An easing in feeder cattle and grain prices produced a modestly improved result in Beef Central’s latest fortnightly trading budget calculated on Friday.

An easing in feeder cattle and grain prices produced a modestly improved result in Beef Central’s latest fortnightly trading budget calculated on Friday.

While the impact and extent of the weekend weather event may yet be reflected on feeder cattle prices, the picture up to Friday suggested a moderately improved minus-$50 trading result on typical 100-day cattle entering the feedlot on Friday, and closing out in early June.

That contrasts with a $64 loss in the previous breakeven calculated a fortnight ago, and a negative $87 recorded in our year-opening budget calculated on January 11.

The forecast, based on typical 100-day flatback cattle (variables listed at bottom of page), continues to reflect the tough going, profit-wise, in non-committed grainfed cattle at present.

The outlook is not stopping heavy demand for custom-feeding space in southern Queensland feedlots, however, as western producers under seasonal pressure seek a grainfed solution to finishing cattle, almost regardless of profit prospects.

Lower feeder prices have also pushed more cattle towards feedlots, as evidenced in the latest quarterly feedlot survey.

There was a 10pc increase in cattle numbers on feed reported in the December quarter, lifting 75,000 head across Australia to 792,000 head by year’s end (see last week’s feedlot survey report here.)

For Friday’s trading budget, the prescribed feeder steer buy price ex Darling Downs was dropped 5c/kg on a fortnight ago to 170c/kg, on the basis of continued dry conditions in many western areas of NSW, Victoria and Queensland. Evidence suggests feeders fitting our profile are trading currently at 170-180c, while higher grade Indicus feeder cattle last week were trading in the mid-160s.

The feeder price of 175c is at its lowest point since our July 2011 calculation, when it sat at that level for a month or so before again starting to rise.

If those dry areas in the three eastern states receive 75mm of rain or more out of the current rain episode, however, there could easily be a 10c/kg liveweight improvement in feeder price, but it is too early to make that call yet, despite reports of some good weekend falls.

That fact remains that Eastern Australia has not experienced widespread rain across all beef regions since the early stages of 2012. Since then, relief has been patchy, at best, across the heartland production areas.

Friday’s breakeven 450kg feeder steer value apportioned at 175c/kg values him at $787, back $23 on a fortnight ago, and $179 less than what he was worth 12 months ago when he was quoted at 215c/kg, valuing him at $967.

Interestingly, that 18pc price drop in feeder value is exactly in line with the Eastern Young Cattle Indicator performance over the same period.

Ration price for Friday’s trading budget has been reduced $5/tonne from a fortnight ago to $305/t, on the back of a gentle easing in the feedgrain market. The downwards correction follows a $15/t rise in ration price seen over the previous three months, which left the figure up to a fortnight ago at its highest point since Beef Central started to report this data-set in May, 2011.

A factor in recent grain price strength comes from the demand side, with many Downs feedlots now at close to feeding capacity due to the effects of prolonged dry weather across NSW and Queensland. This has meant many feedgrain buyers have been more bullish in their buying strategies, which has probably exacerbated the market strengthening trend.

There was still some variance in finished ration price evident in down feedlots last week, however, with quotes from as low as $280 to $320/t.

The ration price of $305/t attributed in Friday’s trading budget represents a total feeding cost over 105 days of $470 on our trading steer. Total production cost is calculated at $1355, down $32 on our last budget, due to softer feeder and ration price.

Cost of gain, using our chosen variables (2kg/day ADG, for 210kg gain over 105 days) is also down a little to 228c/kg, from 233c/kg on February 6. This time last year, the cost-of-gain was 187c/kg on a $250/t ration price, about $55/t or 20pc lower than yesterday’s figure. Feeders back a year ago were worth close to 215c/kg, however.

The above variables deliver a breakeven figure in yesterday’s budget of 385c/kg dressed weight on a 100-day feeding exercise, down 8c/kg from a fortnight ago, and a bigger decline from a breakeven of 400c/kg in mid-January. That was the highest breakeven figure seen since the July-August period last year when it peaked at 402c/kg.

Current forward public grid prices from Southeast Queensland processors for June, week one, are around 370c, although there have been a number of cattle sold last week at rates below that. Friday’s grids suggested a figure of 365c for 100-day grainfed was common.

All that suggests a trading loss on Beef Central’s regular variables on Friday of minus-$50.

Basing the scenario on a higher Brahman content beast bought as a feeder at 365c, however, returns a figure close to breakeven. The offset, however, is that these cattle may not be as high in compliance.

That’s good news for a typical producer at Winton with Indicus cattle and deteriorating conditions. To them, a 370c/kg forward price is looking a ‘pretty good sell,’ under current circumstances. The added bonus for retained ownership structures could be some compensatory growth, if conditions have been under pressure for any length of time.

Looking backwards at 100-day cattle that went on feed in October at forward meatworks rates of 390c/kg, that compares with a spot rate today of 365-370c. That means the sellers of those cattle were in the money, while processors would be out-of-pocket on those cattle to the tune of $70-$90.

At the processor end, however, that result has been softened a little by a modest easing in currency since the start of the year. The A$ has been trading in a narrow range between US102-103.5c, in the past fortnight, in contrast with US107.5c this week last year.

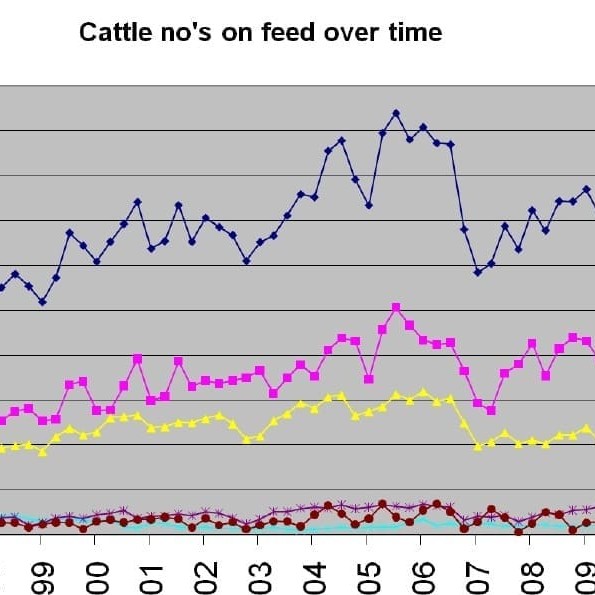

Greater consistency in feeding numbers

Some industry stakeholders looking at last week’s quarterly feedlot numbers survey were surprised that given the current dry interior conditions, figures for December were no higher than they were this time last year.

Some industry stakeholders looking at last week’s quarterly feedlot numbers survey were surprised that given the current dry interior conditions, figures for December were no higher than they were this time last year.

The graph of lotfeeding activity over time, published here, perhaps suggests a change of approach among lotfeeders, compared with the way they operated previously. The graph shows relative stability in numbers on feed over the past three and a half years, almost without regard to seasonal conditions, with numbers sitting in a quite narrow band between 700,000 and 800,000 head.

“Perhaps it suggests that despite the dry conditions and importance of feedlots in these times, it’s evident that more lotfeeders today are maintaining consistent production numbers, almost without regard to market influences,” one respected stakeholder said.

“In December 2011 there were 790,000 head on feed, and in December last year the figure was almost identical – yet seasonally, the circumstances could hardly have been more different,” he said.

“That suggests more feedlots are maintaining a higher occupancy of cattle (either custom-fed or feedlot-bought) as a business strategy – as opposed to being more reflective of seasonal conditions in numbers,” our contact said. “It reflects a stage of maturity in the industry, somewhat like what happen in the processing sector, where their business model aims to operate as close to capacity as reasonably possible.”

“If we had looked at the same scenario ten years ago when lotfeeding was good, numbers on feed were more reflective of the season, and how cheap the cattle were, and how much margin there was. Today more feedlots are looking at remaining closer to full, allowing them to operate more efficiently, and working hard to develop reliable markets to enable that to happen.”

“Therefore we are not seeing the huge variances we once saw in feedlot numbers, beyond the annual seasonal fluctuations.”

In some cases, feedlots have seen a drastic increase in the number of custom-fed cattle on their books since October, but their overall numbers have not reflected that rise, suggesting bought cattle numbers have been reduced, to compensate.

- Beef Central's regular 100-day grainfed breakeven scenario is based on a representative standard set of production variables, ex Darling Downs. They include a 450kg liveweight feeder steer fed 105 days; 356kg dressed weight at slaughter; ADG of 2kg; consumption 15kg/day and a NFE ratio of 7.5:1 (as fed); $25 freight; typical implant program. Bank interest is included. It is important to note that variations exist across production models (feed conversion, daily gain, mortality, morbidity, carcase specification); from feedlot to feedlot; and between mobs of cattle. For a more specific performance forecast on a given mob of cattle, consult with your preferred custom feeder