Simon Quilty

There is no doubt that if and when the drought breaks the impact on cattle and beef prices will be significant – but it’s the timing that matters, and where it breaks that will see different market impacts, suggests independent market analyst Simon Quilty, in his latest report…

THERE is no doubt there are some confusing market signals globally at the moment.

On the surface global beef prices look firm, with average prices higher than last year, but scratch beneath the surface and there are two separate stories to be told.

Firstly, falling grinding meat prices into the US, and secondly, strong global steer prices that have masked in some ways the impact of weaker grinding meat prices. In essence global steer cut prices is a demand-driven market, while grinding meat has now become a supply-driven market since February this year.

In March last year, I wrote that globally, we were at the start of a two-year ‘super-demand’ cycle that could see strong global demand and prices for all of 2017 and 2018. This, I believe, is still the case, but the ‘super-demand cycle’ is isolated to the quality end of the markets for both chilled and frozen steer items. It is the lower-grade manufacturing end of the market and cow items that continue to struggle, due to the drought in Australia and the US, and oversupply.

So what are the factors driving the two markets, and how long might each continue on their separate paths? And what danger is there for buyers in believing that low grinding meat prices are here to stay?

With rain (either in the US, or Australia, or both) the dynamics of supply are likely to change very quickly.

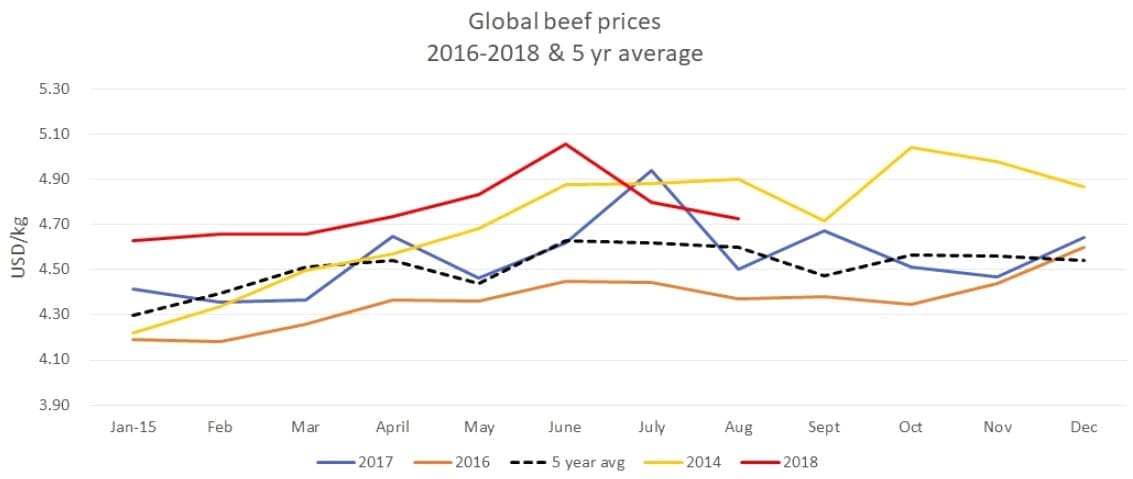

Global beef prices today

Today’s global beef prices are strong when looking at this year’s pricing versus last year, with pricing up 5pc, which has kept pace with global shipment volumes up 5pc. That indicates strong demand is continuing at the quality end of the market, as both supply and pricing is up. Asia has been a key driver in this strong price support, with Japan, Korea and China all playing key roles.

US beef exports in August were at record values and strong beef volumes, and continue to be an important indicator.

The peak in June saw global prices at US$5.05/kg which is the highest global price in the last 10 years and is traditionally the seasonal peak globally that coincides with the Northern Hemisphere summer strong demand period. This peak normally occurs in June or July, but in recent years as China’s demand influences global pricing, a second key price increase has occurred later in the year in December and early January, depending on the timing of Chinese New Year. Each year the volume of Chinese New Year beef buying has increased, due to China’s quickly expanding middle class.

Click on graphs for a larger view

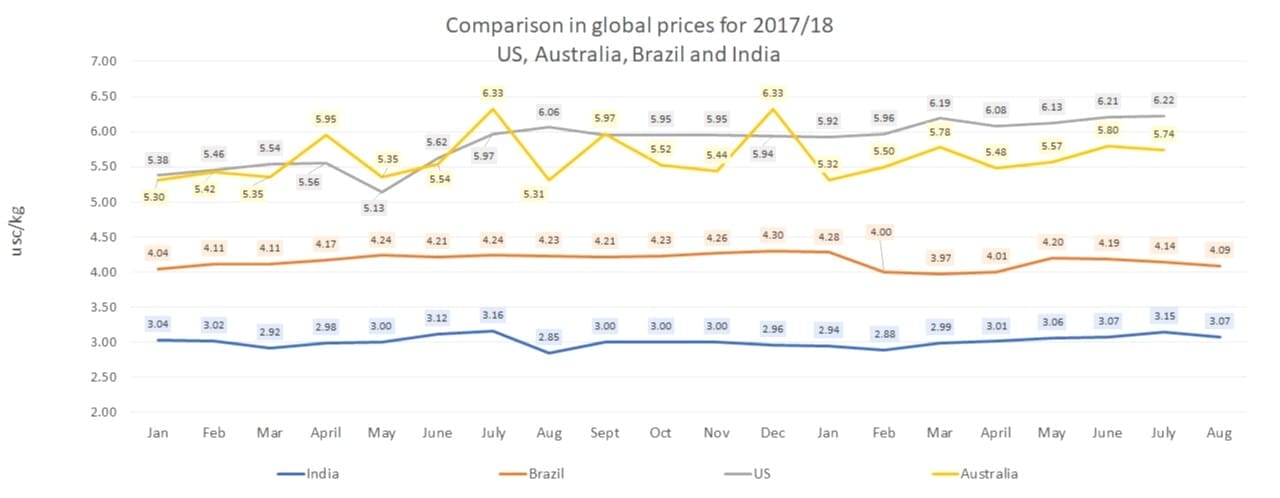

When assessing the individual pricing movements of each of the key export countries – Australia and US prices have improved steadily since April this year by 3.5pc, while Indian and Brazilian prices have either stagnated or fallen since May this year by 1.5pc – so each end of the market has moved further apart in 5 months by 5pc.

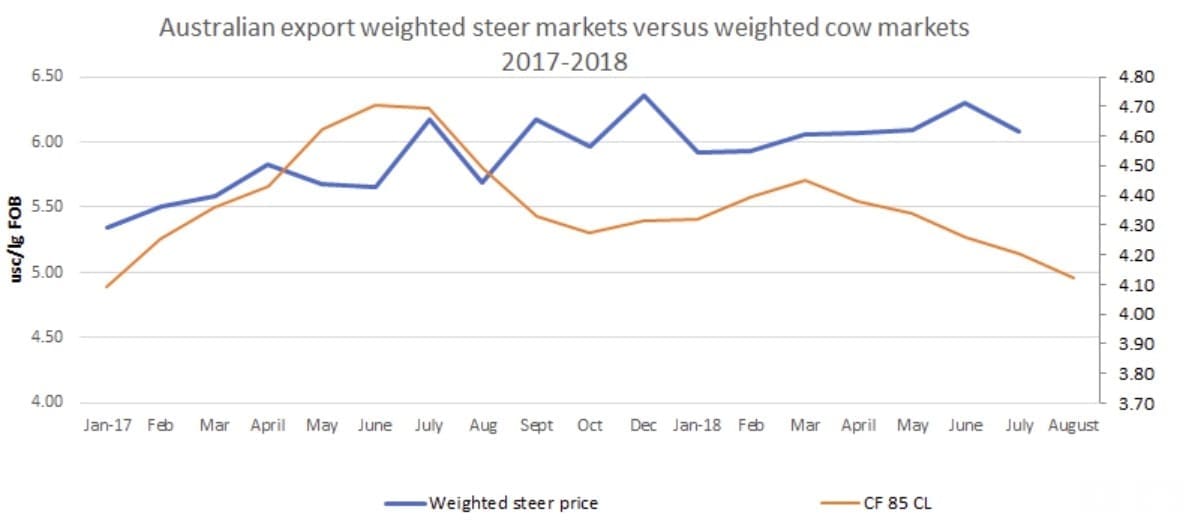

Strong global steer prices

Global steer prices have remained strong over the last 18 months. Outlined below are the weighted Korean and Japan export values against Australian 85 CL price into the US, to highlight that since March this year, steer prices have improved or held steady, but cow prices have fallen.

In August US beef exports set new records with beef export value topping $750 million for the first time, according to data from the USDA. August beef exports were at 119,850t, up 7pc from a year ago, with the value up 11pc on last year. Again, this all points to strong global demand.

Weak grinding meat markets

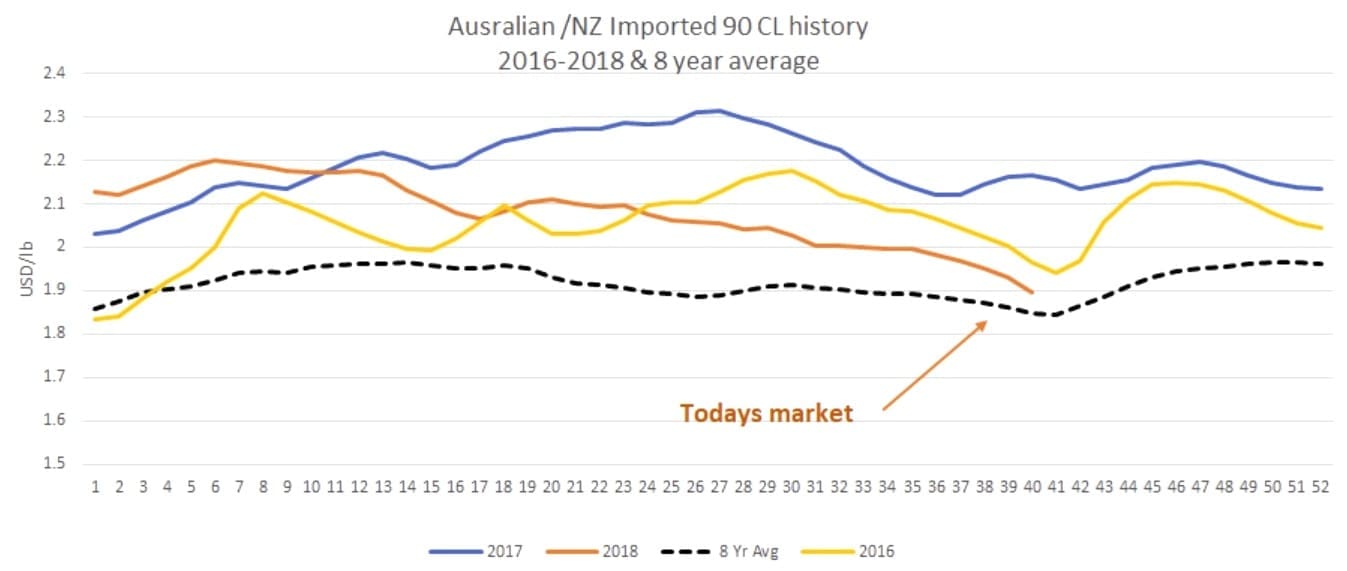

The US, to me, still sets grinding meat markets globally, and since April this year the volume of cow slaughterings in both Australia and the US has increased dramatically as both countries are in drought. But as pointed out in previous reports on Beef Central, US grinding meat volume has remained very similar to previous years, and Australian cow cuts have been diverted into Asia.

US grinding meat prices in 2018 have seen a steady decline, mainly driven by the drought in the US and the high slaughter of US cow. As a result Australian 90CL prices have fallen 13.5pc since February this year.

Drought in Australia and the US

The cause of this is the drought in both Australia and the US, with the impact of US drought being the bigger influence on falling grinding meat markets.

In October, US drought conditions have improved with the Drought Severity and Coverage Index, DSCI having registered 87 down from Septembers index of 115. US drought conditions still remain in certain areas, but the impact is now becoming more regionalised, with 41pc being declared as moderate to extreme drought conditions, down from earlier months’ level of 52pc drought declared.

The most vulnerable sector of the US cattle industry is the cow/calf operators, as they are so reliant on grass and under-performing cows, and will be the first to cull cows during dry conditions. Recent rain in Missouri in the last week has seen 6-8 inches fall, which has resulted in the drought conditions subsiding in the Mid-West. The regions that continue to remain in severe drought are the ‘Four Corners’, consisting of the southwestern corner of Colorado, southeastern corner of Utah, northeastern corner of Arizona and the northwestern corner of New Mexico. The other serious region is the West, where drought coverage and intensity remains unchanged, with hay crops being reduced to 50pc of the normal yields and remaining forage poor.

To further complicate matters, the recent US summer produced severe irrigation water deficiency due to the lack of major storms last winter, which bypassed the West and resulted in much less mountain snow this year which normally in summer provides a valuable irrigation reservoir. In many mountain regions the snowpack was reported to be only 30pc of the normal average snow storage levels, which left irrigation water during summer in short supply.

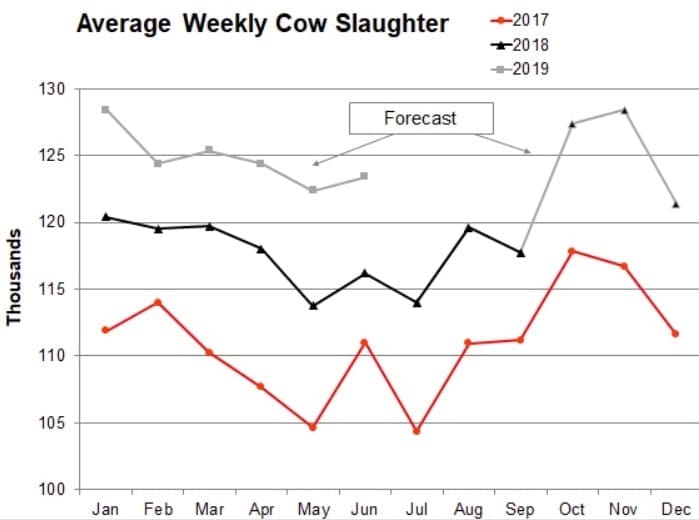

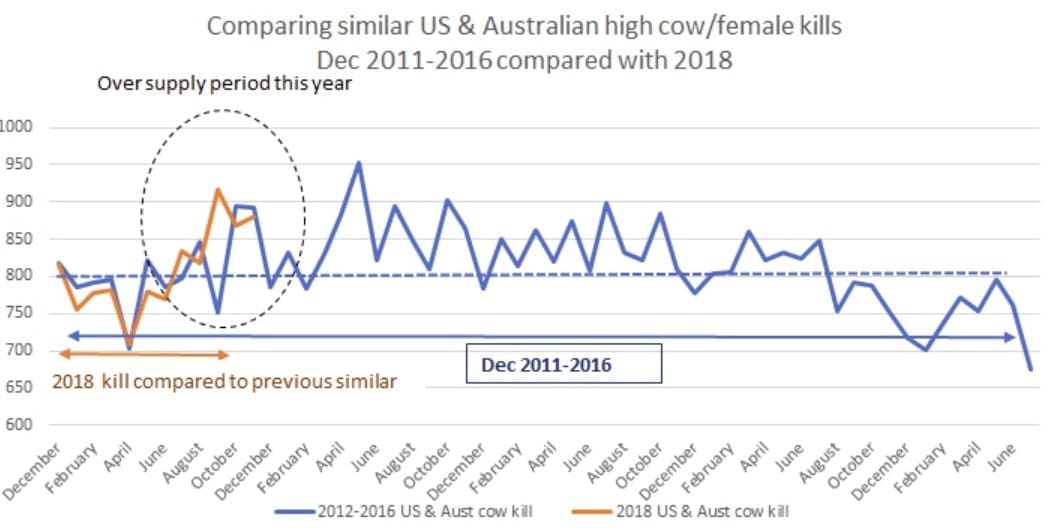

The net affect has seen this year’s US cow kill jump 8pc year-to-date compared to 2017.

The combined US and Australia cow/female is kill up 13pc, and this in turn has created an oversupply situation in cow meat, which as stated, has seen grinding meat prices fall since February this year.

Kevin Bost, a well-respected US livestock analyst has forecast the high US cow kill as being likely to continue at 6.8pc above the previous year’s cow kill until June next year.

US & Australian drought impact on grinding meat prices

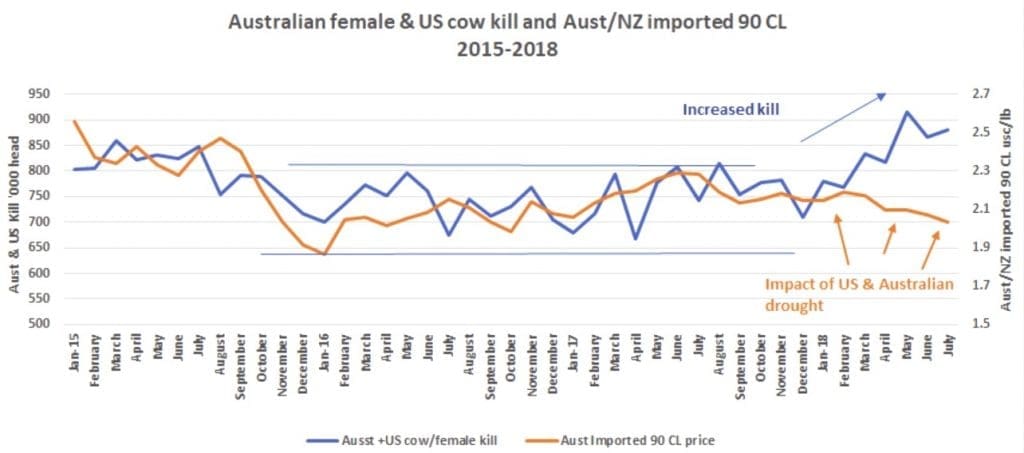

I used the above estimated US cow kill and added the Australian female kill to give a combined impact of drought on the impact of both on 90CL market.

The critical volume is 800,000 head across both Australia and US kills. It seems when volumes exceed this, the price of lean grinding meat falls – particularly when demand is lacklustre. To me, this reinforces the belief that this is a supply-driven market.

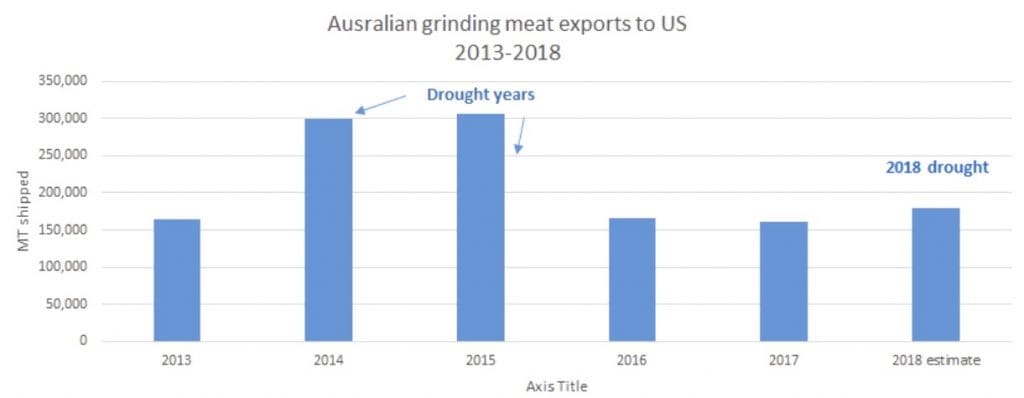

Total grinding meat exports to the US will be up slightly for the overall year, but compared to other drought years, the volume is likely to be down significantly. I am expecting the volume of grinding meat exported to the US to be close to 180,000t, which is slightly higher than last year’s shipments.

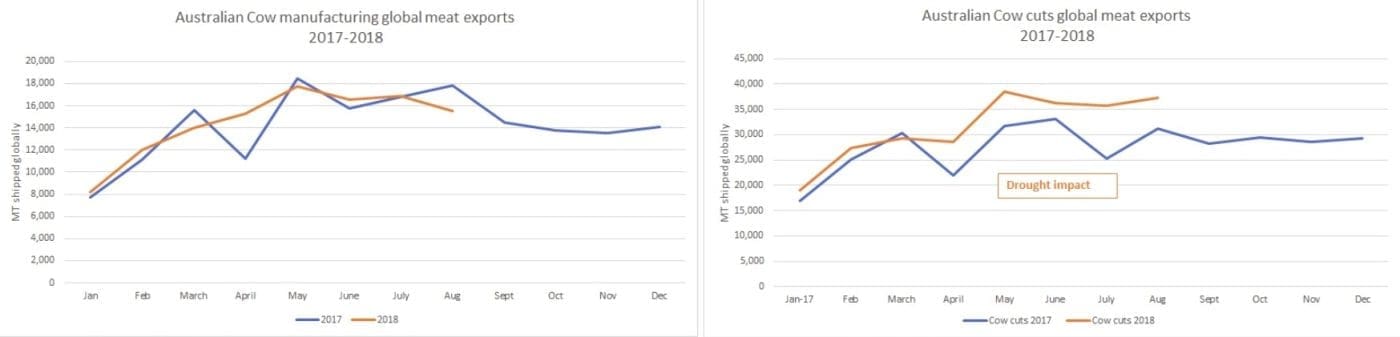

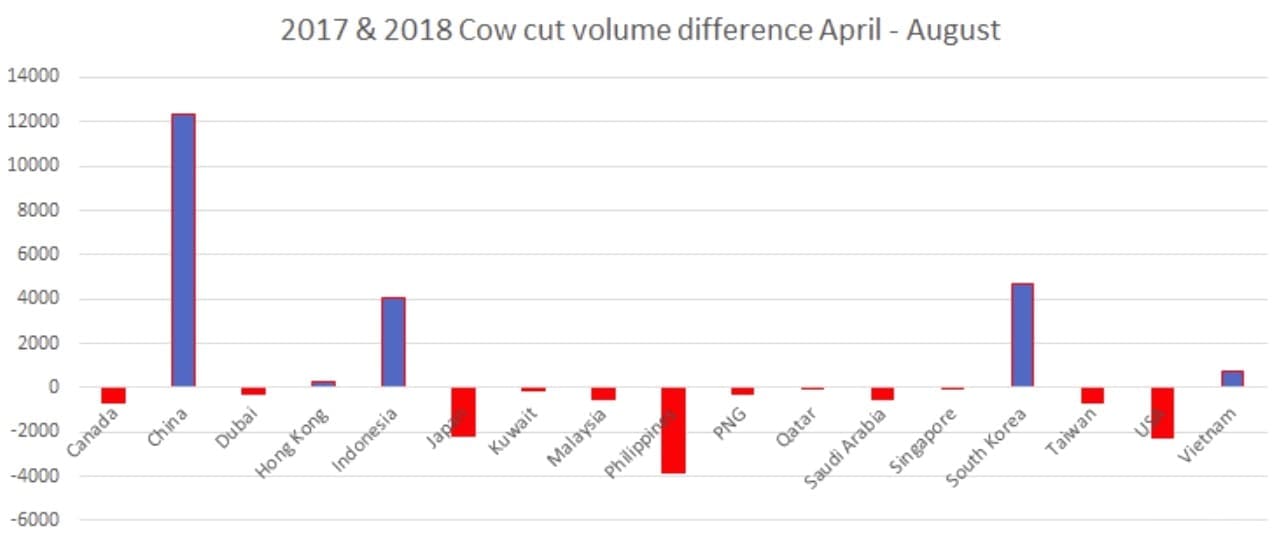

As can be seen in the graphs below, Australian cow manufacturing meat exports for 2018 are almost identical to 2017, with exports up only 1.3pc, whereas cow cut exports year-to-date are up almost 17pc with Asia playing a critical role in taking cuts instead of as traditional grinding meat.

The following are the key countries that have taken the extra cow meat cuts since the onset of Australian drought this year. China has taken 12,000t more than last year, with Indonesia and South Korea being the other key Asian countries taking extra cow meat cuts.

One scenario is the US drought and Australian drought continuing into 2019 with either one or both breaking mid to late next year.

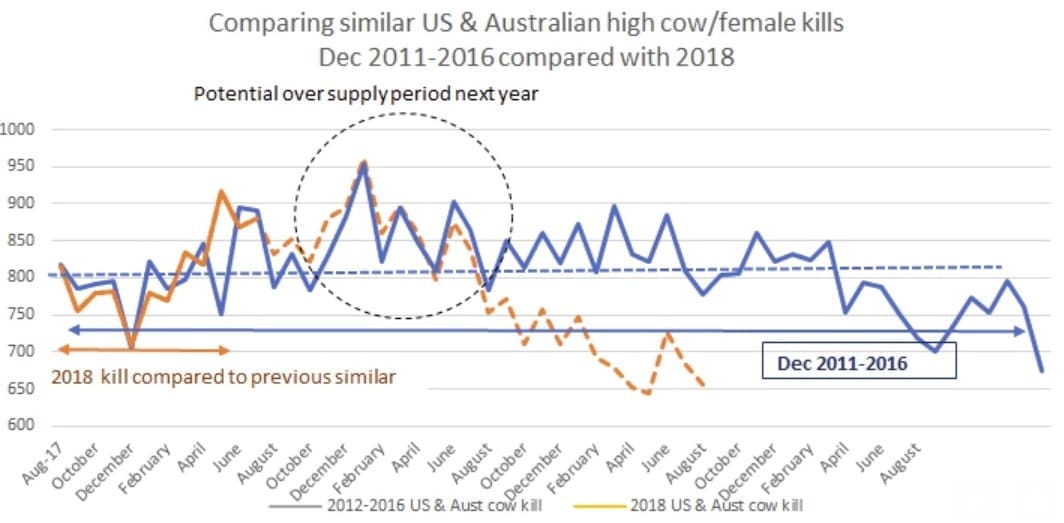

I looked back through history to see if I could find a similar kill volume and movement. There is one period during late 2011 and 2012 which has a similar look to today’s combined volume. (see below) When assessing potential difficult periods of over-supply, it would seem that next year’s 2019 February to July looks like it could be a period of heavy supply with total cow kills likely to exceed 800,000 head, if history repeats itself.

There are two other key factors to consider during this potential period of over-supply from February to July. Firstly, this coincides with the northern hemisphere summer demand period, which if strong, could see much of this excess supply absorbed. Secondly, this is also when New Zealand season is in full swing and could see the added pressure of supply influencing price and markets; and thirdly, the role of Asia and in particular China on taking excess volume.

In this scenario the impact of the drought breaking in either Australia and/or the US would see a ‘demand driven’ market return. I see the critical level for under-supply being 680,000 head – should the combined kill be lower, this is likely to result in a dramatic rise in grinding meat prices.

Australia’s drought breaking will impact both US and NZ prices

There are three important scenarios that could occur in the next 6-12 months:

- Australia’s drought breaks first, with good rains

- The US drought breaks first, or

- Both droughts break at much the same time (the fourth would be drought continues in both countries but recent rain in the US so the drought is becoming more isolated and regionalised and Australia’s drought on average last 2 years)

1) Australia’s drought breaks in the next 6-12 months before the US:

Should the drought break first in Australia, it is important to note the impact will not only see a tightening of supply into the US which will create a tighter US trim market, but of equal importance is the tightening into alternate markets that Australia currently serves on trim and cow cuts. The other non-US critical markets impacted would be China, Japan, South Korea, Indonesia and to a lesser extent Canada, Taiwan and the Philippines.

The lack of Australian cow meat in all these markets would create supply deficiency ‘holes’ which would need to be filled, with New Zealand the likely country to do so. This in turn would see NZ cow meat being diverted away from the US into these other cow markets. If I would put a value on the potential lift in prices due to Australia’s drought breaking, I would estimate close to US10-20c/lb lift across the lean trim market, above any seasonal price movements.

For the US market, the breaking of the drought in Australia would likely to see a double whammy effect, with not only Australian cow trimmings becoming tight, but also NZ cow meat also tightening as NZ supply fills the holes left by Australia. The net affect would see the US imported trim market tighten dramatically I believe.

2) US drought breaks in the next 6-12 months before Australia

This is potentially the more likely of the two scenarios, given the recent rain in the US and the impact on lifting US trim prices will be even more dramatic than should drought break in Australia.

This would see the critical cow kill numbers outlined above fall very quickly below the critical number of 680,000 cow/female kill combined from US/Australia. The impact on pricing of trim would be almost immediate, with potential rises of close to US15-30sc/lb over the following 3-5 months.

3) Australia/US drought breaks in the next 6-12 months

This is the most lethal combination of all that might see tightening throughout the US, and all key cow markets globally, with the potential price rise being even more dramatic than with each drought breaking on its own. Potential rises of US20-40c/lb would not be out of the question given the genuine strength of the US economy, and the strength of other global cow market economies such as Japan and Korea.

‘Shall ever the twain meet?’ Impact on Australia’s livestock market

The three scenarios outlined above almost work in reverse when it comes to the impact on cow livestock prices in Australia. The most significant impact will be when the drought breaks in Australia, and as stated in previous discussions in this series, could potentially see the value of cows increase 25-50pc as the market in Australia looks to rebuild.

With such a young herd already partially liquidated, there is no doubt in my mind cows will become extremely tight in supply.

The impact of the US drought breaking will be price supportive to Australian cow livestock values, but it will be a much more minor influence in the short term if drought continues in Australia at the same time. The impact may only be 5-10pc depending on how severe conditions are across Australia at the time.

The last scenario of both Australia and US droughts breaking at the same time, I believe, could drive the estimated 25-50pc higher price, adding an additional 10pc or more to the price rebound in Australia.

The potential of cows matching or exceeding the value of steers in Australia is a real possibility, particularly if both droughts break at the same time. I do not believe that cow cuts on their own will match steer cuts internationally, in particular the ‘sweet cuts’. In the past, cow round cuts have matched steer cuts, but rarely do they exceed them.

This scenario may be a potential outcome for a brief period. The exception to this rule might be 100 VL items which are very reliant on lean items such as INS, flats and eyes and should these items become hard to find, then the premium for 100 VL items could be high.

Columnist Simon Quilty is currently traveling in the US getting a first hand look at market conditions meeting with US processors, farmers, lotfeeders and end-users over three weeks, and attending US meat and livestock industry forums.