US cattle on feed numbers are a million head higher than this time last year

AN alarming buildup in US beef production, and potentially, exports, is sending ominous signs for Australian exporters, particularly for grainfed beef.

The US Department of Agriculture’s most recent report estimated US cattle on feed as of March 1 at 11.715 million head, up one million head, or 8.8pc on the previous year. That’s the largest March inventory seen since 2006. USDA reported that US feedlots placed 1.82 million head of cattle on feed in February, 7.3pc more than a year ago and 12.9pc higher than the five-year average.

USDA has put US beef production in the second quarter up a massive 13pc from a year ago, perhaps illustrating the ‘nervousness’ and ‘uneasiness’ (both terms used by US industry analysts in commentary last week) seen in cattle futures about US beef/cattle prices in the northern hemisphere spring and early summer.

US cattle futures have continued to drop alarmingly during March.

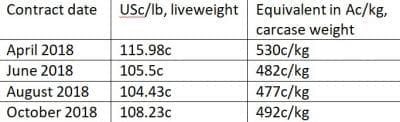

The table set out here shows US live cattle futures contract pricing in USc/lb for April, June, August and October, and compares this with Australian c/kg carcase weight equivalent. Note that these sums can vary a little, depending on how respective US/Australian grainfed trim value is accounted for, and standard carcase trim in each country.

The table set out here shows US live cattle futures contract pricing in USc/lb for April, June, August and October, and compares this with Australian c/kg carcase weight equivalent. Note that these sums can vary a little, depending on how respective US/Australian grainfed trim value is accounted for, and standard carcase trim in each country.

But regardless, it still shows a massive deficit in value between Australian grainfed carcase price competitiveness based on forward pricing later in the year (see references below), compared to what’s coming out of the US. The June US Futures figure, for example, is this week calculated at A$220.49 per carcase cheaper than Australian forward contract prices for grainfed, and August, $227.

Sanger Australia’s Sydney-based meat trader, Stewart Hanna suggested US cattle futures should be used only as an indicator, however.

“At the moment, there’s a big disconnect between actual cattle prices in the US and US cattle futures. They are what they are, and in the end, movements in the futures market like this causes an attitude, and fuels the sentiment in the market,” he said.

“That’s the issue we have at the moment.”

US buyers are apparently becoming reluctant to forward-purchase, anticipating that meat prices will fall.

“But regardless of the futures numbers, in the end, these big numbers of US cattle have to come to market, when they have finished their time. It’s been increasingly evident since the end of last year that there’s a huge competitive challenge coming,” Mr Hanna said.

“The issue is that the US is going to continue to kill very large volumes of cattle, and there’s going to be plenty of meat around. Are the carcase weights going to be particularly heavy? Probably not, because there are a lot of cattle out of drought-affected areas in the US now going onto feed. So the weights might not be huge, but the number of cattle coming forward will be huge.”

Mr Hanna said the competition impact would be seen right through the export market spectrum, from chilled, quality grainfed cuts exported into Japan and Korea, right through to lean trim into the US, north Asia and elsewhere.

Customers were telling him that when the big wave of US cattle came mid-year, end-users could push the abundance of knuckles, outside flats, clods and other primals into the grind, making it tougher for Australian manufacturing beef exports.

“Apart from one or two big corporates, a lot of US meat customers have currently got their cue in the rack,” he said.

Offsetting the looming surge in supply out of the US, was strong prospects for greater US consumption this year, however.

“When I look at US CIF prices on a range of domestic cuts at the moment, beef is pretty affordable,” Mr Hanna said. “Especially in the US, where the economy is OK and there’s a bit more disposable income in the system, big retailers and food service operators plan to run specials on beef, this northern hemisphere summer. I think that will soak-up at least some of this big beef surplus. To have beef on special is a good thing, because if they can afford it, American want to eat beef over chicken or pork.”

Australian grainfed pricing show signs of softening

The impact of US grainfed buildup is starting to be reflected in forward pricing for 100-day grainfed cattle in Australia.

Several large grainfed exporters told Beef Central they anticipated trading conditions to get ‘particularly nasty’ during the winter months, and further ahead.

While some dedicated grainfed exporters yesterday had quotes for July delivery around 535c/kg for grainfed export cattle, others have started to decline. And most significantly, neither of the nation’s two largest beef processors today were making forward price offers for July-August. Readers can draw their own conclusions about the reasons behind that.

Spot pricing yesterday for 100-day grainfed kills in Queensland in coming weeks ranged from 520-540c.

“A million head of extra US cattle on feed is a lot of cattle,” a major export processor who watches the US market closely told Beef Central yesterday.

“Those cattle are going to die – they are on feed, and are locked in for slaughter during the second or third quarter. They will be liquidated when the time comes – the US industry will not just sit on them,” he said.

Whether that extra meat was absorbed into the US domestic market, or was placed into export to markets like Japan, Korea or elsewhere (US beef exports in February were up 15pc year-on-year), it was going to impact the Australian industry, he said.

One of the challenges faced by the US this year (discussed by Beef Central’s regular columnist Steve Kay in this recent monthly item) was whether the US processing sector in fact had the capacity to handle such a large volume of slaughter stock.

“Some may accuse us of being too pessimistic, so far as our forward pricing on grainfed ox goes, but given what’s coming, we are just not prepared to let this get away,” a large processor said. “We’re not going to ‘blow our brains out’ (suffer a huge financial loss) by paying over the odds for grainfed cattle, like the industry did last year.”

Another multi-site export processor said the current (spot) market for 100-day cattle was still in a ‘little window of optimism’ since the downturn in production, writing a little more money in the short term.

“But we are of the view that trading conditions for grainfed beef will get exceptionally difficult during the middle of the year,” the company spokesman said.

“That view is reflected in our forward contract pricing for July, even though some of our competitors apparently do not yet share it. Somebody is going to be proven right, and somebody wrong,” he said.

“No processor wants to get back to the situation seen last year, where losses got to $300 a head and more on forward contracted cattle, during the last six months of 2017. We have no appetite for that.”

While numbers of so-called ‘program’ cattle (committed to long-term supply agreements with customers) are likely to be less affected, numbers of ‘non-committed’ export weight cattle going on feed are likely to continue to come under pressure, Beef Central was told.

‘Full weight’ yet to be seen, says MLA

MLA chief market analyst Scott Tolmie said Australian export beef prices had held up relatively well so far this year, but he did not think the ‘full weight’ of some of the US beef production increases had yet flowed through.

“The main impact is yet to be seen,” he said.

“The current US cattle futures pricing should serve as a bit of a ‘watch-out’ for Australian exports. There’s more and more talk in the US industry about what’s coming, later in the year.”

“Further declines in US cattle futures could be in the pipeline this week as the effects of a potential ‘trade war’ between the US and trading partners over steel and aluminium (causing weaker economic growth) have a negative impact on fed cattle trading – something equity markets have already started to consider,” Mr Tolmie said.

- Steve Kay will explore the topic of US supply and demand further in his upcoming monthly column for Beef Central.