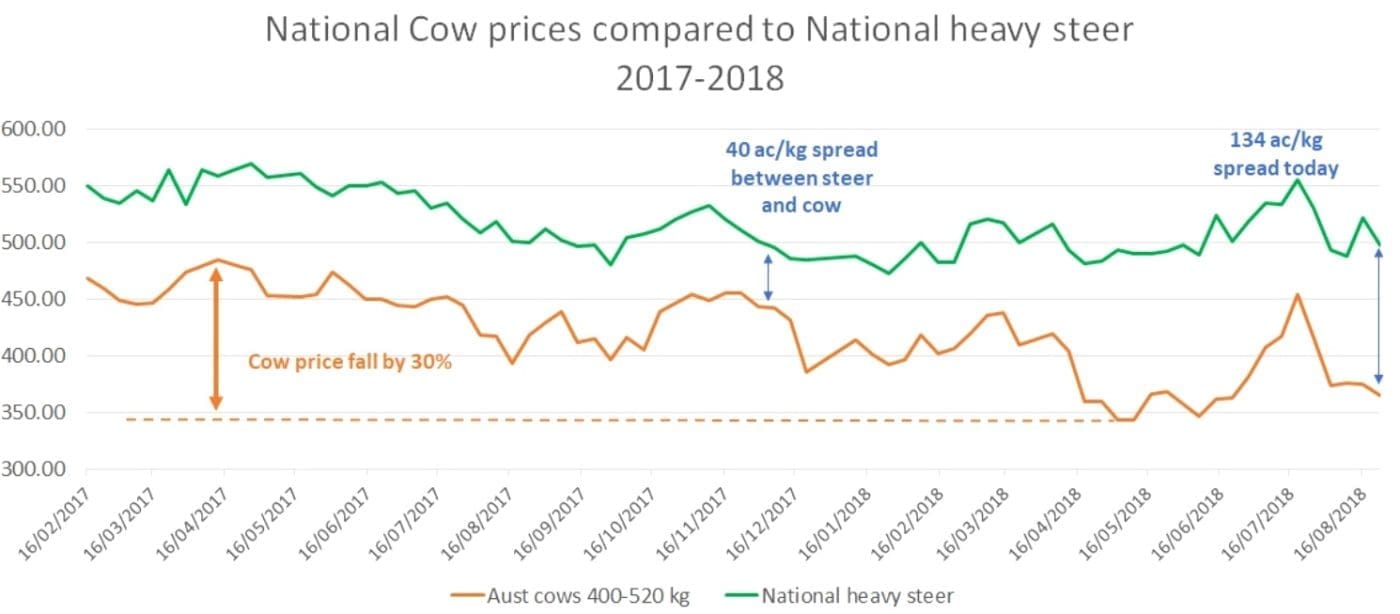

As a result of the drought impact, cow prices have fallen twice as much as steer prices since early 2017, with cow saleyard prices 140c/kg lower compared to a heavy steer price fall of 66c/kg.

Looking back at the previous 2013-14 drought, national cow prices doubled in the following two years, with cow prices which averaged 272c/kg CW in the drought jumping once rain came to 540-555c/kg range in the June to August period in both 2015 and 2016.

Prior to the post-2013-14 drought’s meteoric cow price rise, previous droughts when broken had seen only 15-40pc increases in cow prices during the following herd rebuilding years.

I attribute the dramatic cow price rise post 2013/14 drought to two reasons:

- Firstly, the 62pc increase in global beef prices that had occurred since 2010 that had not been built into Australia’s livestock prices at that stage, and

- Secondly, the dramatic liquidation of the national herd which saw over 2 million head shed from the herd due to drought.

I believe that due to the liquidation of such a young herd in Australia today, and the potential increase in global prices in the next 3-5 years, that these two factors will add another 10pc to the traditional post drought cow price improvement range. This puts my estimate on where cow prices could go to 25-50pc higher from today’s drought-affected cow price of 380c/kg to potentially 475-570c/kg CW when the drought breaks.

Recent lower prices into the US grinding meat market is more to do with Q3 being traditionally a slow time of year for demand, rather than the impact of the Australian drought. This weakness is because the market is between two key demand periods – Chinese New Year buying which is likely to start in October, and the finish of the Northern Hemisphere summer demand period whereby we are seeing beef inventories being wound down and demand is slow.

The Australian drought is not driving Australia’s imported 90 CL price to a discount to US domestic fresh 90’s – instead we are in a regular seasonal price movement that is likely to see Australian 90’s move to a premium to domestic 90’s within three months.

Australian cow cuts exports are 15pc higher and cow grinding meat is only 5pc higher in Q2 – in other words the additional drought-driven cow cuts are no longer being slashed and downgraded into the grinding meat pack, but are being sold as whole-muscle meat to other markets paying a premium over the US for these items, in particular China. This trend is unlikely to change.

Currency impact

The greatest impact on Australian beef exports due to the global trade war has not been the impact of tariffs or pork duties, but currencies – more importantly the currencies of our supply competitors and our key demand countries. Duties on other meat products such as pork and beef will have some affect, but this may not be felt for at least 6-12 months whereas currency influences are immediate.

Australian cow cuts due to currency uncertainty within key demand and supply countries are much more vulnerable on both the buy and sell side of the market – much more so than Australian steer meat.

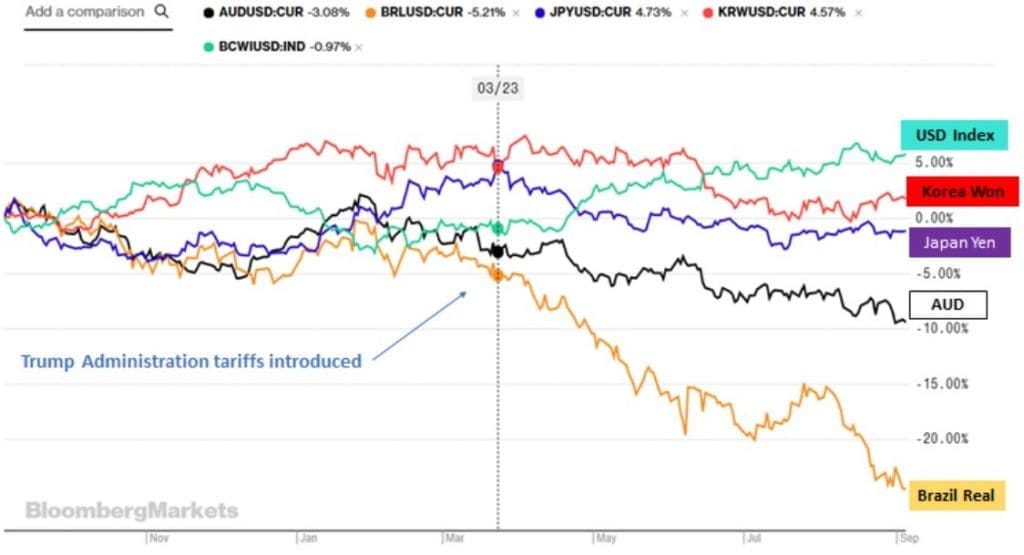

The most dramatic currency impacted has been Brazil, which has fallen 18.5pc since 23 March, while the Indian Rupee has fallen 8.3pc. In both instances each country competes with Australia into key cow meat export markets such as Indonesia, China, Hong Kong and Vietnam and in lesser cow markets such as Kuwait and Qatar – where the cheaper currency means they are far more competitive.

Thankfully, neither Brazil nor India compete into US, Japan and South Korea for beef and this has seen both Australia’s steer meat exports and cow meat cuts be competitive against US meat due to the appreciation of the US$ by 6.7pc.

Note the price forecasts within this paper are my own personal views, and I would always advise readers to seek further advice when making decisions to buy and sell, whether its cattle or meat.

Australia’s drought – overview

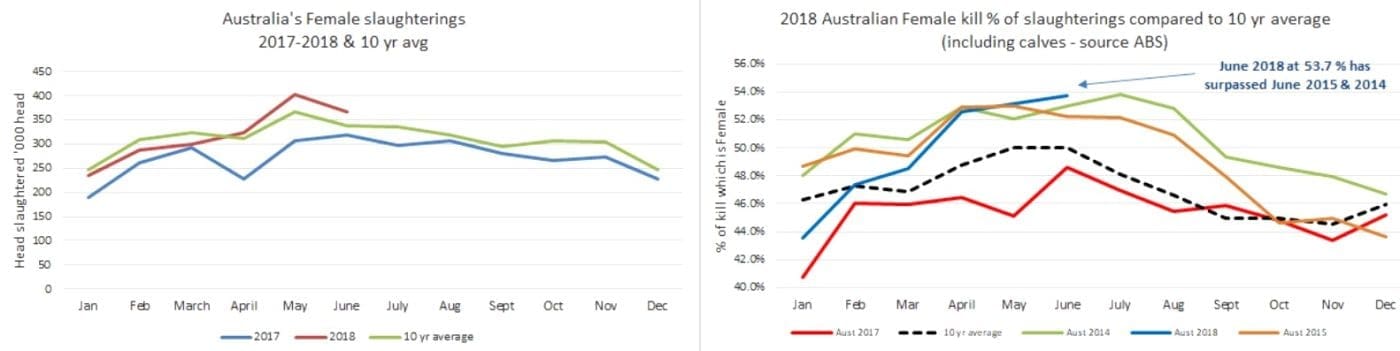

Australia’s drought is mainly occurring in NSW and QLD and given that these two states alone account for 63pc of Australia’s cattle herd, then it is not surprising the impact of this drought is felt across the entire Australian livestock sector. Australian total kills for 2018 year to date are 10pc higher than last year, with female kills up 20pc and male kills barely up 0.3pc. The herd in NSW and QLD is liquidating cows and the Australian cow market in one form or another is being impacted.

Click on images to enlarge

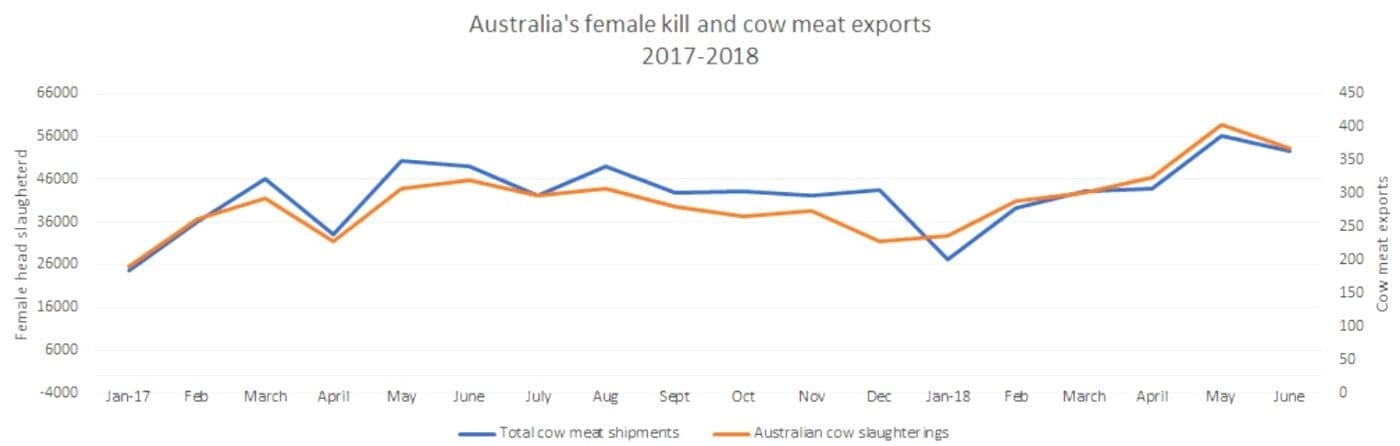

When assessing the impact of this cow liquidation on cow meat exports, I focused my attention on cow items that have the cypher ‘A’ and ‘C ‘- as cow products can be exported under either code (it should be noted that steer products can also be downgraded into the cypher ‘A’).

The graph below highlights that as the spread between cow and steer prices have widened, the volume of steers cuts being downgraded is getting less, with the ‘A’ cypher being more dominated by pure cow products. That is why the A & C exports below mirror the Australian more closely (higher correlation) as the drought has got more intense in 2018 (see graph below).

The volume of cow meat exports is up 15pc in the last three months and directly reflects the increase in the cow kill in Australia.

Question 1: What is the likely cost for a breeder to buy back cows once the drought has broken?

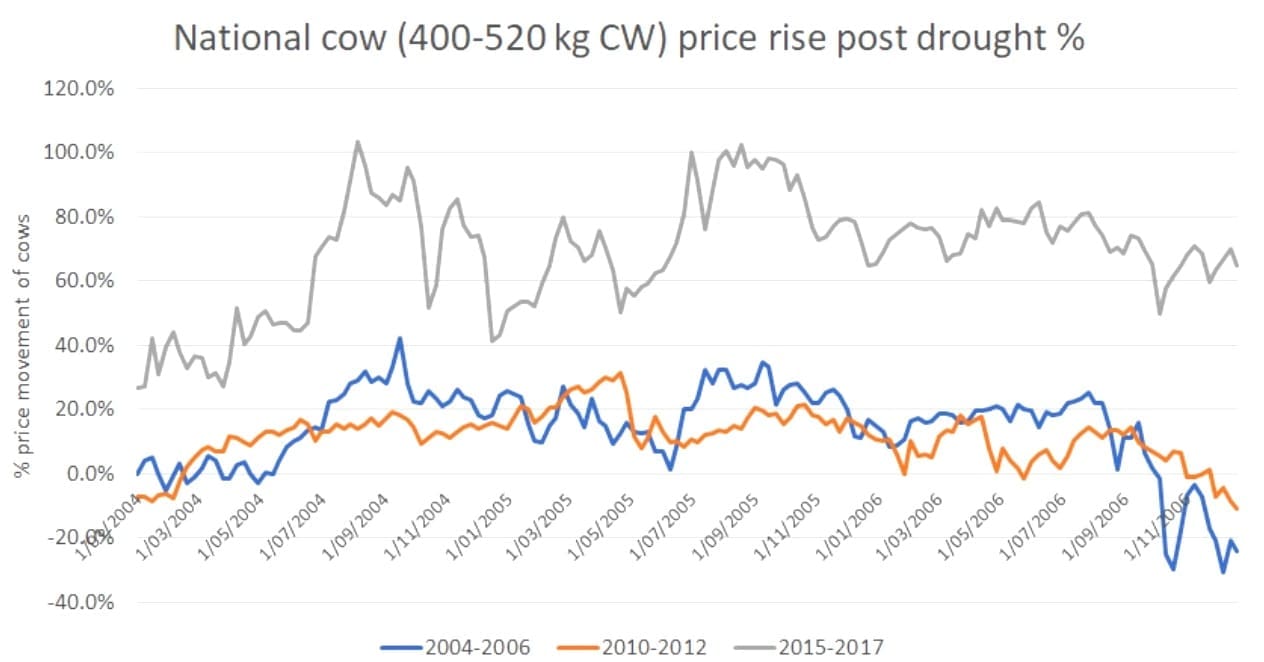

The simple answer to this question is cows will become very expensive once the drought breaks. To help assess the potential buy-back cost, I have looked at the previous three droughts and the percentage price increases that occurred, based on the average cow value during each respective drought versus the average cow value after the drought.

Cow prices have fallen twice as much as steer prices

The following graph shows that national cow prices have fallen 30pc in the last 18 months since the start of 2017. This graph also highlights the widening spread between heavy steers and cows – in short, heavy steers have fallen 66c/kg CW since early 2017 and in the same period cows have fallen twice as much by 140c/kg to 370 ac/kg. The narrowest spread was last November at close to 40c/kg which was the start of the QLD drought, and has widened ever since as grain and feed costs have got more expensive and pastures have deteriorated.

Source: MLA

Previous post drought cow price movements

When looking at the price movement after the last three droughts, the 2015-17 period stands out the most, whereby record cattle prices were experienced on steers and cows which came from a relatively low price base in the 2013-2014 drought which averaged cow prices of 272c/kg CW and saw cow prices double in value once the drought broke. The post-drought price peak occurring in the June to August period saw levels in the 540-555c/kg range.

The graph below highlights how earlier droughts had seen breeding cows on average increase by 15-40pc – the contrast of 100pc increase in 2013/14 is startling and can be attributed. I believe. to two reasons: the increase in global beef prices that occurred from 2010 onward which coincides with China’s entry into global beef markets as a significant buyer, and secondly, the dramatic liquidation of the national cow herd which saw more than 2 million head being shed from the total cattle herd. Both factors contributed to the sharp rebound in price levels in 2015 and 2016.

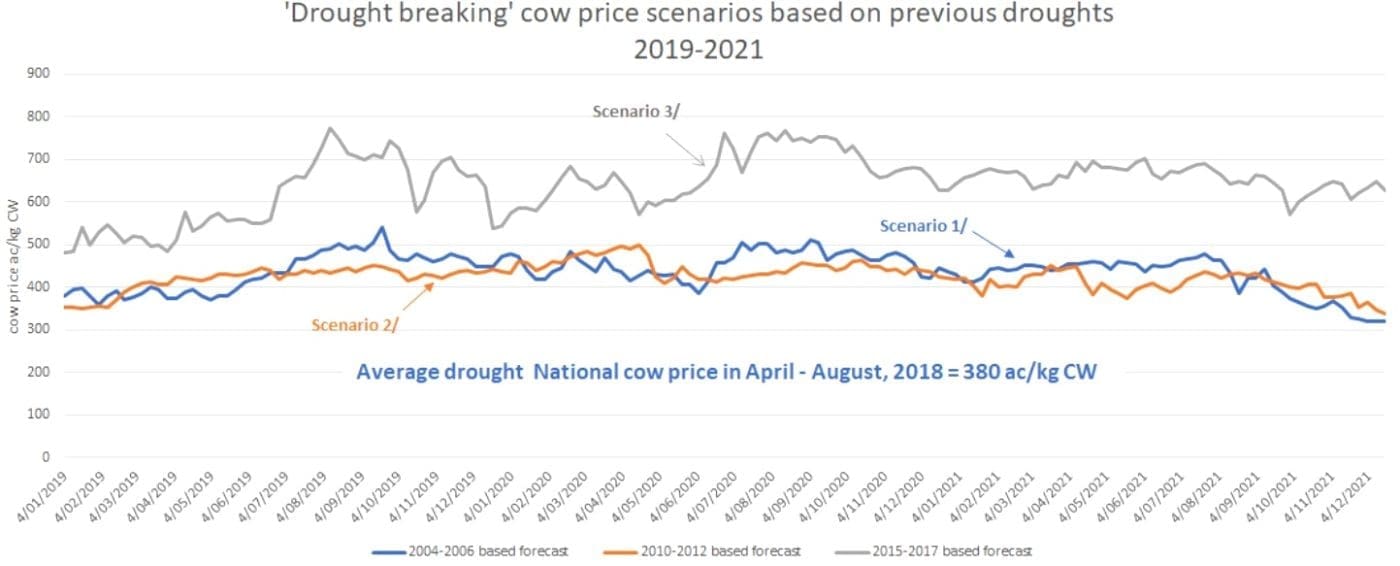

The next graph is the extrapolated potential prices of cows should the drought break, based on previous drought cow price movements. The starting price is this year’s drought affected April-August average national cow price (400-520kg) of 380c/kg – to create three ‘what if’ scenarios.

In brief, the 2002-03 drought and the 2006-09 drought had similar price movements that saw cow prices lift on average over the following three years by 50c/kg (or 430c/kg in today’s market) with a high of almost 120c/kg above the average which would translate to 500c/kg in today’s market.

I think the really sobering scenario is the forecast based on 2015-17 price movements which if were repeated would see an average price increase of 263c/kg over three years which would equate to 643c/kg for cows (compared to todays 380c/kg) with a potential high of 760c/kg which would be an unprecedented price. The last record peak price on cows was September 2016 when cows reach 540c/kg (just before the EYCI peak of 725c/kg).

It is hard to imagine that cow prices could double in value again when this drought breaks, yet as back in 2014, if anybody had said to a farmer back then that cow prices would double within a year, they, too, would not have believed them. It shows that anything is possible if demand is strong enough.

The table below summarises the potential highs and lows of what cow prices would have done at today’s money of 380c/kg CW, based on the previous post drought cow price movements.

Which scenario is likely to happen?

I think improved global beef prices are now built into today’s cattle markets, and this is evident when looking at the previous price cycles levels versus today’s market. So a traditional cow price rise in the 15-40pc range is more likely as opposed to the 70pc average cow price increase that occurred after 2013-14 drought.

There are several important caveats to this. Firstly, the severe drought of 2013-14 cleaned out a lot of old cows and today’s Australian cow herd is much younger as a result. Therefore the impact of liquidation is even greater this time, as quality cows will be very hard to find when the drought breaks. In the past the ability to buy ‘old cull cows’ and try to get another calf or two out of them was a potential cheap way to re-enter the breeding business, but with so few old cows left, this will be hard to do.

Should global beef prices go higher in the next 3-4 years, and when the drought breaks, it could see steer and cow prices go to new record levels in Australia. Given the potential shortage of protein due to African Swine Fever in China (see earlier report) I would not rule out this possibility and the continued growth of China and the Asian middle class are also key factors in driving global beef prices high.

Once again the ability to buy back cows with such strong slaughter market signals could drive cow prices much higher than expected. I think these two factors alone will add another 10pc to the price improvement range, putting my estimate on where cow prices could go to 25-50pc higher or from today’s cow price of 380c/kg to potentially 475-570c/kg CW if and when the drought breaks.

Question 2: Is the Australian drought going to see cheaper cow meat go to the US market?

Ten years ago I would have said yes to this question, but with the demand growth in China and other Asian countries for cow meat, the answer today I believe is no.

Although I have seen some short-term pressure in market prices that has seen imported US prices drift lower in recent weeks, this to me is a function more of the July-September (Q3) period and the weak demand globally that we see each year in Q3, as described above. Q3 global demand sluggishness happens every year, and this year is no different.

In the last few weeks, US market participants have spoken to me of the excess in pork, beef and chicken and the belief that imported beef will get cheaper as the Australian drought continues, which in the past saw US volumes increase and prices get cheaper as the US became ‘the market of last resort’.

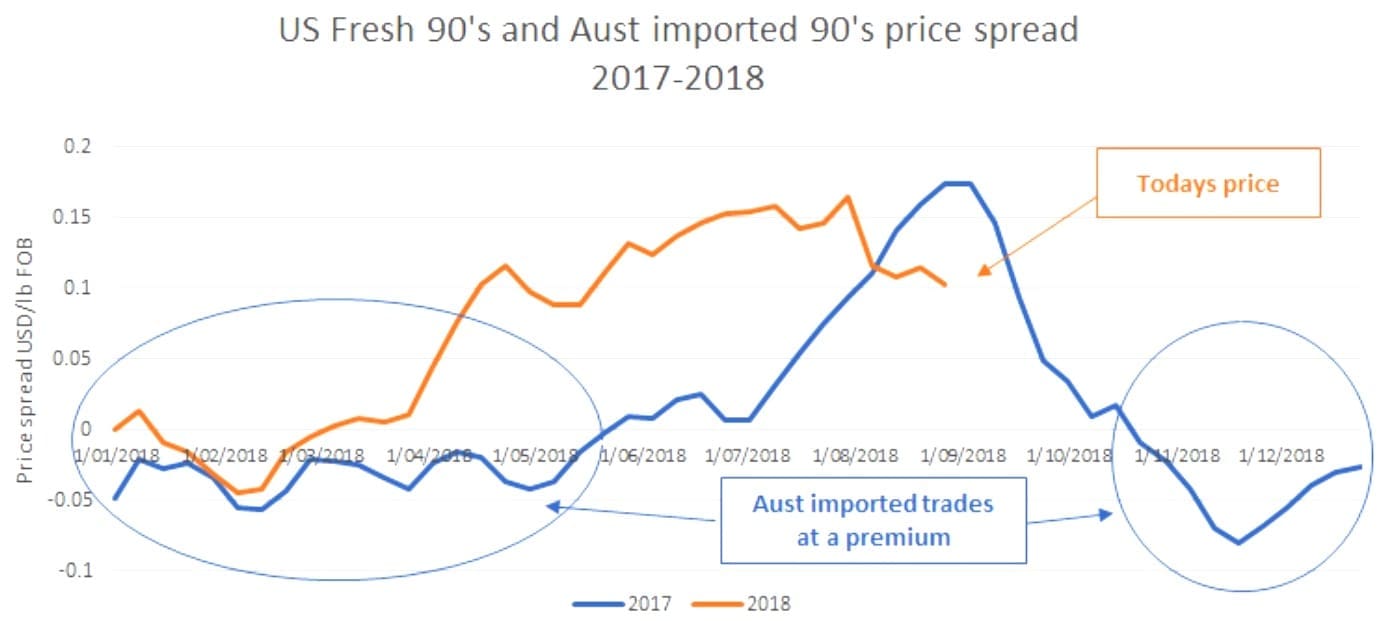

Last week one US market participant said to me that imported 90CL grinding beef was trading at a discount to US fresh 90’s, because of the Australian drought and this trend would continue into next year as the drought potentially worsens. I disagree with both these views.

The graph below highlights that Australia’s imported 90’s have been trading at a discount both pre-drought and during the drought. This normally occurs in May to October and this year came early in March but this is a seasonal factor. In the October to March period we see imported trade at a premium to domestic – this is a seasonal factor once again, and I see this year being no different in this price trend.

In short, the Australian drought is not driving Australia’s current imported 90 CL price discount but we are in a regular seasonal price movement that is likely to see Australian 90’s move to a premium to domestic 90’s within three months.

Drought is not driving cow meat exports to the US, but instead cow meat is going to other markets. In essence, a structural change has occurred in Australia’s export markets.

Us exports remain at 22pc of Australia’s global beef exports and have been at this ratio for many months. In previous droughts, this ratio was greater than 30pc due to the US being the destination of last resort due to the excess of lean meat and few markets would take the lean items.

But there has been a structural change in Australia’s export program with China and other key Asian countries now playing a crucial role in taking cow cuts that would have once been ‘slashed’ and put into the grinding meat pack and sold as lean trimmings.

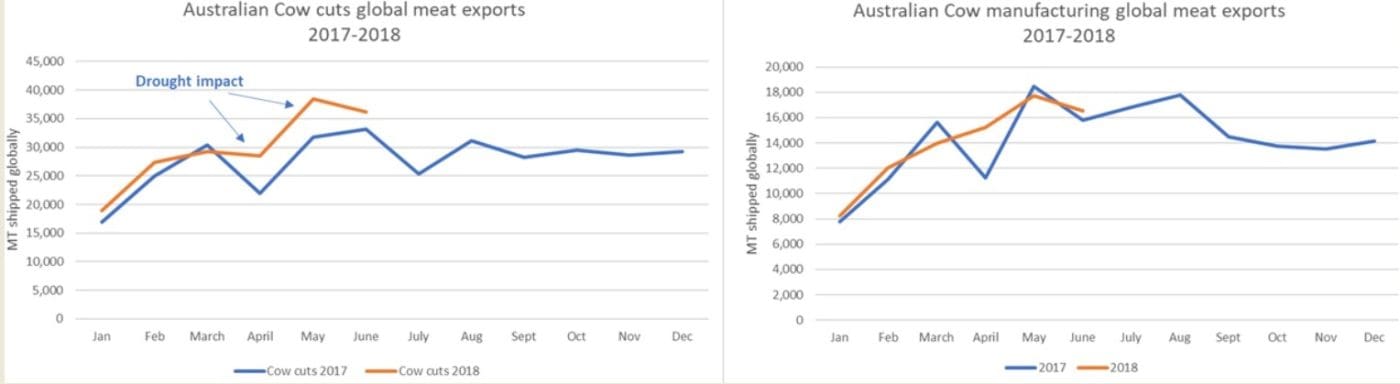

Australian global steer and cow meat exports since the drought commenced in April are 16pc higher in volume, with exports in cow cuts being 15pc higher and cow grinding meat 5pc higher. In other words, the additional drought-driven cow cuts are no longer being slashed and downgraded into the grinding meat pack but are remaining intact due to other markets paying a premium over the US for these items, in particular China.

Impact of drought so far on cow meat production and exports

The female kill in Australia has increased dramatically since April this year as the dry conditions have forced farmers to sell breeding stock in addition to their regular culling of older cows.

Where have the cow meat exports gone?

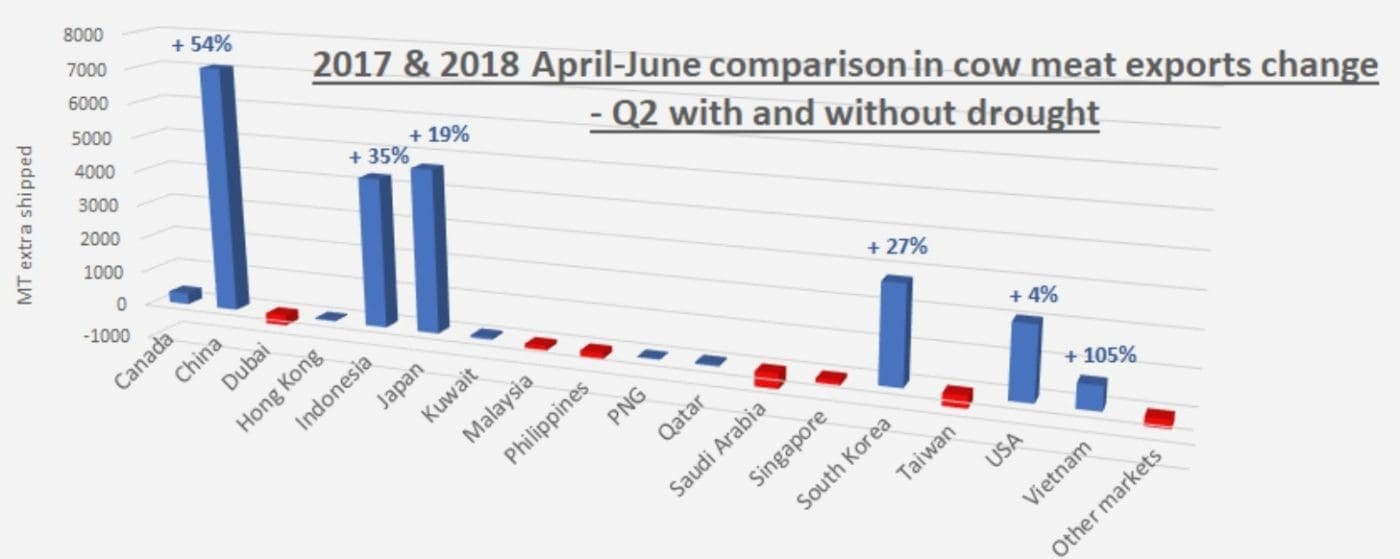

The following graph highlights who has taken the additional volume of cow meat produced this year in Q2 (April-June) compared to pre-drought conditions in Q2, 2017 last year. China, Japan, Indonesia and South Korea are the big winners taking the additional cow cuts. China has increased its volume by 54pc (or 7000t more), Indonesia by 34pc (4300t more) and South Korea by 27pc (2800t more).

Japan’s increase has been in cow trimmings, which has seen Japan buying away from the US the additional volume. The US increase in cow meat items has been only 4pc for Q2 compared to Q2 of 2017.

Effectively China, Indonesia, Japan and South Korea have been buying cow meat as either cuts or grinding meat away from the US, and this trend is unlikely to change as the drought continues – as a result there will not be cheaper cow meat into the US market. In the last two months overall market prices have fallen due to the lack of global demand which is typical of Q3 and the seasonal buying pattern that exists – improved demand is expected next month as China and other parts of Asia start to buy for Chinese New Year and the Asian Spring Festival.

Question 3: Have cow markets been impacted by the global trade war?

Since the Trump Administration imposed tariffs on China and other countries with a 25pc tariff on steel and 10pc on aluminium which took effect on March 23, counter tariffs have been placed on numerous US items by varying countries, including pork from the US to China which at the moment has duties of 78.2pc.

When asked what has been the effect on Australia’s exports so far, I believe the most accurate answer is the impact on currencies of competing supply countries and critical demand countries more than anything else. The pork duties and other meat product duties are likely to have a 6-12 month potential lag period but the impact of currency instability is immediate and is impacting our exports today.

In a recent report released in June by the World Bank Group, they summarised the situation accurately – saying “Emerging and Developing Economies (EMDE’s) remain vulnerable to risks of sudden market adjustments and tighter global financing conditions, which could be amplified by further US dollar appreciation, triggering disorderly exchange rate developments.”

The report said a worldwide escalation of tariffs up to the limits permitted under existing international trade rules could lead to cumulative trade losses equivalent to those experienced during the global financial crisis in 2008-09, with particularly severe consequences for EMDEs.

This report is both prophetic and insightful into what is driving the global currency movements today. I believe this currency impact is different on our cow meat markets compared to the high quality chilled and frozen steer meat markets.

Australia cow meat exports compete directly with EMDE countries like Brazil and India than compared to our major steer cut supply competitor, the US whose currency is stronger. So the impact of cheap currencies affects steer cuts much less than cow cuts.

There is overlap between cow and steer markets, but it is countries like China, Indonesia, Malaysia and Vietnam (also EMDE countries) which have cheapening currencies and accept beef from Brazil and India which have seen their currencies fall 18.5pc and 8.3pc respectively. To me, this points to Australian cow cuts being vulnerable on both the buy and sell side of the market much more so than Australia steer meat exports.

The key steer cut purchasing countries such as Japan, US and Korea are non EMDE countries and have relatively strong economies, and hence their currencies have remained stronger. This assists in buying Australian steer cuts.

The most dramatic currency impacted has been Brazil which has fallen 18.5pc since March 23 this year. The Indian Rupee has fallen 8.3pc, and in both instances each country competes into key cow meat export markets such as Indonesia, China, Hong Kong and Vietnam and in lesser cow markets such as Kuwait and Qatar – where the cheaper currency means they are far more competitive.

Thankfully neither Brazil nor India compete into US, Japan and South Korea for beef and this has seen both Australia’s steer meat exports and cow meat cuts be competitive against US meat due to the appreciation of the USD by 6.7pc.

Conclusion

Whether you are talking cows in the saleyard or export cow meat, both will become very expensive when this drought finally breaks, and it will be interesting to note who will be able to afford cows either on the hoof or in a frozen export box.

My bet is the buyer with the greatest need.