For the Bahasa Indonesia version of this report click here (Untuk versi bahasa Indonesia dari laporan ini klik di sini)

Key Points

- Indonesian Feedlot industry finally clears the backlog ready for a new beginning.

- The Philippines slaughter cattle prices have rejoined the SE Asian pack.

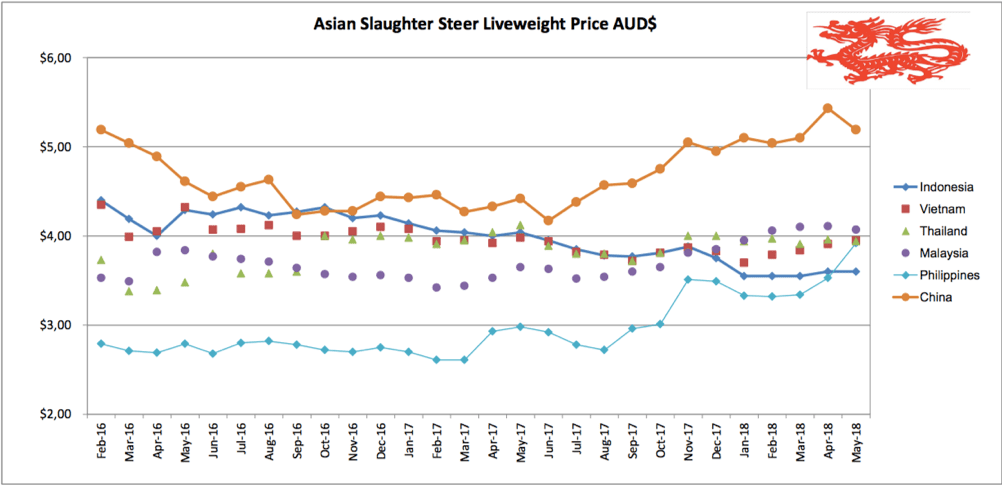

Indonesia: Slaughter Steers AUD $3.60 / kg live weight (Rp 10,550 = $1AUD)

Prices were unusually stable this month including the first two weeks of Ramadan (14th – 31st May) with bottom rates steady at Rp37.5k (at the beginning of the month) and top rates holding at around Rp40,000 or less. The significant feature for this month is that all feedlots have finally got their stock numbers down to a point where there are no more long-fed, over-fat cattle left in the system while some importers are even having to ration their sales to ensure that they don’t run out before their new stocks reach slaughter weight. This is the first time stocks have been in under-supply territory since the introduction of Indian buffalo beef in late 2016.

In AUD terms, today’s CIF price for feeder cattle delivered Jakarta is about $3.65. This time last year the CIF rate was $4.05-4.10 while two years ago it was closer to $4.60! When this new under-supply situation is combined with the attractive new CIF price, importers should be in a position to end all discounting and allow the price to firm up to the previous non-stressed levels of around Rp40-43,000 per kg live weight for slaughter cattle. For most of the history of this trade, importers have had to buy feeders at a price per kg that is higher than their per kg selling price i.e. with an initial trading loss (with the net profit all coming from the feeding margin). In the event that the recent discounting disappears then the new pricing levels of around Rp40,000 per kg may provide a very welcome combination of both a small but positive trading margin as well as a feeding margin which should mean that all efficiently managed feedlots will soon be able to return to profitability. The main danger is that some importers will become over optimistic and bring in too many feeders which will eventually lead to another over-supply situation followed by a return to the inevitable discounting cycle. Finding this new industry equilibrium point will be tricky but at least importers now know how many cattle in the feedlot is too many, i.e. all 2017 levels, as well as today’s number which is very close to not enough. Recently published MLA figures for the calendar year to the end of April show feeder imports to Indonesia for the first 4 months at 147,000 head. These imported feeders are the ones now being traded into today’s Ramadan market. An extrapolation of this number to an annual figure would suggest a 12 month import level of 441,000. This is potentially misleading because Ramadan is the annual peak in demand so this figure should perhaps be seen as an annual maximum number rather than a minimum. The same MLA report shows the total feeder imports for 2017 were 513,000. This number was clearly shown to be far too many while the new level to April seems to be much closer to the right commercial balance of supply and demand. Last month I made a guess that the new sustainable feeder import level might be at about 300,000 head based on a factor of 50% of the pre-Indian beef number of 600,000. I think that the new estimate above of about 440,000 feeders is based on much more reliable information.

It is interesting to note that the current price of feeders delivered Darwin is around AUD$2.65 per kg live weight while the CIF price Jakarta for that same feeder is about AUD$3.65 (exchange rate @Rp10,500 per AUD$1). So as a rough rule of thumb, the CIF price in Indonesia can be estimated by simply adding $1 per kg to the price of feeders delivered to Darwin.

I have been travelling around Indonesia recently and visiting wet markets wherever possible. One consistent finding is that beef prices are remarkably similar across all Indonesian wet markets. See below photos of wet markets in Lombok and Bengkulu (West Sumatera). Despite the great distance between the two and the major differences in their live cattle supplies, the prices of fresh beef in both markets are very similar. I have also found this to be the case in Java, North Sumatera and Kalimantan. In the two locations below, knuckle costs between Rp125,000 and Rp130,000. In Bengkulu the source of cattle is Australian imports trucked in from the feedlots in Lampung while the cattle in Lombok are mainly locally bred Bali cattle. The indicator price in Jakarta this month was Rp135,000.

There are a large number of beef tables like this one in the main wet market in Mataram, the capital of Lombok.

Pak Hari has the cleanest and best presented wet market beef table in Pasar Minggu, the largest wet market in Bengkulu, West Sumatera.

Ayam Kampung (village chicken) in the Lombok wet market. These small and very tasty birds sell for triple the rate of industrial broilers with each bird selling for Rp35,000 at a weight of about 330 grams so effectively Rp105,000 per kg while broilers sell for about Rp38,000 per kg. The bird-on-a-stick presentation is ready for the BBQ.

Vietnam: Slaughter Steers AUD $3.95 / kg (VND17,200 to $1AUD)

Prices remain similar to last month with the main indicator slaughter steer rate in HCM City holding at Dong68,000 per kg. Bulls range from 71-73,000 Dong while heifers are stable at 65,000Dong. As usual, prices in the north are all about 1,000 higher for each category. The only slight change from last month is the report on the stock on hand. Total feedlot capacity is estimated at about 100,000 head. Last month the numbers on feed were estimated to be around 50% of capacity while this month the estimate is 60% which I expect is a direct result of the lower prices out of northern Australia. Given that prices in northern Australia are unlikely to rise until the end of the year at the earliest, this on-feed percentage may well continue to rise in the coming months.

China: Slaughter Cattle AUD $5.19 / kg (RMB 4.82 = AUD$1)

Prices for slaughter cattle have eased very slightly in both Beijing and Shanghai with the rate in both locations reducing from 26Yuan in April to Y25 per kg in May. This small fluctuation still leaves China as the dominant market in Asia by a wide margin. It also continues to put them in the spotlight as Australia’s most likely new mega-market for live cattle in the not too distant future. While this prospect is a pleasant one from a general economic perspective, I can’t help thinking of the politicians who will inevitably use this trade as a leverage tool if and when it expands to its full potential. Imagine the scenario in say three years time, the live cattle trade from Australia to China is booming with 700,000 slaughter cattle per year being exported. The Australian market is on a high, cattle are moving through all states and territories to coastal quarantine depots and being loaded onto ships in vast numbers. Four or five full shipments are on the water heading for China at any given time. China takes some action such as suddenly introducing shipping restrictions in the South China Sea and Australia (following the USA and others) protests strongly. In retaliation, China stops the live cattle trade overnight, putting the Australian government in a very difficult position of balancing diplomacy and trade. I don’t wish to be a pessimist but this style of diplomacy is already playing out on a daily basis, it just doesn’t involve large numbers of live animals mid-ocean, yet.

Discounted locally slaughtered beef shank @ Y54/kg (AUD$11.20) in a Beijing supermarket.

Philippines: Slaughter Cattle AUD $3.92 / kg (Peso 39.5 to AUD$1)

The Philippines is the star of the show at the moment with a relentless increase in slaughter cattle price rises finally bringing it into parity with the rest of the region. These rises have also led to a predictable increase in rates for fresh beef in the wet and supermarkets. And all this has developed over a very short, 6 month period. This new local live cattle price level combined with a reduced feeder price in northern Australia must surely put this market squarely back into the sights of the Australian exporters who are keen to find any new market opportunities given the ongoing decline in the Indonesian import numbers.

Thailand: Slaughter Steers AUD $3.94 / kg (Baht 24.1 to $1AUD)

Once again nothing significant to report from Thailand this month with live cattle and beef prices unchanged from last month. See below some photos providing a comparison of a range Australian imported beef with local product.

Australian Wagyu BHT3,000 (AUD$124/kg), Aust grain fed BHT2,000 ($83/kg), Aust grass fed BHT1,250 ($52) and local beef BHT1,180 ($49).

Malaysia : Slaughter Steers AUD $4.07 per / kg (RM3.00 to $1 AUD)

Local slaughter prices are down a little while the Ringgit has strengthened. Domestic fresh beef prices have risen slightly in line with the festival of Ramadan during the last two weeks of May.

May 2018 price table

These figures are converted to AUD$ from their respective currencies which are changing every day so the actual prices here are corrupted slightly by constant foreign exchange fluctuations. The AUD$ figures presented below should be regarded as reliable trends rather than exact individual prices. Where possible the meat cut used for pricing in the wet and supermarket is Knuckle / Round.

These figures are converted to AUD$ from their respective currencies which are changing every day so the actual prices here are corrupted slightly by constant foreign exchange fluctuations. The AUD$ figures presented below should be regarded as reliable trends rather than exact individual prices. Where possible the meat cut used for pricing in the wet and supermarket is Knuckle / Round.

| Location | Date | Wet Market

AUD$/kg |

Super market

$/kg |

Broiler chicken

$/kg |

Live Steer

Slaughter Wt AUD$/kg |

| Indonesia | Dec 17 | 12.98 | 14.42 | 3.75 | 3.75 |

| Rp10,700 | Jan 18 | 12.62 | 14.30 | 3.27 | 3.55 |

| Rp10,700 | Feb 18 | 11.21 | 14.30 | 3.27 | 3.55 |

| Rp10,700 | March 18 | 11.21 | 14.21 | 3.18 | 3.55 |

| Rp10,550 | April 18 | 12.79 | No stock | 3.41 | 3.60 |

| Rp10,550 | May 18 | 12.80 | 10.80 – disc | 3.32 | 3.60 |

| Philippines | Dec 17 | 8.01 | 7.88 | 3.75 | 3.49 |

| P40.5 | Jan 18 | 7.65 | 7.65 | 3.09 | 3.33 |

| P40.7 | Feb 18 | 7.86 | 7.62 | 3.37 | 3.32 |

| P40.4 | March 18 | 7.92 | 7.67 | 3.39 | 3.34 |

| P39.7 | April 18 | 8.31 | 8.06 | 3.45 | 3.53 |

| P39.5 | May 18 | 8.35 | 8.86 | 3.54 | 3.92 |

| Thailand | Dec 17 | 9.60 | 11.20 | 2.80 | 4.00 |

| THB 25.4 | Jan 18 | 9.49 | 11.02 | 2.76 | 3.94 |

| THB 24.7 | Feb 18 | 9.72 | 11.34 | 2.83 | 3.97 |

| THB 24.3 | March 18 | 9.88 | 11.52 | 2.88 | 3.91 |

| THB 24.0 | April 18 | 10.00 | 11.67 | 2.92 | 3.96 |

| THB 24.1 | May 18 | 9.96 | 11.62 | 2.90 | 3.94 |

| Malaysia | Dec 17 | 11.21 5.77 | 11.52 | 2.34 | 3.85 |

| MYR 3.15 | Jan 18 | 11.11 5.71 | 11.42 | 2.22 | 3.95 |

| MYR 3.07 | Feb 18 | 11.40 5.86 | No product | 2.38 | 4.06 |

| MYR 3.00 | March 18 | 11.67 6.00 | No product | 2.40 | 4.10 |

| MYR 2.99 | April 18 | 11.70 6.02 | No product | 2.51 | 4.11 |

| MYR 3.00 | May 18 | 11.66 6.00 | No product | 2.40 | 4.07 |

| Vietnam HCM | Dec 17 | 14.29 | 14.00 | 7.42 | 3.83 |

| D18,100 | Jan 18 | 15.47 | 17.68 | 7.29 | 3.70 |

| D17,700 | Feb 18 | 15.82 | 18.08 | 7.46 | 3.79 |

| D17,700 | March 18 | 15.82 | 18.08 | 7.46 | 3.34 |

| D17,400 | April 18 | 16.09 | 17.82 | 7.59 | 3.91 |

| D17,200 | May 18 | 16.28 | 18.02 | 7.67 | 3.95 |

| China Beijing | Dec 17 | 12.67 | 15.45 | 3.66 | 4.95 |

| Y5.10 | Jan 18 | 12.55 | 15.69 | 3.53 | 5.10 |

| Y4.96 | Feb 18 | 12.50 | 16.93 | 3.22 | 5.04 |

| Y4.90 | March 18 | 13.06 | 17.14 | 3.06 | 5.10 |

| Y4.83 | April 18 | 13.25 | – | 3.73 | 5.48 |

| May 18 | 12.45 | – | 3.32 | 5.19 | |

| Shanghai | Dec 17 | 17.03 | 19.41 | 4.75 | 4.95 |

| Jan 18 | 16.47 | 19.60 | 4.71 | 5.10 | |

| Feb 18 | 16.93 | 20.97 | 4.84 | 5.24 | |

| March 18 | 16.32 | 21.22 | 4.49 | 5.10 | |

| April 18 | 16.15 | 21.95 | 4.55 | 5.38 | |

| May 18 | 16.60 | 22.41 | 4.56 | 5.19 |

To visit Dr Ross Ainsworth’s South East Report blog page click here