Among larger lines offered this week was two runs of Santa-based backgrounder heifers totalling 228 head off Marathon Station, east of Richmond, North Queensland. Both groups averaged 212kg at 6-12 months. The first run of 114 made 584.4c/kg, with the second making 579.6c.

A 13 percent contraction in numbers on AuctionsPlus this week saw price trends varied, with average prices for weaner steers and heifers both falling, while yearling and grown steers rose in value.

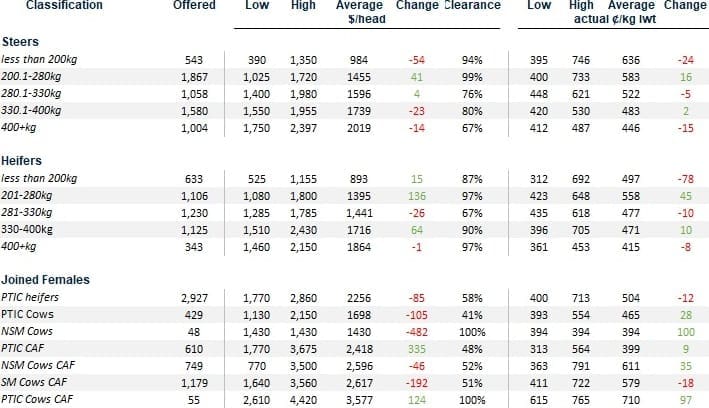

Among breeding cattle, PTIC heifers fell $60 a head on average, with a clearance rate of 58pc, while cows with calves at foot were back $86. Going against that trend was PTIC cows, up $107/head on average.

From the 15,876 head offered this week, PTIC heifers continued to be the largest category line, followed by 200-280kg steers.

One of the most notable factors in the market this week was a decline in the number of joined cows, heifers and cows & calves offered.

However, lines that meet buyers’ specifications continued to clear the market quickly and at what could only be described as ‘seller-friendly’ prices. Among them, 70 PTIC heifers out of the Northern Tablelands of NSW, sold to $2810/head this week, or an estimated 1411c/kg liveweight. The 17–19-month-old Angus heifers averaging 394kg were PTIC to Wagyu bulls.

A line of 55 cows and 54 calves at foot sold for $2190/unit this week, sourced out of Cooladdi, west of Charleville, Queensland. The 55 Santa/Shorthorn x Hereford cows averaged 357kg.

Average prices for the two heaviest young steer categories eased $23 and $14 this week, averaging $1739 and $2019, respectively. The demand for all lines and weight ranges remains exceptionally robust, with many regions (apart from some parts of Queensland) now assured of an autumn that will likely register good growth prior to the cooler months setting in.

Among young cattle traded this week, 53 Angus weaner steers 8–9 months averaging 343kg from Willow Tree, NSW, sold for $1780. Additionally, a line of 70 Angus heavy feeder steers 18-19 months averaging 517kg out of Barnawartha, Victoria, sold for $2396.

Among larger lines offered this week was two runs of Santa-based backgrounder heifers totalling 228 head off Marathon Station, east of Richmond, North Queensland. Both groups averaged 212kg at 6-12 months. The first run of 114 made 584.4c/kg, with the second making 579.6c.

Assessor Ashley Naclerio from Stockplace Marketing said the heifers were in a light store condition, and had plenty of compensatory gain in them with ample bone and frame throughout the mob. “These heifers have a fantastic reputation as heavy feeder/slaughter heifers and are being sold much earlier than usual due to a shortened growing season, to keep grass for mature breeders.” he said.

Forecasts for some good falls in the coming week through southern Queensland will be interesting to watch, especially if some of the drier regions finally get some much-needed rain. In the south, producers will start to turn their attention to feed supplies for the winter months.

Prices reported below are as at the close of reporting of 2pm, Friday 5 March.

The state of the cattle market in early March 2021

Tim McRae

For AuctionsPlus reported categories, February 2021 averages ranged from 15-37% higher compared to February 2020, while for proven and assessed breeders, the increases climbed as high as 63% and 54%, for cows with CAF and PTIC heifers, respectively. Indeed, almost by definition, record high cattle prices in 2021 would be “unprecedented”, given that they have never been this high previously, senior analyst Tim McRae said.

“However, if we are to look at cattle prices in terms of percentage changes recorded across a sustained period, this recent surge is not unprecedented. From November 2014, through to September 2016, the EYCI recorded a 111pc increase, going from an average of 338c/kg cwt to a then “unprecedented” 712c/kg cwt. While the 22-months rise was on the back of improved seasonal conditions, it was also from a very low starting point in November 2014… again following a devastating period of dry conditions,” Mr McRae said.

Rebuilding intentions and restockers clamouring for young stock put the momentum into cattle prices through 2015 and into 2016, assisted by improved seasonal conditions, including a very wet winter in 2016. Sounds familiar?

Looking further back in the history of the EYCI, there have been similar periods of large percentage gains. Comparing monthly averages and percentage changes over a one-year-period:

- April 1998 – April 1999 = 45pc

- September 2000 – September 2001 = 39pc

- November 2002 – November 2003 = 43pc

- December 2009 – December 2010 = 36pc

- November 2014 – November 15 = 73pc

- March 2019 – March 2020 = 72pc

So, in conclusion, 2021 is unprecedented in terms of absolute cattle price levels, but the industry has seen similar run-ups in previous periods, albeit, from much lower price levels.

Prices “Unsustainable”

Any cattle producer that has sold in the past several months would acknowledge that the current price levels are unsustainable, but at the same time, are in no rush to see a sustained decline, Mr McRae said. The boost in incomes for 2020-21, while most likely partly offset by reduced total head sold, will have gone some way to paying off drought incurred debts.

Any recent forecasts for Australian cattle prices into the second half of 2021 indicates a decline – although, given the recent highs, this is not a difficult stance to take. Indeed, while the consensus is a downward trend to come, it will be the speed and timeframe in which this occurs that is crucial for all participants.

Of the organisations that look ahead and forecast cattle prices, the Australian Bureau of Agricultural and Resource Economics provides the longest view ahead, while NAB in its Rural Commodities Wrap, put some near-term numbers for the second half of 2021 on the table. In December 2020, AuctionsPlus also had its first foray into price forecasting.

From ABARES, the national weighted cattle price is forecast to decline every year through to 2025-26. In the near term, the average price is expected to be back 7pc in 2021-22, another 7pc in 2022-23, and then 4pc through to 2023-24. Indeed, from 2020-21, through to 2024-25, the weighted national cattle price is forecast to contract 19pc.

In its February Rural Commodities Wrap, NAB boldly predicted the “EYCI at 700c in Q3 and 650c in Q4 2021”. However, it would only be fair to NAB to also provide the next sentence for context, “It is important to consider that there is substantial uncertainty around cattle prices for the coming year, with weather events, currency moves, global demand and global supply (particularly if processor capacity improves in the Americas), all major influences”.

Finally, AuctionsPlus’ inaugural cattle price forecast released in December 2020, had the market back 5-10pc by the end of the June quarter in 2021, albeit based on a EYCI of 800c/kg cwt at the time of publication.

Given the surge in the EYCI in early 2021 and additional information becoming available, an EYCI between 790-820c/kg now looks more likely by the end of June 2021.

“Unbalanced”

The resurgent confidence and record prices received for cattle during 2020 and early 2021 is not an evenly shared experience across the industry. Whether it be regionally, due to poorer rainfall through central Queensland, or structurally, due to the uneven burdens felt through the supply chain, massive inequalities are being created. These inequalities cannot last for too long, as any chain with a compromised link will ultimately be weaker, shorter, and disadvantaged over the long term.

As a supply chain that is structured upon margin and the next-in-line “paying more”, the cattle and beef industry is almost always unbalanced at any point in time. During drought periods, the growers take the burden of the negative, while processors and exporters accept the positive. In contrast, like today, the growers are positive, while the negatives being made by the processing and exporting links of the supply chain are substantial and growing, and at risk of overusing a word, unsustainable.

Given the extent of the drought in 2018 and 2019, no-one would be begrudging the prices and conditions currently being experienced. Indeed, cow and calf producers are the nursery that ensures the rest of the cattle supply chain has product to be utilised in years to come. As we can see today, sequential years of drought and herd liquidation has the national herd at a multi-decade low, which has “shortened” the volume available within the supply chain upon the return of a favourable season for producers.

The Australian cattle herd is a very large and diverse entity, that can take a long time to turnaround – with biology and weather the key drivers. This means that those in the later stages of the supply chain may be looking at 2022 at the earliest to see any substantial benefit of the 2020 and 2021 seasons. Thus, two or three years of being on the negative financial end of tight supplies and high cattle prices can only be withstood by the strongest and best forward planned operators – which was no different for producers through drought conditions of 2018 and 2019.

Source: AuctionsPlus