Australia’s latest official beef industry outlook points to continued strong demand for young cattle in 2011-12 but a slight overall decline in prices due to subdued export conditions.

Australia’s latest official beef industry outlook points to continued strong demand for young cattle in 2011-12 but a slight overall decline in prices due to subdued export conditions.

The Australian Bureau of Agricultural and Resource Econoimics and Sciences (ABARES) September 2011 outlook for livestock released yesterday forecasts a 4pc fall in beef prices in 2011-12 to an average of 310c/kg dressed weight.

Continued restocker demand in most cattle-producing regions is expected to maintain upward pressure on young cattle prices.

However, prices for other categories of cattle are expected to average lower as a consequence of subdued demand from major beef export markets.

Cattle supply

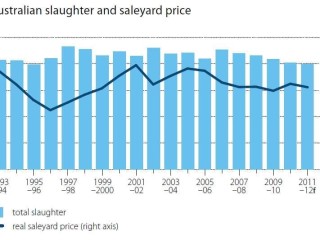

After increasing by 3pc in 2010-11 to 27.4m head, the national cattle herd is forecast to rise by a further by 2pc in 2011–12 to around 28.0 million head.

This is based largely on the improved pasture and water availability stemming from a good season over much of northern and eastern Australia in early 2011.

The combination of restocking, subdued export demand, lower prices and an ability to hold stock afforded by favourable pasture conditions will translate to slightly lower slaughter levels, which ABARES expects to decline by 1 pc in 2011–12 to around 8.0 million head.

Slaughter rates in the last financial year fell to 8.1 million head, their lowest level since 1995–96.

The composition of the slaughter is also changing as producers seek to increase herd sizes.

Australian female cattle slaughter was 15pc lower in the June quarter compared to the same period last year. Male cattle slaughter increased by 5pc over the same period, but not by enough to offset the decline in female cattle slaughter.

While Australia will slaughter less cattle, its production of beef and veal should hold firm, based on a 2pc rise in average slaughter rates due to the better seasonal conditions.

Exports to fall

Australian beef and veal exports are expected to decline by 2pc in 2011–12 to around 920 000 tonnes (shipped weight).

This reflects lower exports to Japan and historically low exports to the United States.

The high Australian exchange rate and increased competition from US beef in the north Asian markets are expected to lead to weaker demand for Australian beef in export markets.

In a sign of the growing importance of smaller, diversified markets to Australia’s beef export trade, the total share of exports to the three big markets of Japan, the US and Korea is expected to be close to 68 pc in 2011–12, compared with the high of 92pc in 2004–05.

US

Beef exports to the United States are forecast to remain largely unchanged in 2011–12 at 160 000 tonnes (shipped weight). However, the volumes of exports to the United States are expected to fall in the near term before increasing later in the financial year. Consumer demand is expected to remain weak in the United States and the Australian exchange rate is assumed to remain high, reducing the price competiveness of Australian beef.

Additionally, US beef production is expected to remain high in the first half of 2011–12. However, growth in US beef production could slow in the second half of 2011–12, under the assumption of more favourable seasonal conditions. The fall in domestic production is expected to lead to increased demand for imported beef, including Australian beef.

During 2010–11 exports of Australian beef to the United States fell by 24 pc to 160 000 tonnes, the lowest since 1965–66. This fall resulted from weaker consumer demand, a higher Australian dollar and prolonged drought in key US cattle-producing regions. The unfavourable seasonal conditions resulted in increased US domestic production, which reduced the demand for imports.

Japan

Australian beef exports to Japan are forecast to fall by 7 pc in 2011–12 to 325 000 tonnes (shipped weight). This forecast fall is largely the result of subdued demand in Japan, increased competition in that market from US beef and the Australian dollar remaining high.The Japanese economy is expected to exhibit only slow growth over the coming year and average personal incomes are expected to remain relatively flat. This is expected to lead to Japanese demand for beef remaining static.

Australian beef is continuing to lose market share to US beef in the Japanese market as US exporters slowly but steadily regain market share lost in the early 2000s. In the five years prior to 2003–04, Japan imported on average around 300 000 tonnes of beef a year from each of Australia and the United States. The United States was one of Japan’s two largest suppliers of imported beef, partly due to consumer preferences for higher marbling—a feature of US beef where cattle are predominantly finished in feedlots.

Additionally, the US beef industry is well placed to supply specific cuts that the Japanese prefer. The bovine spongiform encephalopathy (BSE) related ban on importing US beef in 2003–04 led to Japanese imports of Australian beef rising to 416 000 tonnes. However, demand for Australian beef has fallen in recent years as health concerns about US beef have eased and trade restrictions relaxed.

Japanese imports of US beef in 2010–11 were still less than half that of 2002–03, but have grown steadily and are expected to continue growing in 2011–12. The drive by the United States to regain market share is expected to be aided by a weak US currency.

The damage to the Fukushima nuclear power plant as a result of the earthquakes and tsunami in March 2011 has also adversely affected the beef industry in Japan. In mid July, cattle shipments from four prefectures—Fukushima, Miyagi, Iwate and Tochigi—were banned, as many cattle were identified as having eaten contaminated rice straw.

The four prefectures account for 14 pc of the Japanese cattle herd. In late August 2011 the ban on shipments was lifted, however all beef from farms known to have possessed contaminated rice straw will be subject to scientific testing. Remaining farms in the four prefectures will need to submit samples in every shipment for testing before it can be sold.

Korea

Australian beef exports to the Republic of Korea are forecast to increase by 4 pc in 2011–12 to 145 000 tonnes (shipped weight). Korean demand for imported beef is expected to remain strong over the coming year due to continued substitution of imported beef for local product due to ongoing concerns around foot and mouth disease.

However, the low US dollar against the Australian dollar and a gradual acceptance of US beef in the Korean market could lead to increased competition from US beef.

Australian beef exports to the Republic of Korea increased by 12 pc in 2010–11 to 139 000 tonnes. This can be partially attributed to the outbreak of foot and mouth disease in late 2010 in the Republic of Korea, which resulted in removal from the supply chain of some of the domestic herd and replacement by US and Australian beef imports.

Other markets

With demand for Australian beef forecast to be generally subdued in the major markets of Japan, the United States and the Republic of Korea, beef exports to other markets are forecast to grow by 1 pc in 2011–12 to 290 000 tonnes (shipped weight). This follows a 34 pc increase in 2010–11 to 287 000 tonnes. The largest increase was to the

Russian Federation (up 200 pc to 71 000 tonnes), which was assisted by reduced volumes of beef imports from Latin America.

Live exports

In early June 2011, the Australian Government suspended live cattle exports to Indonesia for the purpose of slaughter. On 6 July, the Minister for Agriculture, Fisheries and Forestry signed the Export Control Repeal Order 2011 to lift the suspension of trade in live exports to Indonesia provided that supply chain assurance principles are in place to achieve internationally agreed animal welfare outcomes.

Total live cattle exports in 2011–12 are forecast to fall to around 450 000 head. However, there is considerable uncertainty as to how quickly live exports to Indonesia will increase over the remainder of 2011–12.

In 2010–11, exports of live cattle for slaughter from Australia fell by 16 pc to 728 000 head.

The largest decline was in cattle to Indonesia, which fell by 35 pc to 456 000 head. This decline mainly resulted from Indonesia enforcing a 350 kilogram live weight limit and issuing fewer import permits. The proportion of cattle shipped to markets other than Indonesia increased from 7 pc to 37 pc of total volume in 2010–11, the highest in five years.

This was driven mainly by a rise of 100 000 head of cattle exported to Turkey.

Indonesian live exports

On 6 July 2011, 29 days after imposition of the suspension on live cattle exports to Indonesia, the Minister for Agriculture, Fisheries and Forestry, Senator the Hon. Joe Ludwig signed the Export Control Repeal Order 2011, lifting the suspension provided that supply chain assurance principles were in place to achieve internationally agreed animal welfare outcomes. The first shipment of live cattle bound for Indonesia left Australia on 10 August 2011.

Effect of suspension

To assist an assessment of the effects of the suspension of trade, ABARES conducted a survey of farm businesses in northern Australia in late June and early July 2011 (prior to the suspension being lifted). The survey revealed that around 660 (of the 1459 with more than 100 head of cattle) farm businesses in northern Australia intended selling cattle for export to Indonesia in 2011. Of these, around 300 intended exporting more than 50 pc of their total cattle turn-off to Indonesia.

At the time of the survey, around 278 000 head were still available to be exported to Indonesia over the reminder of 2011. Farm businesses in northern Australia intended to export 597 000 head of cattle to Indonesia in 2011, of which 375 000 remained unsold at the time of the survey. Of the 375 000 unsold, 274 000 were ready to be shipped to Indonesia.

The suspension of live exports to Indonesia placed financial stress on many farm businesses in northern Australia. In response to reduced revenue, around 46 pc of farm businesses intended to temporarily lower costs by reducing non-essential spending on capital and repairs, adjusting herd management, delaying loan repayments, and reducing staff numbers. Of the farms intending to export cattle to Indonesia, 68 pc were not actively seeking alternative markets, either foreign or domestic. Around 5 pc of farm businesses indicated that if the suspension lasted more than a few months, they would cease operations.

- To view ABARES September 2011 Commodities Outlook report in full click here