WHILE lotfeeders are enjoying price relief in feeder cattle procurement through winter, a declining trend in forward pricing on 100-day grainfed slaughter cattle this year and rising feedgrain prices are keeping trading budget margins squarely in the red for the time-being.

There’s been a small 12c/kg recovery in the NLRS feeder steer indicator (saleyards based) over the past four weeks, sitting today at 321c/kg. That’s still more than 130c/kg behind this time last year, when the feeder market was still red-hot.

The market for heavy flatback feeders bought out of the paddock ex Darling Downs last week was around 335c/kg, having sat around 320c/kg for a period earlier, before firming heading into late June.

The market for heavy flatback feeders bought out of the paddock ex Darling Downs last week was around 335c/kg, having sat around 320c/kg for a period earlier, before firming heading into late June.

That trend was also reflected in AuctionsPlus heavy feeder type steers offered last week, showed a rise of 20-25c/kg in what was generally a flat market, with buyers willing to pay up for quality.

Feeder supply was described as ‘adequate’ by grainfed supply chain stakeholders spoken to last Friday for this report, but perhaps not as abundant as some had anticipated earlier.

But price movement has been dramatic since the start of this year. Similar feeder steers pre-Christmas were still making 450c/kg, coming back at least 110c since then, worth around $520 on a typical 450kg feeder this week.

There appears to have been a substantial reduction in Angus feeder steer premiums in recent weeks, relative to flatback types – some saying the price difference is now less than it has been at any time since the drought started in 2019.

Ration prices near record high

There’s considerable noise evident in feedlot ration prices presently, ranging from $500/t to as high as $550/t. At the upper end, it’s as high as ever reported in Beef Central feedlot breakeven reports stretching back 13 years, with the figure rising around 10pc over the past six months.

What’s unusual is that ration price levels like this normally align with periods of severe drought (high feedlot occupancy plus scarce local grain supply), but are happening this year during reasonably benign conditions.

A surging feedgrain price is a big part of that, but other ration inputs, like cottonseed, have also gone up by $100/t in the past month, as conditions dry off and demand rises.

As Beef Central’s regular weekly feedgrain report has shown, feedgrain prices have risen sharply since Russia withdrew last month from the Black Sea Grain Initiative, throwing Ukraine grain shipments into jeopardy.

SFW wheat ex Downs was quoted at $432/t spot on Friday, up another $7/t on the previous week. The severity of dry conditions in northern New South Wales has growers and traders increasingly nervous about the impact of a dry spring on volumes available to the northern stockfeed market, where more livestock are going onto feed as pastures dry off.

New season grain, which normally trades at a discount off the header later in the year, is this year being priced at a premium of $10-$20/t, Beef Central was told.

Cost of gain

Picking a mid-point in current Downs feedlot ration prices this week of say, $520/t, it delivers a cost of gain in our typical feeder steer (2kg/day ADG, consumption 15kg/day, NFE ratio of 7.5:1 (as fed) – see full details at base of page) of 362c/kg. That’s based on this week’s feeder purchase price of 335c/kg.

That delivers a current breakeven figure on grainfed export steer of around 680-690c/kg.

Forward grainfed bullock pricing

Queensland grainfed processors offering forward contracts on 100-day cattle on Friday were offering around 640c/kg for cattle delivered early November, suggesting a theoretical loss of around $150 a head on steers going on feed last week, on the above numbers.

The current forward contract grainfed price represents a small discount to spot prices on 100-day cattle (650c/kg available for spot 100-day in Queensland late last week – evidently there are few surplus non-committed cattle in the system), but the forward contract price has lifted 10c/kg from 630c/kg last month. Back in May, forward contract grainfeds were still around 660c.

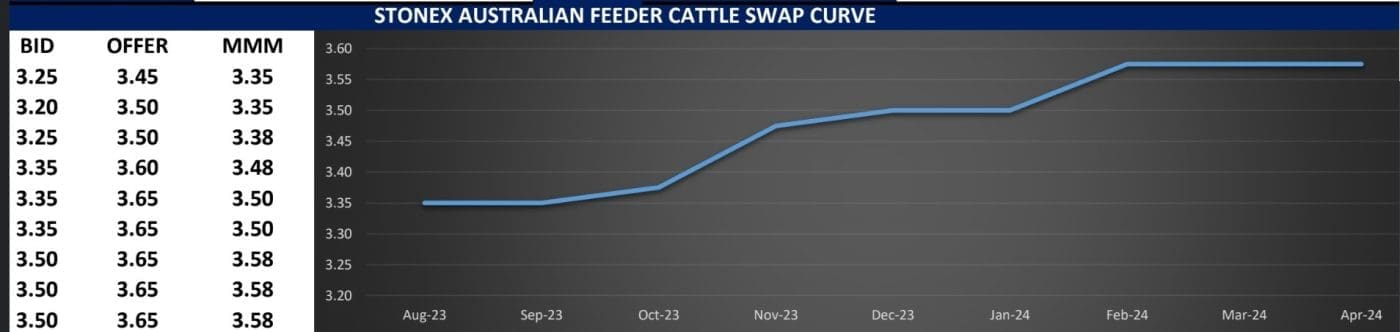

Looking ahead, the Stonex’s Swaps market is indicating a likely 5pc feeder steer price improvement over the next five months.

The Swaps forward bid and offer curve currently sits at 335c/kg out to September, rising in several steps out to 350c/kg by December, and pushing out to 358c/kg between February and April next year (see graph).

A grainfed supply chain contact told Beef Central that with an Aussie dollar today in the low US66s, export processors appeared to be back in a position similar to 2018-19, where they could price cattle quite cost-effectively, and still book cattle – despite the trading losses evident.

Increased use of inventory finance for feeder cattle, as part of a risk management strategy, may have contributed to that, he said.

Using an analogy to illustrate his point, he said it was “a little like a livestock transport contractor who takes a load to Mt Isa at full price, but can then only get half the price for a load coming back – he’s still going to take it, instead of coming back empty,” he said.

Beef Central’s 100-day grainfed trading budget calculation is based on a standard set of representative production variables, ex Darling Downs. The trading budget should not be interpreted as a comment on the viability of the lotfeeding sector – it is simply a gauge of the viability of the exercise of a buying feeder steers, sending them to a feedlot for custom-feeding, and then selling them at the expected grid price at an abattoir. The opportunity costs of the exercise are often missed by producers. The trading budget summary is built on a feeder steer 450kg liveweight, fed 105 days; 356kg dressed weight at slaughter; ADG of 2kg; consumption 15kg/day and a NFE ratio of 7.5:1 (as fed); $25 freight; typical implant program. Bank interest is included.