THE cost of production for grainfed export steers has grown substantially over the past year. But while finished slaughter cattle offer prices have moved in sympathy with that trend, feedlot operators and their custom-feeding clients will be hoping for much more this year to make the effort worthwhile.

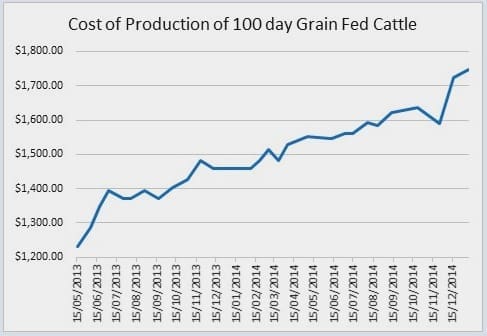

As can be seen in this graph, plotting the input costs attached to a typical 100-day program using Beef Central’s regular grainfed trading budgets, cost of production (COP) has risen relentlessly from around $1250 to a record $1746 a head over the past 12 months.

Click on image for a larger view

Our COP calculation is based on the two big inputs – feeder steer purchase price and ration price – as well as freight, interest, contingency, levy and induction costs. See base of this article for a full description.

While there was some upwards movement, also, in grainfed slaughter price last year, Beef Central’s trading budget has shown a loss, with only a few exceptions, throughout the 2014 year.

The abundance of cattle and the fact that finishing options were so limited due to drought were two reasons for that, but given any sort of decent season across Eastern Australia this year, owners of feeder cattle will be much more reluctant to commit feeders to grainfed programs unless they can see a profit in it.

That might be about to materialise. A direct consignment grid released yesterday afternoon by one of the nation’s largest export processors has spot market 100-day grainfed Jap ox delivery southeast Queensland at an unprecedented 450c/kg carcase weight for 0-2 teeth cattle, 5c less for four teeth. Seventy-day steer was quoted at 440c/kg.

Numbers like that – should they persist, or even improve further – will have a positive bearing on profitability in our future trading budgets, we’d suggest.

In the meantime, we are basing today’s trading budget on information gathered on Thursday, before the most recent lift in processor spot market quotes.

The combination of rain influence and the new-season spike in finished cattle prices driven by processor concerns over supply has had a considerable bearing on outcomes in Beef Central’s latest 100-day grainfed trading budget, based on steers entering a typical Downs feedlot now and closing-out after 105 days on April 23.

While reliable market signals are still a little sketchy at this early point in the year, with neither producers nor processors particularly active yet, some feeder cattle trading has been taking place on limited numbers. That means quotes published here on feeder rates are perhaps still a little speculative, but will become more robust by the time we publish our next breakeven, towards the end of January.

The trend will depend heavily on who gets rain, and how much.

For today’s budget, we’ve logged a feeder price for our designated flatback 450kg steer of 235c/kg. That’s based on bids late last week in the market of between 230c and an extreme of 250c.

That’s easily a record for this series, since our trading budgets started back in mid-2011, and is obviously driven by the recent encouraging rain events across large parts of Eastern Australia.

The feeder price is up 5c/kg on our late December budget, which itself jumped a dramatic 25c on early December, due to the arrival of rain.

Contributing to that rise, also, has been a general tightening in numbers of available feeders, leading into Christmas, pushing feedlots to offer some strong inducement to secure replacements as pens emptied-out out during the quiet three-week holiday trading period.

Today’s breakeven steer at 235c/kg values him at $1057 – again, easily a record buy-price for this report, and up another $22 on last time.

It’s only the second time in history that feeders have made ‘four digits.’ The low-point in feeder steer price in this report series came in May last year when it reached 150c/kg briefly ($675), meaning the purchase price has risen $382 a head since. That’s one of the big reasons for the big rise in COP seen in the graph.

Ration price stays at $375/t

The other factor is ration price, which we’ve let unchanged from our previous breakeven at $375/t.

That’s due to broader grain price trends, as well as continued solid feedlot demand for grain, as yards remained near full through December. Today’s figure is still a little below its recent peak of $385/t, recorded a few months ago.

Full pens means there is still not a lot of competitive pressure on custom feedlots in terms of margin on their ration price offer to customers, but that is likely to change some time in coming months, especially if there is further rain. Numbers on feed across Eastern Australia may now have peaked, and are likely to decline in the first quarter of 2015, if there is any further rain relief. Readers may recollect that the most recent September quarterly industry survey had feedlot numbers at a six-year high, at 908,000 head.

Should feedlot numbers now ease, due to the rain, it may stimulate a softening in feedgrain price, as demand subsides a little, market watchers have told Beef Central.

At the designated ration price of $375/t in today’s trading budget, it represents a total feeding cost over a typical 105-day program of $587. That, also, adds a lot of weight to the COP challenge captured in today’s graph.

Cost of gain, using our chosen variables (2kg/day ADG, for 210kg gain over 105 days) now sits at 284c/kg.

All that delivers a total production cost (steer price plus custom feeding price, freight, interest, contingency, levy and induction costs) of a breathtaking, record $1746, up another $23 on last time.

The inputs as described above deliver a breakeven in our latest budget of 495c/kg, a 7c/kg increase on late December’s calculation. Again, that’s easily a record high for Beef Central’s regular report.

The question for producers or owners of feeder cattle now is: do they consider placing 100-day cattle on feed with the prospect of facing a record production cost, or are they confident that forward slaughter price rates will continue to climb, in order to justify the feeding decision?

Just in the past week, alone, there has been up to three rises in forward contract prices for grainfed cattle on some grids.

Forward pricing for GF ox hits 480c

Based on our inquiries among SEQ grainfed processors on Thursday, we currently have forward pricing on 100-day ox for slaughter April, week three, at 480c/kg, with reports at levels above that, as well.

That price is another 10c/kg above our late December breakeven calculation, and 30c/kg higher than forward pricing seen as recently as mid-September. This time a year ago, the forward price for April delivery was 400c/kg.

So do processors have more in their pocket to spend on 100-day ox this year? Apparently so, based on today’s spot prices quoted at the top of this report. An A$ that has sailed below US81c in the past fortnight adds further firepower, and confidence to processor bidding. This time a year ago, the A$ was at, or above, US90c.

All that, as mentioned in our intro, delivers a trading budget outcome in today’s calculation of negative $53 per beast. While still well into red-ink territory, it is $12 better than our late December budget, and given the price quotes discussed above, is only likely to improve next time, provided feeders do not get too pricey.

Today’s spot market

Looking back at 100-day cattle that went on feed back in October, for slaughter this week, their forward sale position was around 430c/kg, compared with the spot market for 100-day ox on Thursday at around 460c. That means processors are in the money to the tune of 30c/kg, or $106 a head, on slaughter cattle killed today that they secured forward back in October, compared with buying on the current spot market. At the time, though, 430c would have looked reasonably attractive to most producers wanting to secure a price.

One of the factors driving the spot price and forward price currently is supply. Two large Downs feedlots spoken to yesterday already have significantly fewer numbers on their books, since recent rain. One site had dropped from full capacity (30,000 head) back below 25,000, and the other was also back close to 20pc in numbers on where it sat late last year. The sheer number of cattle on feed late last year was having its own dampening effect on price, but that influence now appears to have passed, with the rain impact.

Beef Central’s regular 100-day grainfed breakeven scenario is based on a standard set of representative production variables, ex Darling Downs. It is built on a feeder steer of 450kg liveweight, fed 105 days; 356kg dressed weight at slaughter; ADG of 2kg; consumption 15kg/day and a NFE ratio of 7.5:1 (as fed); $25 freight; typical implant program. Bank interest is included. It is important to note that variations exist across production models (feed conversion, daily gain, mortality, morbidity, carcase specification); from feedlot to feedlot; and between mobs of cattle. Equally, there can be considerable variation at any given time in ration costs charged by different custom-feed service feedlots. Click here to view an earlier article on this topic. For a more specific performance assessment on a given mob of cattle, consult with your preferred custom feeder.