In this opinion piece, MLA managing director Jason Strong counsels about letting the EYCI impact industry sentiment too much, suggesting in a year like this, other indicators like processor cow or heavy steer should be watched more closely

THIS year is very different year to 2022, especially in the cattle market. In 2022 the herd rebuild was very much alive as Northern Australia received its first above-average wet season since 2016.

As we move through 2023, the herd rebuild is stabilising as paddocks become more heavily stocked and the weather normalises.

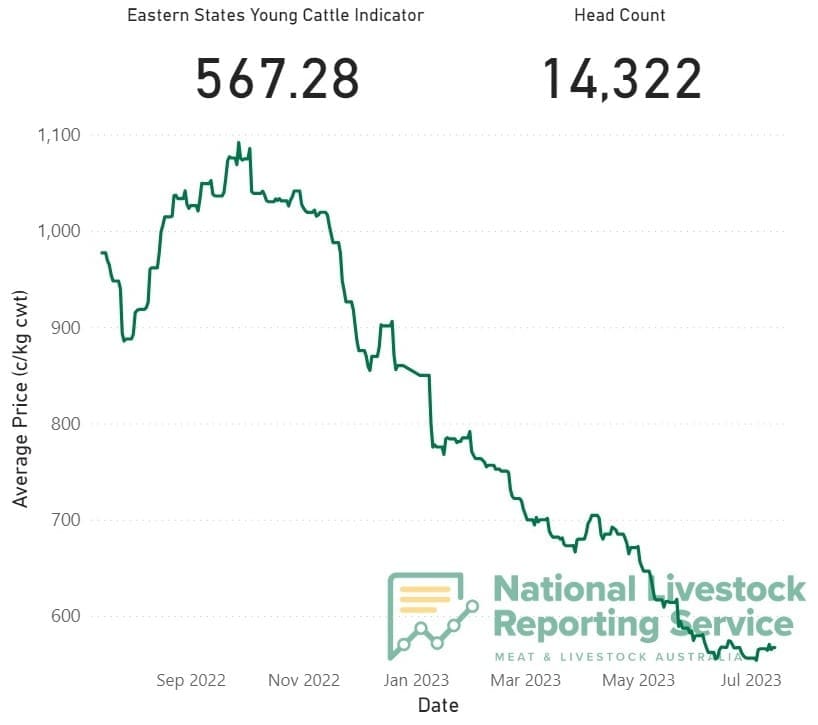

The Eastern Young Cattle Indicator, or EYCI, is a price indicator for animals that meet the following specifications: vealer and yearling heifers and steers with fat and muscle scores of C2 and C3 and with live weight from 200kg to 400kg.

As such, it is an indicator that tracks future sentiment. It is not reflective of the majority of animals being transacted. Only ten percent of EYCI cattle are purchased by processors – most animals that meet EYCI specifications are bought by restockers or feedlots.

As the herd rebuild enters a period of stabilisation, it is imperative that stakeholders in the cattle industry recognise this, and ensure they are using the correct indicators to understand pricing trends.

The EYCI (graph image at left) is not the best indicator to gauge pricing trends, especially this year.

As more finished cattle hit the market, producers and stakeholders should be following the processor cow or heavy steer prices more closely.

Following three years of above-average seasonal conditions, the national herd rebuild is now entering a period of maturation. As a result, in 2023 the national herd will reach its highest level since 2014, and in 2025, the herd is expected to reach levels not seen since the 1970s.

With more cattle available, there has been an increase in the number of cattle being sold and slaughtered. This higher supply of cattle has put downwards pressure on prices. At the same time, demand for young cattle, and especially young females, has softened as properties start to reach their maximum stocking capacity.

This increase in supply and softening of demand has impacted the young cattle market the most with the EYCI easing to sit at 573c/kg this week.

While this appears to be a significant drop, the price of young cattle in the 2020-2022 period was at historically high levels that were never seen before. During this three-year period, restockers were fiercely competing to secure whatever young cattle they could.

Every time a drought breaks, the price for young cattle surges before normalising after around two years. We experienced a similar trend in 2015 and 2016.

The processor cow and heavy steer indicators have not fallen by as much as the EYCI. The heavy steer price is back 10pc less than the EYCI as there remains strong processor demand for animals and there are fewer finished animals than there are animals who were conceived or born in the last year.

As the young cattle in the herd reach processor weights, producers should look at these two indicators as they will be more reflective of the prices they are receiving.

As an industry we must not let the EYCI impact our sentiment too much. It is an indicator focused on rebuilding sentiment. Putting too much weight on the EYCI in the herd maturation phase could fuel further and unnecessary price drops.

The market is fundamentally operating the way it should in the first six months of this year, with supply, demand the cyclicality of the cattle cycle all playing roles in how prices are performing at the current stage.

Jason Strong is the chief executive and managing director of Meat & Livestock Australia.

There is a big flaw in what Mr Strong says.

Processor prices are not publicly available information.

Some time back Teys did put their grids up on the internet for anyone to view, and it was very interesting reading, comparing the prices from their different plants. But as far as I know no other processor did the same, so they stopped doing it.

Note quite factually correct, Paul. There were at least four large eastern states processors that were for a time making their direct-consignment grids publicly available. They included Teys (multiple sites), Bindaree, NH Foods (multiple sites), and TFI. Some of those disclosure decisions, at least, came as a result of the Senate Inquiry recommendations – but equally, some pre-dated the Senate Inquiry. For a period Beef Central provided readers with an access point to those publicly-accessible price grids, but over time, the processors involved stopped publishing them. Excess cattle supply during the drought may have been a factor, but that’s pure speculation. The big obstacle to simply publishing grids in this way has always been not being able to compare ‘apples with apples,’ from one competitor to another. Processors, understandably, want producers with cattle to sell to pick up the phone. Editor

“Grass fever” has always been a disease affecting Graziers with too much grass with both sheep and cattle producers fueling young cattle prices when they have a surfeit of available feed.

Heavy steer prices have seen a significant decline that has accelerated this year down about 25% in the past 12 months. We have not seen a concomitant fall in retail prices and it will be interesting to see quarterly and monthly ABS figures when they are released later this month.

The Australian Bureau of Statistics collect retail prices and reports them monthly and quarterly including retail indicators on the categories Beef and Veal and Sheepmeats. These meat prices contribute to the inflation index which is then used as a principal measure the Reserve Bank looks at when considering interest rates.

As well as there being indicator prices on livestock, there should be indicator prices published on retail to allow some transparency at this end of the supply chain. A number of previous inquiries into the meat industry recommended developing tools to improve transparency in the meat supply chain beyond the farm gate. We are yet to see these.

I would really like to see simon quilty’s opinion on this issue and others. I think jason has a point. But i have a few stats front of mind that simon pointed out a while ago. One of the regarding our rebuild numbers and how every time we have a rebuild peak herd numbers never reach previous rebuild highs. I think our potential bottle neck is going to be our lack of leadership federally with our relationship with Indonesia and the slow loss of interest between our two countrys which was apparent well before prices soared. This could push vast numbers of cattle south regardless of the weather. Cheers Matthew Della Gola