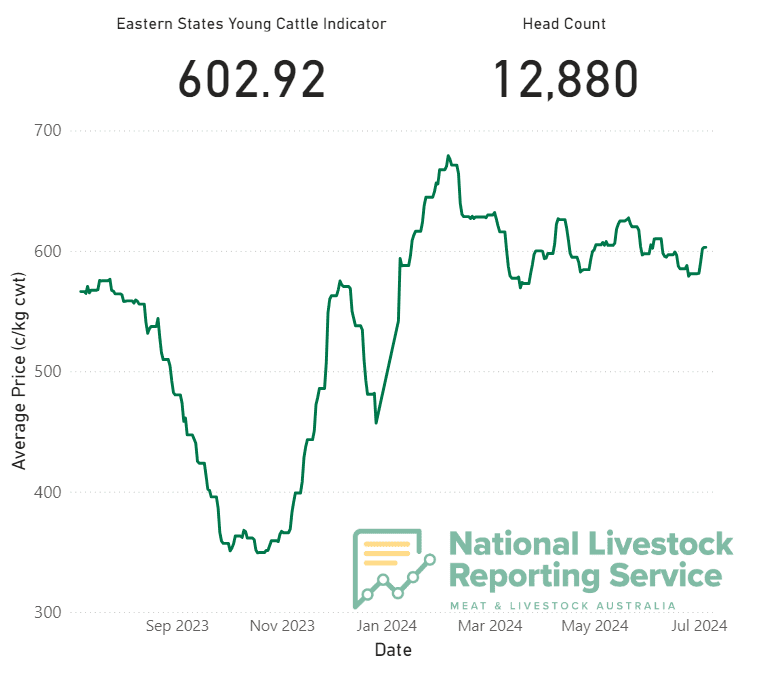

AUSTRALIA’S benchmark Eastern Young Cattle Indicator has continued its resilience for 2024, jumping back above 600c/kg carcase weight after dropping for two weeks.

The EYCI climbed 21.85c this week and is up 36.74c on this time last year. The increase in the past week continues what has been a remarkably stable year, which saw the indicator climb to 679.14c in February and hover 20c above and below 600c ever since.

Click to enlarge

Elders economist Richard Koch said processing capacity appears to be keeping up with the large numbers of cattle coming forward.

“I have heard processing capacity is almost full throttle, a lot of plants are working additional days and shifts,” Mr Koch said.

“The other thing started impact markets is that you are starting to see less cattle available in the southern states – the dry autumn really prolonged the turn-off down there and that has started to ease up in recent weeks.

“Having enough capacity to keep up with the supply coming on has been a major constraint to prices in the last quarter.”

As Beef Central’s Weekly Kill segment pointed out on Tuesday, southern processors have been a presence in Northern New South Wales and Southern Queensland selling centres this week, which has largely been credited for the increase in prices.

“Basically, northern processors had the market to themselves for a while, but the southern guys are really starting to provide some competition now,” Mr Koch said.

“Any slowdown in Australian supply will push local cattle prices higher.”

US showing signs of herd rebuild

On processor margins, Mr Koch said all eyes were on the United States, with signs of a herd rebuild starting to show. The US has been in a drought-induced herd liquidation for the past three years, which has been competing with Australian export markets.

He said the US market can turn from Australia’s biggest competitor to its biggest customer when its production starts to fall and it starts to rely on imports.

“The US is still maintaining its production by feeding to heavy weights, so production is not going to fall off a cliff,” he said.

“But it definitely looks like they have tighter availability of beef, they are becoming pretty big net importers of beef now.

“They are importing a lot of cattle from Mexico, which another way they are keeping up production.”

Mr Koch said he had been looking through some other indicators of herd rebuilding in the US. He said lean beef prices in the US reached record highs in April before coming off a bit in recent months.

“The US beef exports for May was the lowest for four years. There has been a drop in cow slaughter, feedlots placements fell in May but went up again last month,” he said.

“We are seeing that decrease in production from the US in some of our markets in North Asia, which I suspect is giving us a boost there.

“They are still putting a few heifers through the feedlots and that will be big sign of a rebuild when they keep their heifers out of feedlots.”

Is more restocker demand on the horizon?

On Australia’s domestic market, restocker-type cattle have been trading cheaper than a lot of other cattle – as evidenced by the disparity between steers and heifers reaching an eight year high earlier this year.

Asked whether he could see any cattle going back to the paddock in some of the dry areas of the country, Mr Koch said there was not much evidence of it.

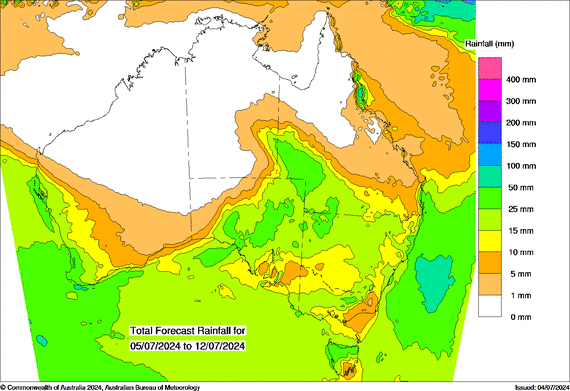

BOM eight day forecast predicting rain across most of the east coast

However, he pointed to this week’s Bureau of Meteorology eight day forecast which is predicting rain across most of the east coast, which might stoke some interest.

“If they get some rain then there might be some restocker interest because those type of cattle are quite cheap at the moment,” he said.

“Most of Victoria, most of South Australia and a good chunk of Southern NSW have been waiting for more rain and even if they get rain at the moment they are probably not going to grow much. But there might be some restocker interest in Northern NSW and Qld if they get rain.”