For the Bahasa Indonesia version of this report click here (Untuk versi bahasa Indonesia dari laporan ini klik di sini)

Key Points

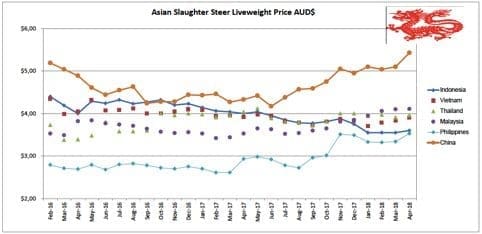

- Chinese domestic slaughter cattle prices are going ballistic.

- The Vietnamese business case for increasing imports at is looking bright.

- The Philippines slaughter cattle prices have finally caught up the rest of SE Asia.

Indonesia : Slaughter Steers AUD $3.60 / kg live weight (Rp 10,550 = $1AUD)

The small rise in the AUD price above is due to currency movements only.

The local Rp rate for slaughter steers is holding at around the 38,000 rate with some sales down to Rp37,000 and some still up to Rp41,000 or even more for exceptional stock.

The general market situation remains weak and if anything is weakening. While actual sale prices per kilo have not declined, it appears that the amount of credit being given to butchers is on the increase. Many feedlots still contain long-fed cattle of up to 180-200 days! These animals are a disaster for everyone although I am advised that reduced import numbers has allowed some feedlots to begin the unloading process.

Once Ramadan commences all feedlots will finally clear their backlogs and be ready to receive new imports.

The difficult question for the importer is, what real demand will there be following Ramadan and Lebaran?

The welcome news of falling feeder cattle prices in northern Australia is not the only factor to consider.

With Indian buffalo beef capturing in the order of 50 percent of the original fresh beef market, it is hard to imagine that importers will be able to justify the purchase of any more than 50 percent of pre-India import levels i.e. around 300,000 head for 2018.

Even if new feeder cattle are cheap, if the demand for the remaining fresh beef market is already fully saturated then lower prices are of no help.

The uncomfortable number of 180-200 day cattle as noted above are a reflection of this lack of demand as feedlots have recently been running at or below 70pc capacity and have still been unable to achieve orderly sale outflows which result in cattle leaving the feedlot after their target on-feed days of 120 – 140 days post-arrival. 70pc capacity is still too many cattle for the market to accept.

Another problem associated with holding cattle past their target sale date is that this obviously leaves a hole in the importers projected bank balance. As cattle are feed longer because a suitable sale can’t be found then they cost more, get fatter and lose even more value as a result of increased fat depth. So the discounting starts again and these very expensive, over fat cattle are finally dumped at a give-away price which may also need to include some credit terms to the butchers. More expenses but less returns so the deficit in the cash flow budget keeps getting bigger.

When the time comes to raise funds for the purchase of the next shipment, the bank can clearly see that sales performance and income is not up to projections so they become more concerned about additional lending. As the business risk profile increases so do interest rates on borrowed funds.

Then there is the ongoing mandatory 1 for 5 government heifer import guarantee signed by all current importers. In short, nobody is even close to meeting their required target for breeder heifer importations.

It is already the beginning of May so, in only 8 months, the government has advised that all importers who have not complied with their 1:5 obligations will have their import permits cancelled for a period of 12 months. As of today, that means that if the government maintains their current policy position there will be zero import permits issued for 2019.

In my opinion, the government appears to be way off track by attempting to force the feedlot industry to import breeding cattle.

Firstly, feedlot profitability has been crushed by the recent introduction of Indian buffalo beef, so importers don’t have the funds to make this additional and very expensive investment. Even if they did, feedlots are the least efficient system of managing breeding cattle. By contrast, palm oil plantations are the very logical place to efficiently manage very large numbers of breeding cattle. Indonesia has the world’s largest area of palm plantations at about 10 million hectares while Malaysia is number two with about 5 million hectares. In addition, palm oil producers are fortunate to have a very profitable industry which would allow them to invest in breeding cattle without endangering their commercial survival.

If the government wants to use their regulatory muscle to increase the national beef cattle herd then placing some cattle integration requirements on the vast and wealthy plantation industry would be far more logical and effective than focusing on the comparatively small and virtually insolvent feedlot industry.

Grazing breeders under palm oil trees, a perfect match. Logical, natural integration which is effective and low cost with potential for massive expansion.

The 32 license holders in the Indonesian feedlot industry represent an amazing range of participants from subsidiaries of corporate giants to foreign venture capitalists to family operations, stand-alone local companies and state owned enterprises. Not one is the same as any other with each having their own unique niche in the domestic beef production system. While the external commercial forces on each importer are similar, their capacity to deal with them are totally different so it is virtually impossible to make a general prediction on how the industry will react to this disturbing mix of serious threats to their survival. The only certainty is that the current situation is grim while the future looks even worse.

The Indonesian government breeder tenders are still in progress but some of them appear to have ran into difficulties. The latest advice is that the final tenders might be in the order of 6,000 head rather than the original plan for 15,000 but only time will tell.

Vietnam: Slaughter Steers AUD $3.91 / kg (VND17,400 to $1AUD)

Fortunately, the situation in Vietnam could not be more different to that described for Indonesia above. Slaughter cattle prices remain high and firm following last month’s small increase but now the importers have the long awaited opportunity to purchase Australian feeder and slaughter cattle at significantly reduced prices. Slaughter steers in Ho Chi Minh City are holding at VND68,000 per kg. Vietnam’s industry is based on simple supply and demand fundamentals with no negative government policy interference. As a result, much lower CIF prices simply mean that importers will be able to reduce their price to the market at the same time as improving the margins for their business. 90 million Vietnamese love their fresh beef so lower Australian prices should translate into increased imports, greater slaughter numbers and lower domestic retail rates. The timing of the reduction in CIF rates couldn’t be better as the approaching warm weather in Vietnam usually results in reduced demand for beef. Attractive rates might well help to offset this traditional dip in summer import rates. It is interesting to note that Vietnam is the largest importer of Indian buffalo beef in the world but this appears to have little impact on their demand and prices for fresh beef.

There has been a general changing of the guard in the Vietnamese feedlot sector with some of the largest players either disappearing or backing off while more nimble and efficient companies have been able to expand their market share. Total imports for 2017 were just under 170,000 with current estimates suggesting that the total for 2018 might be closer to 200,000. If northern Australian prices continue to collapse, Vietnam may well be able to take even greater numbers and break through the 200,000 mark by the end of the year. Current feedlot numbers are reported to be at around 50% capacity so there is plenty of space if the prices are right.

Thailand : Slaughter Steers AUD $3.96 / kg (Baht 24.0 to $1AUD)

Once again nothing significant to report from Thailand this month with live cattle prices the same as last month.

Bangkok supermarket, Aussie grassfed striploin AUD$52, 1824 strip $54, cube roll $64.58 (THB24 = AUD$1)

Malaysia : Slaughter Steers AUD $4.11 per / kg (RM2.99 to $1 AUD)

This apparent price rise is once again purely due to the ongoing strengthening of the Ringgit. My agent reports that there is so little local fresh beef in the supermarkets that they are unable to get a quote for the report. Live cattle imports and domestic slaughter for both Peninsular and East Malaysia are insignificant by comparison to the other markets followed in this report.

Last month I asked for comments regarding the discontinuation of Malaysian section of this blog. I did not get many responses but the vast majority were in favour of deleting this segment. Accordingly, the June report will be the last until further notice.

Philippines : Slaughter Cattle AUD $3.53 / kg (Peso 39.7 to AUD$1)

The contrast between Malaysia and the Philippines live cattle and fresh beef sectors is remarkable. While the Malaysian trade is declining to the point of no serious interest for this report, the conditions in the Philippine market are booming. Since the beginning of this report over 4 years ago, the price of slaughter cattle in the Philippines has been consistently the lowest of all reported countries, below AUD$3 per kg. In October 2017 the price finally broke through this barrier to $3.01 and has since shot up to the current level of $3.53. See the graph above. While some of this AUD price rise is due to currency changes, the main driver is the increase in the domestic Peso price of slaughter cattle as a result of an extended period of rapid and sustained economic growth. Seasons have been favourable, employment is rising, consumer sentiment is optimistic and the population is spending more on everything including beef.

During the late 1980’s, the Philippines was Australia’s largest single market for live cattle exports. If the rise of imports during the last 8 months continues then they may once again re-emerge as one of our significant S. E. Asian live cattle customers.

China : Slaughter Cattle AUD $5.43 / kg (RMB 4.83 = AUD$1)

Forget the rest, China is the market to watch in terms of potential for a massive increase in demand for live imports in the near future. This potential demand will impact the whole of the Australian industry not just the north as China can take both Bos Taurus and Bos indicus type cattle.

The Beijing report for this month provides a price range for slaughter steers of Yuan 26 to 27 while the Shanghai price is quoted as Y26, both increasing from last month. When I asked my agents if the consistent rises that have been reported for the last 10 months were a result of supply or demand factors, the reply was both.

China slaughtered 21 million cattle in 2016 dropping to a reported 20 million during 2017. The expectation for 2018 is a further reduction although not as much as for 2017. Chinese beef output is on the rise as a result of more efficient production from the domestic herd but the level of growth in this beef supply is far short of what is required to keep up with the rise in consumption. Current consumption figures are estimated to be around 6.0-6.5 kg per capita and increasing at a much faster rate than production making it impossible for domestic supplies to ever catch up and bridge the gap. Growing imports of fresh and frozen product are huge and important but the very specific and large domestic market segment of fresh beef can only be supplied by locally slaughtered cattle. As local supplies continue to fall further behind, live imports are the only solution for the additional fresh product demanded by the market. Australia is the only significant potential supplier for these additional live cattle imports.

The Beijing price for slaughter ox this month converts to AUD$5.48 per kg live weight. The price of quality slaughter bullocks in southern Australia was at or below AUD$3 per kg and falling at the end of April The cost of the live export process including sea freight from southern Australia to China is a ball-park $1.50 per kg -ish. Which, if my figures are near the mark, leaves a potential margin to split between the exporter and the importer of around $1 per kg for a 500kg bullock or $500 per head. This level of potential margin has not been seen in the live cattle trade for a very, very long time. Every month that the Chinese government retains its current unworkable health protocol will result in the continuation in the steady climb in the price of domestic slaughter cattle. The domestic deficit for live slaughter cattle is at least 1.5 million and climbing so the potential for big numbers of live imports is real. A change of heart by the Chinese regulators appears inevitable so it’s only the timing that is in doubt.

New York

My daughter Zealie lives in New York. If you are thinking that your beef is expensive, have a look at the prices at this NY butcher shop below. 1 pound of beef is equivalent to 0.454 kg so $36 per pound for a grass fed Rib Eye converts to USD$79.29 per kg. Exchange that to AUD at 76 cents to the USD and a kg of this steak will cost about AUD$104! But it is no doubt a top piece of beef and you are also provided with the name and location of the farm where it was produced.

The photo at the bottom is from an expensive boutique butcher shop in an inner Melbourne suburb. Almost exactly half the price of the same New York product and I expect every bit as good.

April 2018 price table

These figures are converted to AUD$ from their respective currencies which are changing every day so the actual prices here are corrupted slightly by constant foreign exchange fluctuations. The AUD$ figures presented below should be regarded as reliable trends rather than exact individual prices. Where possible the meat cut used for pricing in the wet and supermarket is Knuckle / Round.

| Location | Date | Wet Market

AUD$/kg |

Super market

$/kg |

Broiler chicken

$/kg |

Live Steer

Slaughter Wt AUD$/kg |

| Indonesia | Nov 17 | 12.82 | 19.61 | 3.30 | 3.88 |

| Rp10,400 | Dec 17 | 12.98 | 14.42 | 3.75 | 3.75 |

| Rp10,700 | Jan 18 | 12.62 | 14.30 | 3.27 | 3.55 |

| Rp10,700 | Feb 18 | 11.21 | 14.30 | 3.27 | 3.55 |

| Rp10,700 | March 18 | 11.21 | 14.21 | 3.18 | 3.55 |

| Rp10,550 | April 18 | 12.79 | No stock | 3.41 | 3.60 |

| Philippines | Nov 17 | 8.05 | 7.92 | 2.99 | 3.51 |

| P38.7 | Dec 17 | 8.01 | 7.88 | 3.75 | 3.49 |

| P40.5 | Jan 18 | 7.65 | 7.65 | 3.09 | 3.33 |

| P40.7 | Feb 18 | 7.86 | 7.62 | 3.37 | 3.32 |

| P40.4 | March 18 | 7.92 | 7.67 | 3.39 | 3.34 |

| P39.7 | April 18 | 8.31 | 8.06 | 3.45 | 3.53 |

| Thailand | Nov 17 | 9.60 | 11.20 | 2.80 | 4.00 |

| THB 25.0 | Dec 17 | 9.60 | 11.20 | 2.80 | 4.00 |

| THB 25.4 | Jan 18 | 9.49 | 11.02 | 2.76 | 3.94 |

| THB 24.7 | Feb 18 | 9.72 | 11.34 | 2.83 | 3.97 |

| THB 24.3 | March 18 | 9.88 | 11.52 | 2.88 | 3.91 |

| THB 24.0 | April 18 | 10.00 | 11.67 | 2.92 | 3.96 |

| Malaysia | Nov 17 | 10.15 7.30 | 11.75 | 2.29 | 3.81 |

| MYR 3.12 | Dec 17 | 11.21 5.77 | 11.52 | 2.34 | 3.85 |

| MYR 3.15 | Jan 18 | 11.11 5.71 | 11.42 | 2.22 | 3.95 |

| MYR 3.07 | Feb 18 | 11.40 5.86 | No product | 2.38 | 4.06 |

| MYR 3.00 | March 18 | 11.67 6.00 | No product | 2.40 | 4.10 |

| MYR 2.99 | April 18 | 11.70 6.02 | No product | 2.51 | 4.11 |

| Vietnam HCM | Nov 17 | 17.92 | 14.16 | 7.51 | 3.87 |

| D17,500 | Dec 17 | 14.29 | 14.00 | 7.42 | 3.83 |

| D18,100 | Jan 18 | 15.47 | 17.68 | 7.29 | 3.70 |

| D17,700 | Feb 18 | 15.82 | 18.08 | 7.46 | 3.79 |

| D17,700 | March 18 | 15.82 | 18.08 | 7.46 | 3.34 |

| D17,400 | April 18 | 16.09 | 17.82 | 7.59 | 3.91 |

| China Beijing | Nov 17 | 13.52 | 15.90 | 3.78 | 5.03 |

| Y5.05 | Dec 17 | 12.67 | 15.45 | 3.66 | 4.95 |

| Y5.10 | Jan 18 | 12.55 | 15.69 | 3.53 | 5.10 |

| Y4.96 | Feb 18 | 12.50 | 16.93 | 3.22 | 5.04 |

| Y4.90 | March 18 | 13.06 | 17.14 | 3.06 | 5.10 |

| Y4.83 | April 18 | 13.25 | – | 3.73 | 5.48 |

| Shanghai | Nov 17 | 16.70 | 19.48 | 4.97 | 4.77 |

| Dec 17 | 17.03 | 19.41 | 4.75 | 4.95 | |

| Average 5.43 | Jan 18 | 16.47 | 19.60 | 4.71 | 5.10 |

| Feb 18 | 16.93 | 20.97 | 4.84 | 5.24 | |

| March 18 | 16.32 | 21.22 | 4.49 | 5.10 | |

| April 18 | 16.15 | 21.95 | 4.55 | 5.38 |

To visit Dr Ross Ainsworth’s South East Report blog page click here