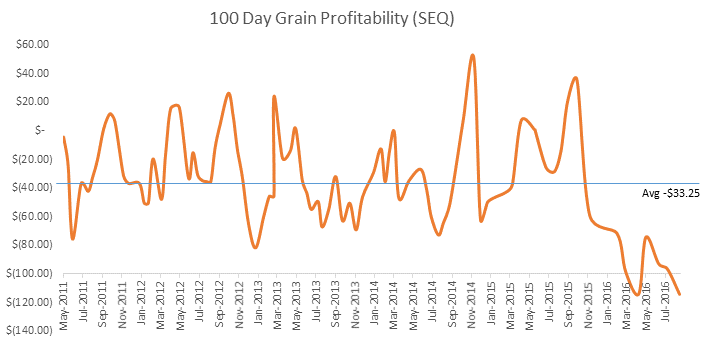

PROFITABILITY projections in Beef Central’s latest 100-day grainfed trading budget have again deteriorated, hitting a record-equalling low of minus-$114 in calculations put together this morning.

The graph published here, plotting our profitability in regular 100-day trading forecasts dating back to 2011, shows a dramatic turn of events after September last year.

This morning’s calculated result, based on our standard set of variables (accessible at the base of this page), equals the previous worst loss generated back in late April of $114 .

Losses since then have averaged well above $90/head, the graph shows.

There have been some substantial shifts in price variables applied since our last breakeven calculation on July 25, based on 450kg feeder feeders entering a typical Downs feedlot today, and closing-out for slaughter after 105 days on December 14.

Feeders ease 5c/kg

On the supply side, we’ve taken 5c/kg off our previous nominated price a month ago – but as lot has happened over the four weeks since then. Our July 26 record-high feeder price of 360c/kg declines to 355c, but the market for feeders hitting our spec in fact rose to the 370-375c range in the intervening period in early August, before easing. That rise was on the back of additional tightness in the market, and the rain influence on flow of cattle.

In the past two weeks, feedyards have given the appearance of trying to pull those heavy feeder rates back – but with mixed success. This morning, there were bids in the market at anywhere from 345c to 375c, but at its peak three weeks ago, there were bids in the 90s for the same cattle.

Today’s nominated figure of 355c – just 5c shy of our all-time record – values our typical 450kg flatback feeder at $1597, $23 short of last time. This time a year ago, the feeder market was certainly on the march, but was still sitting at 290-300c/kg, or at least $245 cheaper than today.

The early sign of an easing trend in young cattle prices is also clearly evident in the Eastern Young Cattle Indicator, now back 17c/kg off its recent record high.

It’s still way too early to suggest that the production sector has yet accepted that young cattle/feeder prices were way too high to be sustainable, but there’s growing sentiment to that effect, now being expressed by everybody from banks to stock agents to grainfed sector analysts.

While the June quarter feedlot survey statistics issued on August 13 are now well and truly dated, anecdotally, many Queensland yards now appear to be 15-25 percent down on occupancy levels recorded earlier in the year.

Another big change since last year is the big decline in custom-fed cattle, versus yard-owned cattle, in the mix. One trusted contact asked to speculate on the shift used the word ‘drastically’ to describe the reduction in custom-feeding, as a proportion of overall feeding operations.

It’s little wonder, given the turnaround in grass seasonal conditions and the extent of trading losses tracked in Beef Central’s regular breakeven since November last year, presenting a very testing period for most participants.

Worth keeping in mind though, as we have stressed before, the result published here is based on our chosen variables, which we argue are representative of typical programs across the industry. But having said that, better-performing cattle (i.e, gaining at 2.2kg/day, versus our prescribed 2kg) or with lower cost structures (i.e. cheaper feeder cattle), will produce a somewhat different result. But as always, it’s the trend which is of greatest importance in this exercise, not the specific profit/loss figure produced in each individual report.

As discussed in our earlier 100-day grainfed trading budget reports, another factor propping-up yard occupancy at the moment is the tendency to feed lighter cattle, especially while cost-of-gain (see figures below) is as compelling as it is, versus feeder purchase price.

As we highlighted last month, heavy feeders matching our ideal spec weight continue to be very hard to find, with many yards broadening their intake specs to take cattle much lighter than what they traditionally would. Some yards are currently accepting feeders for 100-day programs down as low as an unprecedented 300kg liveweight, in trying to secure numbers in a period of extreme shortage. In doing so, they are confident in the knowledge that it’s much cheaper on a c/kg basis to feed cattle than buy cattle to a weight. Effectively, cost-of-gain is much cheaper than purchase price, on a liveweight basis.

Some of those lighter steers will go into backgrounding programs on grass or oats, while others will go straight onto feeding programs to help fill pens, at a time when occupancy is presenting as a challenge.

The fact that the price premium for lighter cattle is currently quite modest, suggests there is some nervousness about buying, backgrounding and feeding those cattle for turnoff in say, six months’ time, when finished cattle prices might be in decline.

Ration price drops sharply

Biggest change in variables in this breakeven assessment is in ration price, which falls from $320/t a month ago to $290 today. It’s the first time we’ve seen it a ration cost with a ‘2’ at the front in this data-set since April 2013, and there’s the possibility it will continue to trend lower, feedgrain grain market signals suggest (click here to access Grain Central website for details).

Many lotfeeders now expect ration prices to continue to decline towards the latter stages of 2016, on the back of crop size, international prices, and also some reduction in demand from feedlots, due to cattle supply constraints.

The $290/t ration price in today’s trading budget delivers a total feeding cost of $454, down $47, and a cost of gain at 216c/kg, 23c/kg less than last time.

At today’s nominated feeder steer purchase price, total production cost is $2160, down $71/head since late July.

Breakeven eases to 612c

On the strength of the decline in feeding cost, the variables described above deliver a breakeven figure in today’s budget of 612c/kg – a drop of 20c from our record high recorded a month ago. But in truth, anything north of 600c/kg is still an unbearably high breakeven figure.

Heavy grainfed forward price grids from large grainfed processors this week for December, week two delivery, are currently at or perhaps slightly above 580c/kg. That’s a significant decline of 25c/kg since our last budget a month ago.

Based on the variables discussed above, it means that today’s trading budget delivers a loss on our current proposition of $114 a head. It’s equal to the worst result ever recorded in late April, when the market was driven hard by a deteriorating slaughter prices and weather conditions at the time.

Spot market comparisons

Looking at 100-day grainfed cattle heading for slaughter this week, forward contracts written on those cattle back in April-May were priced around 500-520c/kg. Compare that with the spot market this week for 100-day grainfeds, which is in a wide range from 580-615c/kg (dependent on the degree of individual processors’ determination to try to pull rates back).

What that means is that processors who forward-bought those 100-day cattle back then, are perhaps $285 to $300 a head better off than they are on spot market cattle today.

Despite the losses being recorded at the feedlot level, there’s been periods this year when processors have in fact bought some grainfed cattle (ie forward contracted stock) relatively well. That’s helped offset the very subdued meat trading conditions in international markets, and perhaps at least helps to offset some of the very expensive cattle bought in early 2016, when many processors were generating horrific losses on their higher-priced grainfed cattle forward-booked at the end of 2015.

Unfortunately, these cycles turn, and processors now face a cliff in front of them, with forward pricing again starting to look expensive in terms of opportunity to redeem that outlay. The better trading period for processors on forward-contracted cattle now looks like eroding fairly quickly.

Beef Central’s regular 100-day grainfed breakeven scenario is based on a standard set of representative production variables, ex Darling Downs. It is built on a feeder steer of 450kg liveweight, fed 105 days; 356kg dressed weight at slaughter; ADG of 2kg; consumption 15kg/day and a NFE ratio of 7.5:1 (as fed); $25 freight; typical implant program. Bank interest is included. It is important to note that variations exist across production models (feed conversion, daily gain, mortality, morbidity, carcase specification); from feedlot to feedlot; and between mobs of cattle. Equally, there can be considerable variation at any given time in ration costs charged by different custom-feed service feedlots. Click here to view an earlier article on this topic. For a more specific performance assessment on a given mob of cattle, consult with your preferred custom feeder.