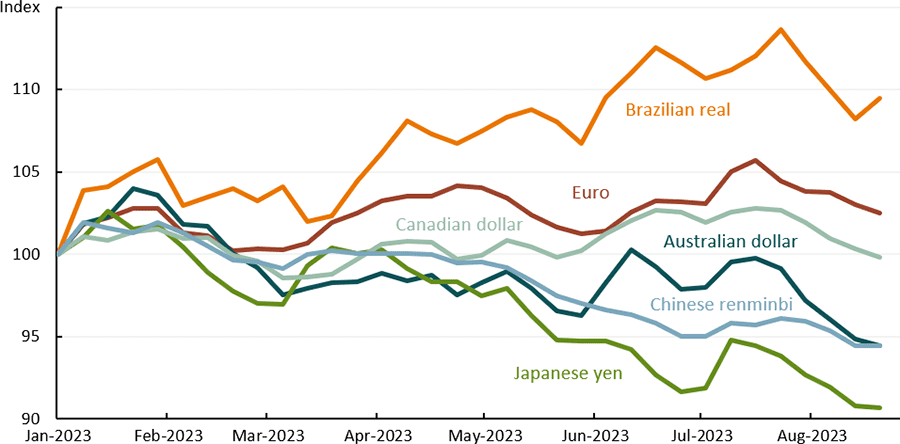

Relative weekly exchange rates against the US dollar, selected economies

- Market pricing suggests the US Federal Reserve will begin cutting interest rates before the Reserve Bank of Australia, improving the relative yield of Australian dollar denominated assets, such as government bonds. This typically increases demand for Australian dollars and leads to an appreciation against the US dollar.

- However, the Australian economy could soften more quickly than expected relative to the US economy over the coming months, leading to the RBA easing monetary policy earlier. This would likely lead to the Australian dollar depreciating further.

The Australian dollar has trended relatively lower against the US dollar compared to our major agricultural export competitors in 2023 (Figure 1.5). A comparatively lower Australian dollar over a sustained period increases the competitiveness in international markets of Australia’s agricultural exports contracted in Australian dollars. For most agricultural exports, which are contracted in US dollars, a weaker Australian dollar increases the Australian dollar value of these contracts.

The US dollar has also been broadly stronger than the currencies of major agricultural importers in 2023, such as China and Japan. This has raised the cost of agricultural imports for these countries relative to domestic products, which if sustained would likely reduce import demand.

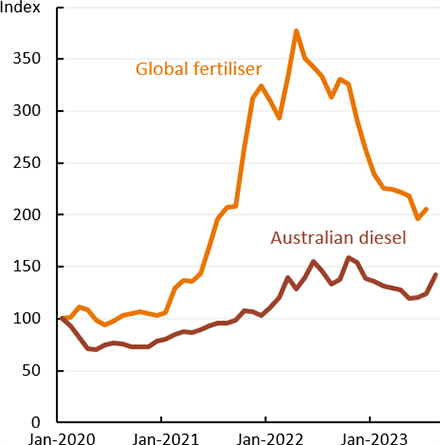

Meanwhile, high prices for fertiliser and diesel – which have increased farming costs for Australian businesses in recent years – have eased from peaks in 2022.

Monthly price indices, Australian dollars

Nonetheless, global fertiliser prices are expected to remain relatively elevated over 2023–24 due to strong demand and higher natural gas prices (a critical input to global fertiliser manufacturing).

Natural gas prices are likely to rise leading into the European winter. In addition, Australian fertiliser supplies have been constrained over the start of 2023–24 due to greater-than-expected demand in some regions. Australian diesel prices are closely tied to global oil demand and supply dynamics, such as the recent OPEC+ production cuts; but also a lower Australian dollar.

Given this, prices are expected to remain somewhat elevated over the remainder of 2023–24.

By contrast, container freight shipping prices have declined considerably over 2022–23 and are now back at pre-pandemic levels across the world. This has supported global supply chains returning to normal mobility and reduced freight costs along the agricultural supply chain.

Finance costs have increased significantly for businesses in Australia over 2023. Debt is an important source of funding for ongoing working capital and new investments for many Australian agricultural businesses. Higher interest rates have increased the level of income required to service debt, with interest payments increasing from an estimated 3% of farm expenditure in 2021–22 to 8% in 2022–23.

Labour costs for Australian businesses have continued to grow strongly over 2023.

Initially, wages increased to attract staff in a tight labour market. Now with the number of temporary migrants back working in agriculture at pre-pandemic levels, high labour costs in the industry are mostly being driven by unemployment near record lows, creating increased competition for skilled workers. In addition, recent increases to award and minimum wages for workers across the economy, partly in response to ongoing high inflation, has led to higher labour costs.

Australian regional unemployment rate, monthly

The Reserve Bank of Australia expects average wage growth to increase slightly over 2023–24 even as inflation subsides, potentially reducing business profit margins.

Source: ABARES