Image: Shutterstock

THE 2025 year is shaping up as one of those rare ‘goldilocks’ cycles in the beef industry when all parts of the supply chain – cattle producers, lotfeeders and processors/exporters – get a share of the profit margin pie.

Meat and livestock supply and demand, seasonal factors, processing capacity improvements and currency outlook all suggest this is possible.

The recent past has seen Australian beef margin share swing alarmingly from year-to-year, as herd size, weather conditions, and other factors came into play. Historically, both processors and producers have tended to make up for long periods of loss-making with financial ‘recharge’ periods, when margin is strongly in their favour.

The 2021-22 years saw cattle prices hit unprecedented record highs, as processors and lotfeeders scrambled to secure feeder and slaughter stock during herd rebuild. Flatback heavy feeders during much of 2022 traded in a range around 550c/kg for long periods, at one point pushing into the 600s, valuing a typical 450kg feeder steer at $2700. Processors racked up big losses during the period as a result, while many producers, blessed with good seasonal conditions, stacked up money like King Solomon.

But two years earlier during 2019, it was beef processors making a killing (both metaphorically and figuratively speaking – pun intended) with abundant, relatively cheap cattle due to herd liquidation, coupled with vigorous export customer demand, especially in ‘new frontiers’ like China.

Even last year, lotfeeders had a field day from mid-August through to early December, with feeder steer prices collapsing by 100c/kg to as low as 200c/kg, as producers panicked in the face of dry conditions and a depressing BOM summer seasonal outlook at the time. Young cattle took a similar path, with the EYCI falling 200c/kg (dressed weight equivalent) between late August and mid-October.

Notwithstanding some uncertainty surrounding next year’s demand and supply across some global protein markets, there’s cause to suspect that the Australian industry profit margin pie will be divided much more equitably over the next 12 months.

Here’s some reasons why:

Season:

Seasonally, the outlook for next year is now a lot better than it was even a month or two ago – especially in southern parts of the country, setting up the early part of 2025 with some confidence.

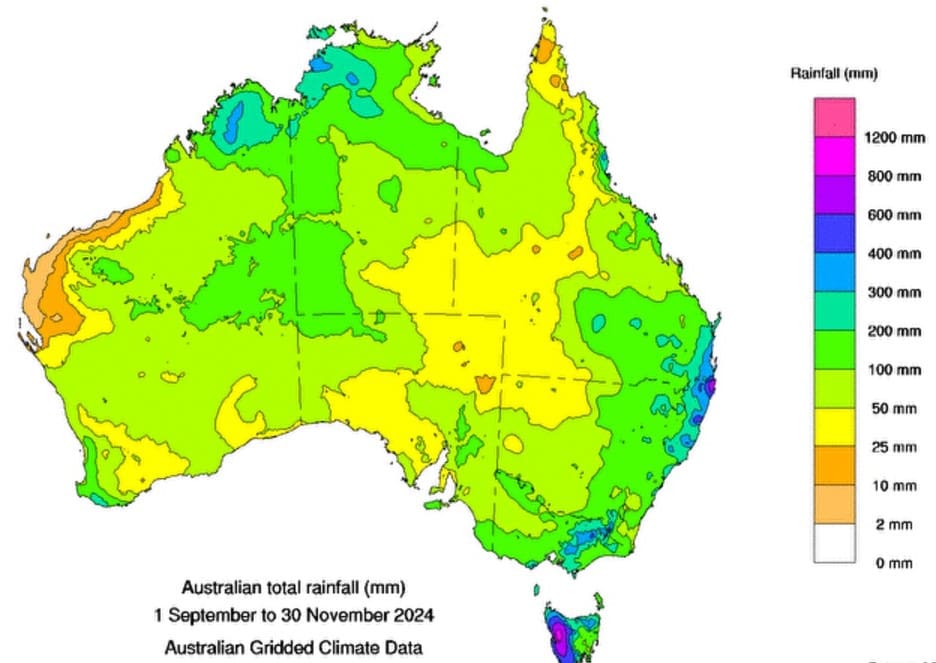

As shown on this BOM map of rainfall over the past three months to the end of November, large areas of eastern Australia have now had a good start to the summer season, with falls of 100-+200mm common across eastern parts of Queensland, NSW and Victoria over the past three months. December falls received over the past three weeks will only add to that. The Southern Oscillation Index currently sits at +7, close to its highest point all year.

Currency:

The Aussie dollar (measured against the US greenback) sat yesterday morning at US62c – its lowest point all year, and in fact since March 2020, when distortions created by COVID were buffeting currency. A low A$ adds to Australia’s beef export competitiveness in international markets.

Processing capacity:

Labour supply challenges saw beef processors tap-out at weekly kills (NLRS numbers) around 145,000 head during 2024 – but that only came in the latter stages of the year, as labour numbers gradually built. Supporting that, the fourth quarter of 2024 ending 31 December promises to be the largest quarterly national slaughter number since September, 2015.

Analyst Simon Quilty believes that next year, capacity to process cattle will grow a little further, to a figure possibly around 155,000 head – a seven percent rise on this year’s peak numbers – as new capacity comes on-line and additional workforce is added at other sites.

Barring widespread drought, that should help insulate against risk of cattle price distortion caused by numbers backing-up too much, waiting for a kill slot in under-manned plants. And with decent margins on offer in processing next year, processors will again be motivated to build on existing workforces.

Cattle price stability:

Australian young cattle and finished steer prices were remarkably stable during 2024, and are likely to continue so next year. Finished steer prices in 2024 traded within a relatively narrow band of 120¢/kg (carcase weight) since January, and have traded within a 70c/kg band from 550–620¢ since July.

The maturation of Australia’s herd rebuild into a consistent supply of slaughter-ready cattle, when paired with growing processor capacity and rising demand in export markets, has allowed prices to remain steady over the year, in marked contrast with extreme price volatility seen in 2023.

Young cattle are the same – the EYCI has been remarkably stable through 2024 – trading in a 150c/kg band from 541c/kg (dw equivalent) to 692c. Compare that with the 2023 year, when average weekly prices ranged from 785c to 349c – a spread of almost 440c.

Cattle supply:

MLA’s latest industry projections forecast has the national cattle herd at 29.57 million head next year, down 2pc on this year due to the mild destock that’s happened in parts of southern Australia due to dry conditions.

MLA forecasts slaughter numbers next year at 8.38 million, up 200,000 head or 2.4pc from this year. Offsetting that, carcase weights are forecast to decline 5kg to 305kg. Beef exports next year are forecast to lift another 17,000t to a record 1.904mt.

The national cattle herd has reached and passed a cyclical peak after operating at maturity for the past 12 months. Elevated turn-off will ensure a higher supply of finished beef, though turn-off of retained and utilised cows will stabilise the breeding herd, MLA says.

The northern herd is expected to stabilise into 2025 as average-to-good wet seasons will continue to support a large, productive breeding herd and increasing numbers of cattle exported into South-East Asia.

The southern zone has experienced some contraction in the back half of this year, as strong overseas beef demand supports higher turn-off in a now-mature herd.

Slaughter is expected to rise above ten-year averages, but remain well below the all-time peak previously set during drought turnoff in 2014.

If seasonal conditions remain largely average in southern Australia and average-to-good in northern Australia, MLA suggests that increases in turnoff will be driven by increasing availability of processor-ready cattle, as opposed to a climate-driven need to reduce stocking rates.

In particular, much of the breeding herd that was retained to power the rebuild is now mature and ready to be turned off.

“We expect that much of the rise in slaughter will be from this cohort, which will push the female slaughter rate above average. This dynamic has been evident across the first two quarters of 2024 and will continue,” MLA said.

Export customers: US production descending

Australian lean beef trimmings sold frozen into the United States hit a record high of 1024c/kg last week, as the impact of US herd liquidation starts to take full effect.

The fundamental driver is the big decline being seen in US non-fed slaughter, as a result of the impact of drought and herd decline.

Fed cattle (ie steers and heifers finished in feedlots) slaughter in the US this year has remained surprisingly high, despite the national beef herd declining to 50-year lows due to drought liquidation.

For the week ending 7 December, total US cattle slaughter was 614,000 head, representing just a 3.8pc year-on-year decline. Fed cattle slaughter was steady at 495,000 head, but crucially, cow/bull slaughter (closer aligned with manufacturing meat) dropped 17pc compared to last year, and 24pc compared to two years ago.

“US packers are struggling to secure sufficient cattle for production despite feedlot inventories matching year-ago levels,” analyst Len Steiner said a fortnight ago.

US packer margins continued to deteriorate due to high cattle prices. Tyson Foods’ recent decision to close a meat processing plant reflected broader concerns about tightening US cattle supply.

“Further reductions in US cattle processing capacity may be inevitable as packers adjust to projected supply trends over the next three years,” Mr Steiner said.

US production falling

In its 16 December Livestock Outlook report, USDA said US beef production next year is forecast to fall by 1370 million pounds or 5pc, on current year volume.

As a result, US beef imports are forecast to rise by 122 million pounds, or 3pc.

US cattle prices (Steers Five-State area direct) are forecast to rise even further to US$191/cwt, up 10pc on two years ago, USDA suggests, while feeder steers are forecast to increase another 8pc.

Because fewer feeder cattle are expected to be placed on feed heading into 2025, there are expected to be fewer slaughter steers available for processing starting in second-quarter 2025, and continuing for the next year or two.

Adding to the cattle dynamic is the recent discovery of New World Screwworm in cattle in Mexico and the subsequent US import ban on cattle from or transiting Mexico. The ban is assumed to remain in place until the policy changes, which is anticipated to limit available slaughter cattle starting in second-quarter 2025.

Export competitors: US

For the same reasons described above, the US is shaping up to be a much less vigorous beef export competitor for Australia in 2025.

US beef exports are forecast to fall by 365 million pounds or 12pc next year, affecting key markets like Japan, South Korea and China. Cost of production rises in the US as slaughter cattle become increasingly scarce will also challenge US competitiveness in markets where we both compete.

Export competitors: Brazil

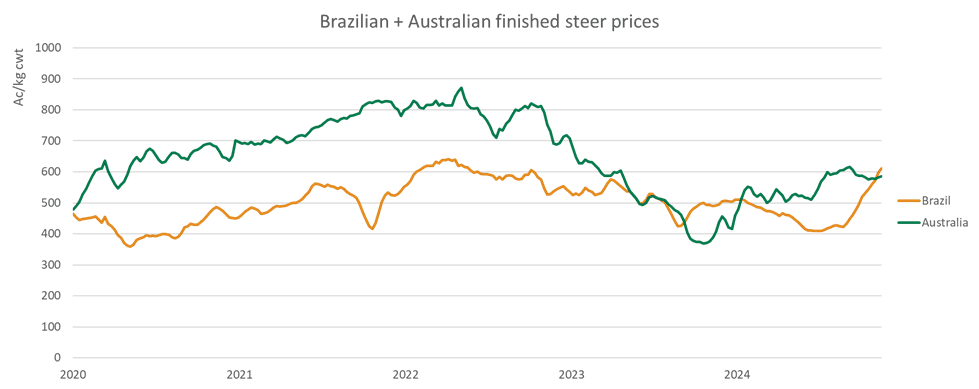

Brazilian processor steer prices have risen 52pc since June, meaning Australian cattle in early December were slightly cheaper than equivalent Brazilian cattle in A$ terms (see graph).

The sharp rise in Brazilian cattle prices can broadly be attributed to a slowdown in supply. After several years of drought conditions driving cattle slaughter up, supply of finished cattle has begun to tighten and Brazilian slaughter has begun to slow down. When combined with relatively consistent export demand, this has driven up demand for existing slaughter-ready cattle.

Provisional November monthly slaughter at 2.13 million head were 5pc below October 2024. While still very high, this is the first time slaughter has been below year-ago levels since 2021 and marks the fourth month of consistent declines in Brazilian slaughter.

The rise in Brazilian prices makes Brazilian beef somewhat less competitive in export markets, and acts as a signal of tightening supply. The markets where Brazil exports the most beef tend to be relatively price-sensitive (ie China), so increased costs are likely to correspond with lower exports over time, analysts suggest.

Signs of tighter supply and margins for processors in Brazil came in a recent report from Global Agritrends, which said Brazil’s JBS planned to shut down at least 11 of its South American processing plants in December and had suspended sales to China. There has been unofficial reports that there might be as much as 15 factories. Several smaller Brazilian meat packers were said to be following suit.

A surge in live cattle prices in Brazil was cited as the trigger for the shutdown. In recent months, Brazilian live cattle prices have risen by a 52pc, far exceeding industry expectations, Global Agritrends wrote. This caused the production costs of meat companies like JBS to increase significantly, and their profit margins were severely compressed. The companies eventually had to stop production to cope with the difficulties, the service said.

“With beef stock within China falling in the last six months, this fall in Brazilian exports is likely to see freezers in China emptied further and prices improve across beef, sheepmeat and chicken,” Global Agritrends wrote.

“With rising prices in China, further beef is likely to be diverted away from the US market, which is also price supportive for US imported grinding meat prices.”

Confidence

Market confidence has certainly shifted during 2024 from last year – many would say last year was the first time in a long time that producers made a decision based on a forecast rather than actual weather events. This confidence influenced buying behaviour; however, despite poor conditions in Victoria and SA, prices remained strong due to demand from NSW and Queensland producers.

All eyes have been on the global market, particularly the United States, which has recorded the lowest cattle herd in about 70 years. This has driven high cattle prices and thus increased the volume exported.

“Yes there may be emergence of improved confidence in Queensland in the latter half of 2024, but it’s a very long way in both economic and cattle cycle terms from where we were in 2022,” Stonex livestock and commodities manager Ripley Atkinson said in his most recent weekly bulletin.

“Confidence is king in today’s markets, for both cattle and sheep, and it will remain a key theme to watch closely in 2025 as to what kind of influence it has on the direction of the market,” he said.

Stability

Another part of the ‘confidence’ story heading into 2025 is stability.

Without a doubt, the cattle market has stabilised in 2024 – reflecting the balancing act between supply and demand which are influenced by weather, overall confidence and increased female slaughter, among many other factors.

Prices over the last 12 months have lifted by 20–40pc, indicating the recovery of the market from the challenging conditions in 2023.