TRADITIONALLY, a cattle producer has been happy for their calving ratio to fall in favour of steers, due to the widely accepted rule that steer calves are worth more than their heifer siblings.

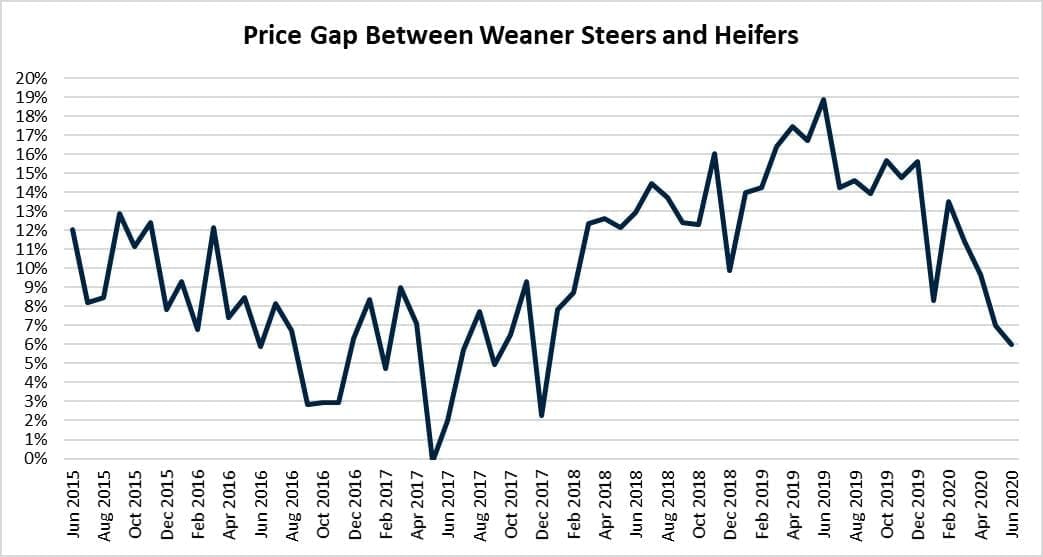

The price differential between steers and unjoined heifers is a useful indication of the current state of the cattle market. The difference, as measured between June 2015 and June 2020 on AuctionsPlus listings, has on average over the past five years sat at ten percent. However at times the price gap has exceeded or been less than this average, as certain market conditions promote considerable price swings.

There are certain market factors and conditions that result in the gap between heifers and steers reducing. The most common is the period of rebuilding the national herd which typically follows a significant or drought-breaking rain event.

Supply is currently at an all-time low, but demand is extremely high for all stock categories as producers look to take advantage of feed and rebuild their operations. We are currently seeing these market conditions play out, with the average price difference being 9pc for the first half of the year, with June currently tracking at 6pc.

Following a request from Beef Central, the AuctionsPlus Market Insights team has investigated data from 2015 to present to showcase previous periods when the price disparity between the genders has reduced. AuctionsPlus monthly cattle listings have been used to illustrate the effect of supply on prices and the price gap.

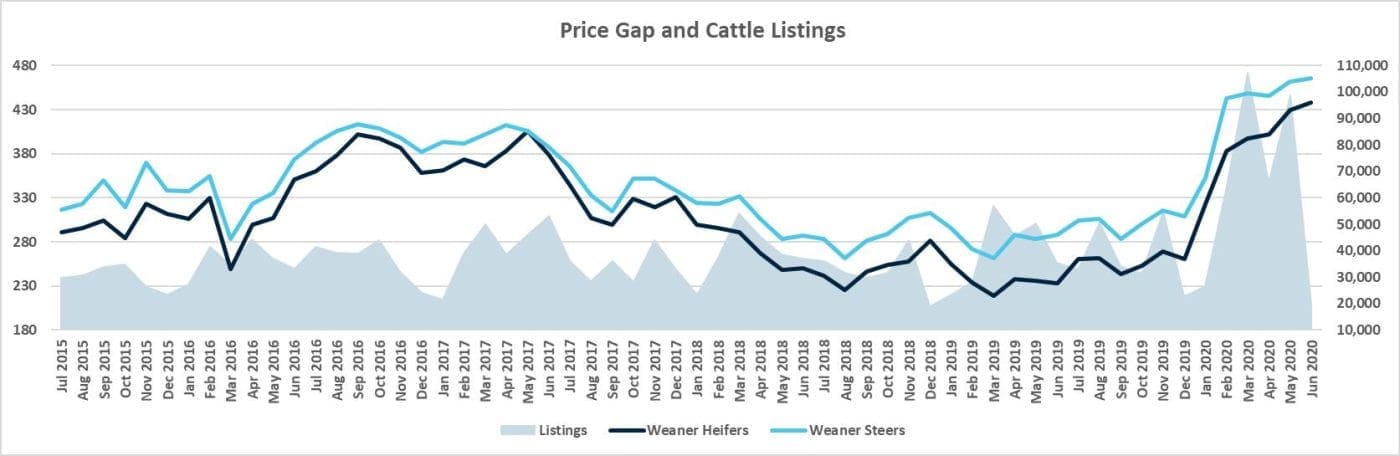

Figure 1: Price gap between steers and heifers with total monthly cattle listings. Click on image for a larger view

Generally speaking, steers trade at a considerable premium over heifers. This is due primarily to feedlots being willing to pay more for feeder weight steers, as they have the capacity to reach slaughter weights faster than heifers. Steers require less feed and time to reach slaughter weights and will ultimately increase feedlot profitability allowing for the overall efficiency of the program to increase. As it costs more to feed heifers, the initial outlay price is typically significantly less.

Processors will also typically pay a little more for fed steers over equivalent liveweight heifers, due to variance in meat yield.

The last period when heifers and steers were similar in price was during 2016 and 2017. The price gap averaged 6pc for this period, and in May 2017 the gap reached zero. This was a herd rebuilding phase after a period of prolonged drought.

Strong rainfall in the Autumn of 2016 resulted in a surge of AuctionsPlus listings as demand to rebuild was strong. Prices for steers and heifers became similar, as producers looked to pay premiums for potential breeding cattle. The period from 2018 through to late last year saw the gap widen again, averaging 14pc as listings fell, prices eased, and the drought sustained.

Figure 2: Price Gap between Steers and Heifers from June 2015 to June 2020. Click on image for a larger view.

Currently, we are observing similar conditions to 2016/17, with the key difference being the larger listings experienced at present. The start of 2020 has seen widespread consistent rain across eastern Australia, stimulating the market to surge. AuctionsPlus listings have increased by more than 100pc and prices have skyrocketed as producers look to fill empty paddocks.

Price gap narrows

The price gap between steers and heifers during the start of 2020 has again reduced, as the value of all beef articles have risen. As shown in figure 2, February and March exceeded the 10pc average, but this can be explained in the enormous numbers of cattle listed on the platform. In March alone, 107,311 head of cattle were listed, setting a new AuctionsPlus monthly listings record. Much of the listings were breeders. as sellers looked to take advantage of a rapidly rising market, the over-supply of breeders caused the price disparity to ease.

Looking forward, it’s anticipated that we will continue to observe a reduction in the price gap as the herd rebuild and producer restocking continues.

As the uncertainty of COVID-19 begins to dissipate and more importantly a large portion of the Eastern States continues to receive rain, the question remains as to how small will the price gap be? Will it head back to zero like in 2017, or could it even fall into the negatives where heifers trade at a premium over steers?