HIGHER ration and feeder steer purchase costs have pushed Beef Central’s latest 100-day grainfed trading budget calculation back out to a loss of $60 a head.

HIGHER ration and feeder steer purchase costs have pushed Beef Central’s latest 100-day grainfed trading budget calculation back out to a loss of $60 a head.

The calculation, performed yesterday using our standard set of variables (see full list at base of page), is based on our typical flatback 450kg feeder steer going on feed on the Darling Downs yesterday, and exiting the feedlot after 105 days on January 22.

The latest result is $27 worse-off than our last trading budget calculated three weeks ago, and a widening gap from our last projected net profit – a modest +$4 – posted back on May 16.

Based on current market signals, we have pushed our feeder steer purchase price out by 5c/kg to 175c/kg for yesterday’s budget. Since our last breakeven on September 19 the feeder market has been choppy, but feeder numbers on offer are now showing signs of tightening and some lotfeeders appear to be trying to gather a few more cattle around them.

Part of that is anticipation of shortage of supply, and higher prices, if and when a seasonal break occurs.

Significant rain across Queensland/NSW over the next month could easily see the feeder steer market lift 10-15 percent overnight, contacts said, and the other impact would be a likely drop on ration price, because a sorghum crop planting would start immediately in those areas where a crop can be grown.

Trade contacts tell Beef Central that another factor after widespread rain would be a sharp decline in pen occupancy in feedlots offering custom-feeding options, after a ‘fantastic’ six month trading period where all available pen space in Queensland and northern NSW yards has been soaked up by custom-feed customers facing extremely dry conditions at home.

That high demand on space has lessened competitive pressure on custom-feedlots, on their ration price margins. Widespread rain could see lotfeeders accepting narrower margins on feeding for others, in order to sustain pen occupancy, sources say.

Saying that weather could influence grainfeeding trends in coming months might sound like ‘stating the bleeding obvious’, but it applies more acutely than ever under the current market circumstances, both from a grain supply/price and feeder supply/price perspective.

A number of southern Queensland processors have kicked their direct consignment rates for slaughter cattle since Monday, suggesting they see slaughter numbers starting to tighten heading into November. Processor margins appear to remain very healthy, and the export trade appears to still have the capacity to handle whatever volumes of beef processors can procure.

Part of the reason for that is circumstances in the US, where the latest US Cattle on Feed report showed the smallest September 1 COF in the US feedlot industry in ten years. The total was below 10 million head for the first time since August, 2010, primarily because August placements into US feedlots were 11pc below a year earlier. Placements the rest of the year are also expected to be well below last year in US feedlots, leaving a void in fed beef.

Pricing our feeder steer for yesterday’s trading budget at 175c/kg values him at $787. That’s $22 higher than three weeks ago, and considerably improved from a record-low 150c/kg liveweight in our budget in early June when the steer was worth only $675 due to drought supply pressures.

A point worth noting currently, however, is that feedlots are reporting cracking feedlot performance, because of the good pick-up in cattle entering the pens, including some compensatory gain. For consistency, we have not adjusted the ADG in our formula (2kg/day), but some cattle currently on feed would certainly be doing better than that.

Ration price lifts

For yesterday’s trading budget, we have lifted the ration price to $335/t, although current feedlot pricing signals are mixed. Darling Downs wheat is currently priced around $290/t, a little less for barley.

While in Queensland grain is still a little on the short side, further south, southern NSW and Victorian feedlots are getting more grain around them at better prices. South Australia is shaping up for a near-record wheat crop, and Victoria is solid.

The $335/t ration cost applied in yesterday’s budget is a record-high for our breakeven report, dating back to May 2011, and the highest seen since the huge grain price spike in 2007-08.

It represents a total feeding cost over a 105-day program of $524. This, combined with the current feeder price, gives a total production cost of $1403. Surprisingly, that’s not the highest total production cost recorded – it was eclipsed during a period when feeder prices went to 215c/kg briefly in December 2011.

Cost of gain, using our chosen variables (2kg/day ADG, for 210kg gain over 105 days) has risen further to 250c/kg. This time last year, the cost-of-gain was around 213c/kg, representing a 20pc rise this year. Feeder steers back then were worth 190-195c.

Cost of gain, using our chosen variables (2kg/day ADG, for 210kg gain over 105 days) has risen further to 250c/kg. This time last year, the cost-of-gain was around 213c/kg, representing a 20pc rise this year. Feeder steers back then were worth 190-195c.

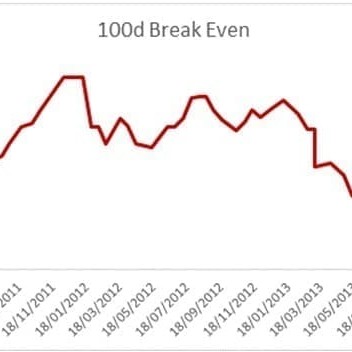

The combination above inputs suggest a breakeven figure in yesterday’s budget of 398c/kg – up 9c/kg on three weeks ago due to the lift in feeder steer purchase and ration cost.

As can be seen in the graph published above, that’s reaching historic highs, being exceeded only by breakevens that crept up to 412c in the early 2012 period when feeders went to 215c, and a brief slot during winter last year when the number touched 400c.

Forward pricing

Current forward public grid prices for 100-day ox from Southeast Queensland processors for January 22 close-out, have remained much the same since our last calculation, at around 380c/kg dressed. Cattle carrying higher content might be 10-15c below that, for some contracts.

The fact that processors are still keen to maintain high rates of kill reinforces the view that international meat demand remains solid, and there are still good margins present in grainfed export processing at those rates.

As mentioned in our intro, the variables outlined above deliver a $60 loss on our trading steer, closing out on January 22, which is $27 worse off than the $33 loss figure recorded three weeks ago.

Looking back at 100-day flatback cattle that went on feed in early July for slaughter this week, they had a breakeven at 380-396c/kg according to our calculations, on forward-contract meatworks rates then at around 370-380c/kg. That represented a loss of $43-$54 a head.

The market for spot 100-day cattle in Southeast Queensland this week is about 375c/kg. On that basis, processors who secured this week’s 100-day kill under forward contracts back in early July at 370-380cc/kg contracts are more or less line-ball in terms of result over buying those same cattle out of today’s spot market.

- Beef Central's regular 100-day grainfed breakeven scenario is based on a representative standard set of production variables, ex Darling Downs. They include a 450kg liveweight feeder steer fed 105 days; 356kg dressed weight at slaughter; ADG of 2kg; consumption 15kg/day and a NFE ratio of 7.5:1 (as fed); $25 freight; typical implant program. Bank interest is included. It is important to note that variations exist across production models (feed conversion, daily gain, mortality, morbidity, carcase specification); from feedlot to feedlot; and between mobs of cattle. For a more specific performance forecast on a given mob of cattle, consult with your preferred custom feeder.