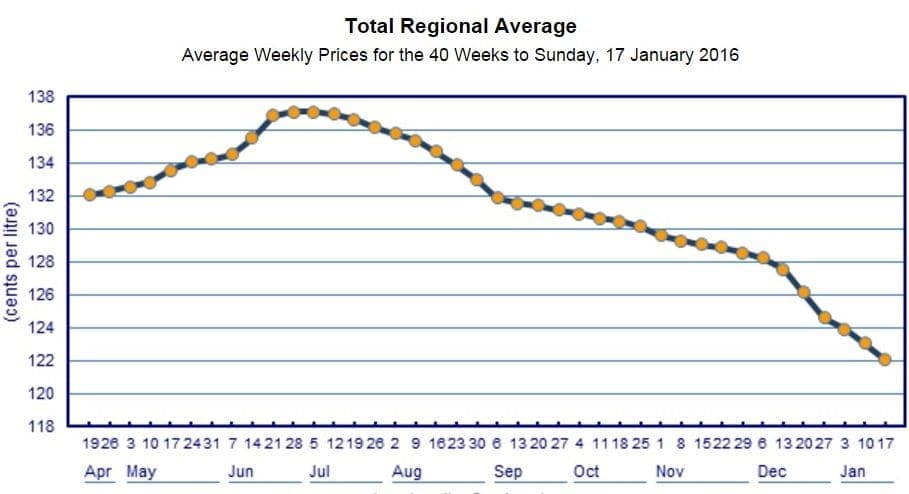

SPECTACULAR declines in global fuel prices over the past six weeks have pushed Beef Central’s regular monthly rural diesel fuel price report figure into uncharted territory.

As the graph above shows, diesel prices have continued to plummet, reaching a national average price in rural/regional areas of Australia this week of 122c/litre – its lowest level in the five years this report has been produced.

Pressured a growing global surplus of fuel oil, poor economic performance in China and elsewhere and a strong US$, diesel fuel prices have continued to plummet since November, and look likely to fall further.

The Australian Institute of Petroleum’s weekly price report for the week ended Sunday, January 17 indicates prices for diesel in non-metro regional areas of Australia averaged 122c/litre, another 6.2c/litre drop since our previous report in mid-December, and back more than 15c/l since late July.

The International Oil Market Report says a massive global oil stockpile at a record 3 billion barrels has forced prices lower. At the same time demand is easing, driven by recent difficulty in the Chinese economy and elsewhere, while there has also been by vigorous production growth from OPEC and non-OPEC supply. Russian oil output, for example, is at a post-Soviet record and likely to remain robust in 2016, while North American crude production is soaring.

By mid-January crude oil prices touched twelve-year lows, with Brent crude below $30/bbl. Exceptionally mild temperatures in the early part of the winter in Japan, Europe and the US, alongside weak economic sentiment in China, Brazil, Russia and other commodity-dependent economies, saw global oil demand growth flip from a five-year high to an four-year low.

“The net result is brimming crude oil stocks that offer an unprecedented buffer against geopolitical shocks or unexpected supply disruptions,” the report said.

The latest Australian Institute of Petroleum weekly survey shows that based on current average diesel prices for regional/rural areas of Australia, filling a Toyota Landcruiser 200 series (138 litres, main and auxiliary tanks) today would cost $168 – $31 less than the same fill this time last year.

All regions have seen big declines in diesel pump prices since mid-December, with the biggest drops seen in Queensland, WA and SA.

Regional/rural non-metro diesel prices in the latest AIP report for the week ended last Sunday included:

- Victoria 120.3c/litre (down 4c since mid-December)

- NSW 122.7c (down 4.6c)

- Queensland 119.5c (down 9c)

- WA 128c (down 6.9c)

- SA 118.5c (down 7.3c)

- TAS 129c (down 5.7c), and

- NT 137.8c (down 0.4c).

Monthly diesel report notes:

Australian Institute of Petroleum’s reported prices are calculated as a weighted average of retail diesel fuel for non-metro regions in each state/territory. All values include GST.

Australian Institute of Petroleum’s reported prices are calculated as a weighted average of retail diesel fuel for non-metro regions in each state/territory. All values include GST.

Variation in fuel prices can have a considerable impact of cost of production across the Australian beef industry, impacting on livestock transport, cost of shipping in live cattle and boxed beef exports, pumping stock water and providing station electricity in remote locations.

Crude oil, diesel and petrol prices are closely linked, as the price of crude oil accounts for the majority of the cost of producing a litre of petrol or diesel. Crude oil is purchased in US$, meaning that changes in the value of the A$ against the US have a direct impact on the relative price of crude oil in A$ terms.

NAB outlines impact of lower oil prices on Australia

The persistent oil glut globally has had mixed effects on various countries, NAB Agribusiness explained in this note to stakeholders:

The falls in global oil prices over the last year or so are fundamentally a reaction to oversupply in global markets – as US new oil supply comes on board, OPEC puts the squeeze on profitability of new sources of supply by refusing to cut production, while some traditional suppliers either add to production (e.g. Iran) or attempt to maximise production to add to their hard currency reserves (Russia).

Oil prices have taken another round of beating on China fears but is expected to be positive for global growth overall.

While recent drops to around US$30 per barrel may be related to fears of reduced demand – notably in China – it’s worth noting that the Chinese economy (unlike its equity markets) did not fall over in the first few weeks of January. China is very much in a process of transition from an economy driven by industrial production and construction activity to one driven by the tertiary sector (consumption and other services). Thus we are still comfortable with the view that China will grow by around 6 ¾% this year. Clearly their economy is not crashing although it might feel like it for Australian commodity producers.

Finally, on a global basis, lower oil prices in traditional economic models are net positive for global growth – albeit with very mixed effects by region. For example some of the best known global econometric models (IMF, IMF/WEO, and Oxford – while not perfect but do at least give some independent guidance) suggest that were oil prices to remain permanently around US$30 per barrel (rather than nearer US$50) global GDP might, after a year or two, be around 0.4% higher – with much larger positive impacts for economies highly exposed to commodity prices such as China (0.8%) and Japan (0.7%). Clearly the results are very negative in OPEC and Russia and mixed for Australia and the USA. Of course the results are very different if lower prices are demand driven. Finally one might fret that demand is about to crunch – it may – but as noted above, equity market concerns do not necessarily equal real economy outcomes.

The implications of lower oil prices on Australia are multifaceted, but the net impact is overall assessed to be neutral

On Australia the outcomes are complicated – but are probably net positive to growth and will result in lower inflation. The latter might also increase the risk of further help via rate cuts. But lower oil prices will be especially punishing on LNG profits – via the link between long term LNG contracts and oil prices. And, via that mechanism, it will provide further substantial headwinds to government revenues.