US analyst Joe Kerns addressing the BeefEx conference in Brisbane last week

“HERE’S a little hint guys: it’s good.”

That was the under-stated entry-point made by visiting US analyst and agribusiness consultant Joe Kerns during a BeefEx conference address last week, referring to Australian beef’s extraordinary global prospects over the next few years.

Mr Kerns told delegates the revenue side of the global livestock business at present was “almost too bullish.”

“Beef prices are moving higher across the world. The compression of animals numbers is also happening. On top of that beef demand is moving even higher – and it should be a tide that raises all ships – I am convinced of this,” he said.

If he had to pick a date, it would be around July of 2026 when this current cycle reaches its peak, he said.

Mr Kerns’ business EverAg Livestock consults with US livestock producers, processors vets, researchers, mill operators and feed ingredient suppliers in 13 US states. He and his team assist clients with procurement and risk management activities related to hedging, ingredient purchasing, operational benchmarking, livestock marketing and business development.

He told last week’s conference that among the top beef producing countries, the US and Australia were almost dead even in terms of annual export tonnage, but the US exported about 15pc of its annual production, and Australia, 70pc.

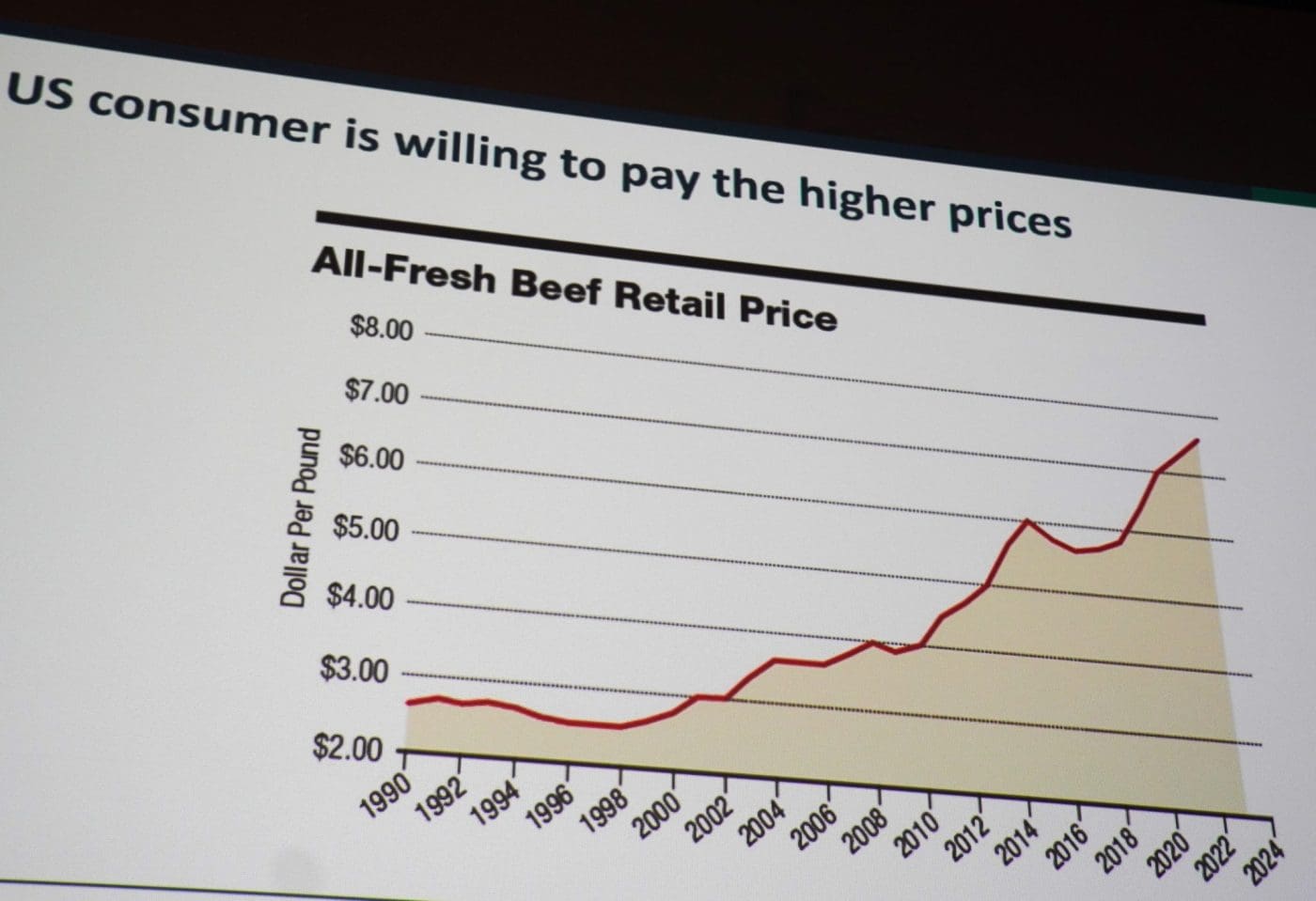

“At the same time as fresh beef prices are at record highs presently in the US, we want more,” he said. “This is a good sign for the rest of the (beef exporting) world. The US consumer is willing to spend more.”

When it came to exports, droughts across most of the globe (not just the US) were keeping the supply of beef reasonably high.

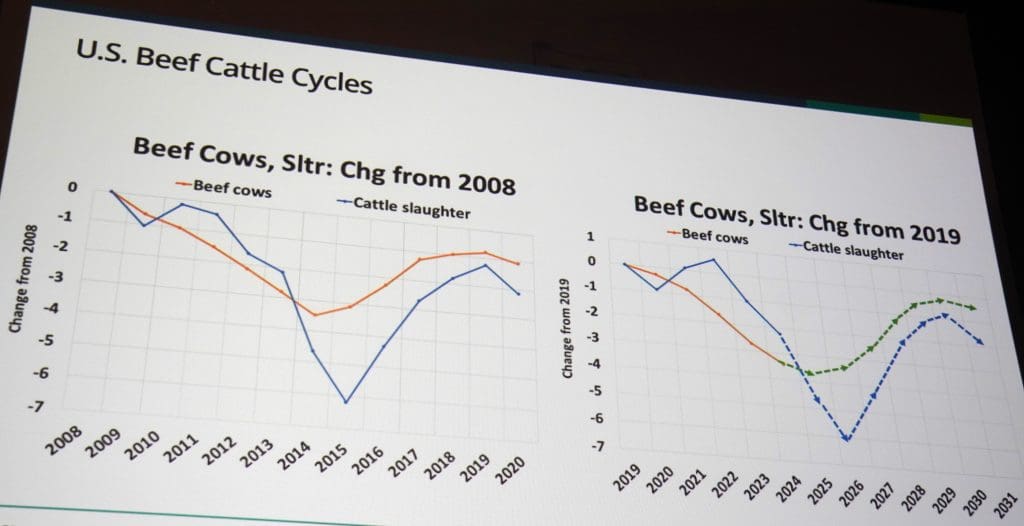

“But that’s going to change very quickly,” Mr Kerns said. “Since the 1920s, there’s always been this rhythm, and the US is now coming into a big dip in production (see graph), likely to reach its peak around 2026.”

The bulk of the US beef herd is located in southwestern states, which received some ‘decent’ recharges of rain in the first half of this year. Since then, drought had returned in some areas.

“We are not yet rebuilding the US beef herd,” Mr Kerns said. As a consequence, US cattle and calf prices were moving to their “absolute highest level in history.” (see graph below).

“The industry has never been here before – people don’t know what to do, and there’s nothing that’s going to stop this train,” he said.

US cow slaughter would ebb some time around the summer of 2025, and prices should move even higher, he suggested.

“We saw this back in the previous US drought of 2015, that led to the closure of some US processing facilities. Ten years later, the US is going to be right back in that position – except this time prices will be even higher.”

In terms of global meat imports, China remained dominant, closely aligned with beef supply out of Brazil.

In South Korea, the US was doing OK on the chilled side, but for frozen, Australian exports into Korea were doing “really, really well, and there’s a reason for it,” Mr Kerns said. “The US has Avian Influenza (bird flu) in its dairy herd, and suddenly the Koreans are testing for it.”

This is a really good set-up for the Australian beef industry. Any decline in future US beef exports due to lower production spelt opportunity for Australia.

Elsewhere around the world, the European Union market was in an abysmal state, Mr Kerns said.

“They are killing animal agriculture off as fast as humanly possible. The domestic EU beef supply is starting to contract, pork supply is also contracting right now.

“Mexico is itself going through an incredible drought that’s taking any access out of the US. There is no way we can duplicate what’s happening in 2024 (Mexican cattle movements into the US) in 2025.

“In Brazil, the southern regions where most of the cattle are experiencing dry conditions and won’t be rebuilding their herd whatsoever. Lack of pasture means Brazilian cows are coming to market, keeping Brazilian beef supply reasonably high for a period, before suddenly changing.

Australia’s proximity to Asia was also a factor, he said.

“China, the world’s largest meat importer, hates the United States and will do anything to avoid it. Does that work in the Australian industry’s favour for quality beef exports? Dang right it does,” Mr Kerns said.

“And logistically, you are a shorter ride across the ocean to the major Asian destinations for beef – both developing and developed countries.”

Having visited at Australian export processing plant during his visit last week, Mr Kerns noted the “ability and willingness” of Australian processors to cater for export customers’ requirements – “giving them what they want, as opposed to a US market, where we figure if they buy it and paid for it, they must have loved it.”

“You guys (along with the Canadians) do a much, much better job in servicing export customer requirements – putting together packages and products that appeal to the Asian markets. And Asia is absolutely where the game is, and where it is going to continue to be.”

World beef supplies tighten

All this was weaving a story that world beef supplies are starting to tighten up, and prices are moving higher, Mr Kerns said.

“US beef supplies are tight, with no signs of expansion; we have a drought in Mexico; Brazil is also tightening in supply, and the EU policy is killing all of animal agriculture. At the same time world beef demand is moving higher (measured by disappearance, at a price).

All this meant the medium term future for the Australian beef industry was as positive as it could possibly be, he said.

In contrast the Australian beef herd had rebuilt in 2015-16 after the earlier drought, and again in the past few years after the 2019-20 drought. Production would grow out to the summer of 2026.

“This is huge profits coming for the Australian beef industry, as near as I can tell,” Mr Kerns said.

“All of these global cycles are synchronised together. It’s just a complete coincidence that all the major production regions (barring Australia) are heading in the same direction. We went back through records and could not find evidence of a similar cycle in the past 60 years.

“This liquidation of animals is going to happen some time next year, and that’s what’s going to set the stage for the appreciation in prices. Global supplies will tighten up, and it is going to continue on through 2026 and 2027.

“It’s looking really, really good for Australian beef, from a world view – it almost could not be better.”

On top of that, the global grain situation was very comfortable, even in the face of some dryness.

“Global grain production remains reasonably high – even in the face of global conflicts. This is good news for our side of the equation – tightening beef supplies across most of the world and beef demand that’s moving higher, and seems to have no risk of substitution (chicken or pork for example).

“Being a pig guy from Iowa, I lament this at times – but we (pork producers) can’t seem to grab onto the tail of that increasing beef price that’s being seen. But this is good news for beef – beef evidently tastes better than any other form of protein, and consumers are prepared to pay for it.”

Production cycles

One of the challenges for beef, as opposed to pork or chicken, was long production cycles, Mr Kerns said.

“Chicken has about a six-week lifespan. The industry can change on a dime, but you can’t do that in the beef industry. It makes it a lot of fun to predict, because they are such long cycles – the industry can’t change direction in a heartbeat.”

Where could Kerns’ forecast go wrong?

So where could Joe Kerns’ super-bullish outlook for Australian beef go wrong?

There could be three possible impacts, he said.

The first was an escalation of world economic events. “If we suddenly find ourselves in economic collapse, on a global basis, maybe this analysis gets skewed a little. It might not change the supply side, but could change the demand and price side a little.

The second was carcase weights moving higher. “We’re already seeing this in the US. Carcase weights lifted 10kg last year in the US industry, but we can’t do it again and again – physically the infrastructure won’t allow it to occur.”

The third was the prospect of expansion of drought. If that occurs, it might impact the timing of the cycle, but it also meant that meat prices would have to move even higher.

One of the BeefEx delegates asked during question time whether even in the ‘worst case scenario’ where things changed, whether the next couple of years still looked bright for Australian beef.

“If I’m wrong in this rosy outlook I’ve presented for Australian beef, it’s just as a flat line – things aren’t going to go down. The ‘wrong’ provides a baseline of where we currently sit, not a decline. Maybe my timing might be off a little if circumstances change, but directionally, it’s an undeniable fact of numbers and biology,” Mr Kerns said.

“The world cannot replace its beef herd numbers as quickly as it needs to – simply because of the long reproduction and grow-out cycle.”

Hope the buyers at the rail know this, as my view is the current prices are pulling back on the old supply button our kills are full so no encouragement there, the processors seem to be happy with unstable supply scenario or don’t care as their profits are always there in some form or another, we are always the takers not the makers of price.

Sending that straight to the bank manager!

If you are a beef producer in Western Australia you would be scratching your head at the article.

Prices were gaining slow momentum and now they are tracking backwards.

We have even heard that Coles and Woolworths have told their feedlot suppliers that they need to pay less for feedlot entry stock. I thought that was illegal and they obviously didn’t get the Joe Kerns memo.