FUELLED by an injection of optimism since November’s widespread rain, there’s been a spectacular late 2023 season rally in Australian feeder steer prices over the past four weeks.

Heavy flatback feeder steers that were being quoted in the paddock (ex Downs) at 230c/kg in the first week in November are today making around 330-335c/kg – a cool $1/kg liveweight lift, worth around $450/head on a typical 450kg heavy feeder.

The NLRS feeder steer indicator, based on saleyards results for feeder-weight cattle, has mirrored this trend, lifting 97c/kg since this time last month, and 24c/kg over the past week, alone. The indicator today sits at 303c/kg liveweight. Visit Beef Central’s home page Industry Dashboard graphs to see the pattern, this year and last.

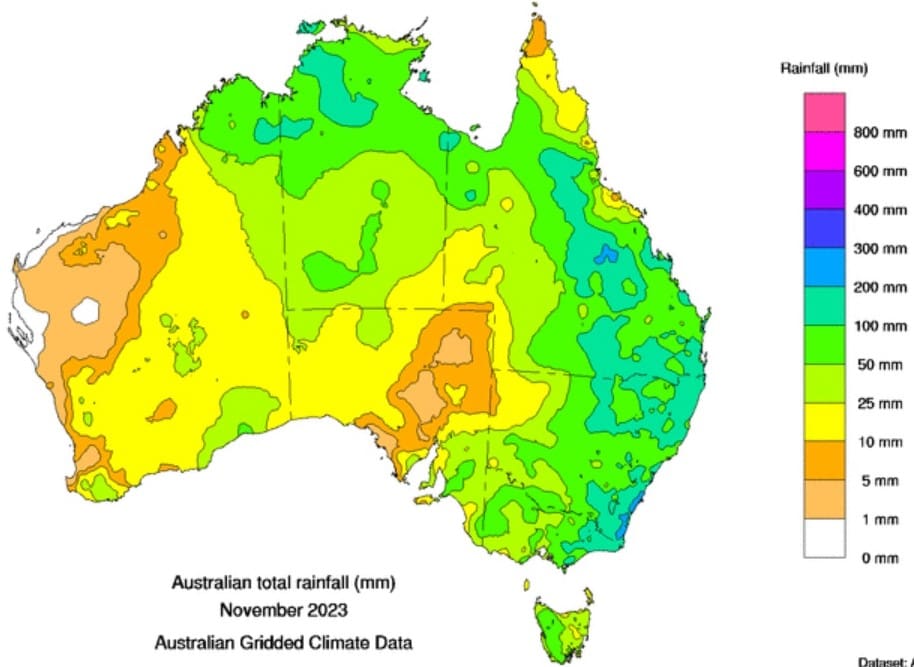

The November rainfall map below, provided by BOM, tells the back-story on recent feeder price movements.

“Everyone knew it would happen when it finally rained enough, but it’s still taken people a little by surprise, especially how quickly its changed,” one grainfed supply chain manager told Beef Central yesterday.

“But equally, nobody really expected the market to fall away as quickly as it did during the dry months September-October,” he said.

As encouraging as the current feeder price rally is, it still falls far short of the red-hot prices seen this time last year, when similar feeders sold via saleyards were making around 445c/kg, on average.

As is often seen after rain, the saleyards channel was the first to react to the recent change in price dynamics, with feeders starting to rise sharply in price in sales from around 12 November.

Feeder steers +400kg C muscle score or better at Dalby this morning averaged 301c/kg and sold to 326c, while similar descriptions at Roma yesterday averaged 312c and topped 336c. Gunnedah yesterday saw feeder steers average 329c and top 338c.

The Stonex Angus feeder steer swaps facility currently has December 2023 bids and offers averaging 320c/kg, advancing to 370c for April 2024 delivery and 380c in May. Swaps forward prices have shown considerable movement, with May 2024’s quote up from only 290c as recently as late October.

Forward contracts on fed cattle not yet lining-up

Forward contract rates for March 2024 delivery* from Queensland grainfed processors on 100-day grainfed ox currently sit at 580c/kg carcase weight. That does not add up on today’s feeder rates and ration costs – even a 600c/kg forward price does not look particularly attractive, one stakeholder said, with some big negative margins still attached at rates like that.

However March forward contracts on grainfed finished cattle were evidently set prior to the full impact of November rain across eastern Australia.

* Editor’s note 7.12.23: The original version of this report published yesterday incorrectly suggested the forward contract price related to April delivery cattle, not March. The contact we spoke to accidently referenced the wrong month during the conversation. No forward contracts have yet been issued for April, as far as Beef Central is aware. A separate correction will be published today.

A bigger inflow of saleyards cattle coming forward this week may stop the feeder market from getting any dearer for the time being, with big yardings seen at Roma yesterday and Dalby today.

In Queensland at least, there is still little evidence of a margin for Angus feeders over flatbacks, with paddock offers for Angus around 330-335c, back to around 300c in southern states.

The absence of the traditional Angus premium over recent months suggested two things, one program manage said: better supply of Angus-type feeders relative to other bred types, and the fact that better quality Angus type fed beef had struggled in international markets since mid-year, due to cautionary spending by consumers faced with rising living costs, inflation and interest rates.

At some point an Angus feeder premium will re-emerge, but how big is open to speculation, he said.

“Meat market signals have been that food service customers overseas, particularly, have not wanted the volume of more expensive Angus-type beef, as people tighten their budgets. The Wagyu beef market has experienced a similar trend, especially out of China, Korea and other parts of Asia.”

Will US demand for chilled cuts next year drive feeder prices higher?

Some stakeholders are now asking whether the change in seasonal fortunes is the only reason for the recent feeder price rally.

As described in this story yesterday, there’s growing expectation of sharply increased demand for Australian grainfed chilled cuts out of the United States next year, as the US beef herd approaches 50-year lows due to drought liquidation. This would add competition and demand from traditional grainfed chilled customers like Japan, Korea and China.

One grainfed supply chain manager said 100-day cattle going on feed during the last week in December would be due to close-out around April 8 next year, after 105 days on feed. For 150-day cattle, the close out would be early June – by which time the US market is forecast to be in significant deficit for chilled grainfed cuts.