Comment : While prices have been steady for live slaughter cattle in all of the SE Asian markets during September, all the relevant exchange rates have moved significantly. As the prices noted in this report are in AUD this gives the false impression that live cattle prices have changed.

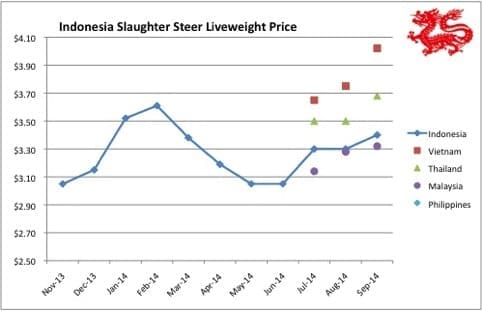

Indonesia: Slaughter steers AUD $3.40/kg liveweight

The remarkable thing about the Indonesian market this month is that while there have been so many factors pushing the market in different directions, the end result is that the price in local currency remains steady.

The increase in the AUD price from $3.30 last month to $3.40 now is entirely a result of the weakening of the AUD against the Rupiah.

For all of our live cattle markets, the important currency issue to watch is the local cross rate rather than the AUD/US$ relationship.

Importers are paid for their cattle in local currency and exporters have to pay Australian producers in AUD so the relationship between the local currency and the AUD is the one to watch.

Some of the factors driving the market this month were :

- With the Muslim festival of Korban due on the 5th October, many locals are saving their cash for the sacrifice expenditures so demand in the wet markets was significantly weaker.

- Local male cattle have been withdrawn from the market for the last few months and reserved for delivery at the Korban festival pushing local cattle prices to very high levels.

- Cattle for Korban are sent to Java from all over Indonesia. See photo below taken earlier in September of Bali cattle in a saleyard just outside Denpasar. Saleyard price was Rp39,000 per kg live with about rp2,000 Rp per kg to deliver to Java.

Photo from David Heath : Bringkit cattle market just outside Denpasar, Bali.

- Some local state-owned lot feeders are offering prices at the lowest end of the market range restricting the capacity of other importers to push prices upwards.

- A few months ago, East Java, the home of breeding cattle in Indonesia, opened up its market to live cattle imports by allocating permits to two importers to send 500 head consignments of Australian cattle from West to East Java.

This was seen as strong evidence of the savage reduction of the national breeder herd.

A few weeks ago, the East Java government intervened once again to stop any further imports from entering the province. It looks like politics is winning again over the natural forces of supply and demand.

The import number guessing game is on again with official Q4 allocations of 246,000 head. Actuals for Q1 were 134,000 and Q2 212,000 head.

Q3 is not over yet but an educated guess from a local source at this one is around 120,000 producing a Q3 year to date total of about 470,000. The importers can request and the government can allocate 246,000 permits all day long but there are some other factors at play that are likely to reduce this figure substantially.

‘My advice is the total number that can be shipped in Q4 is 180,000 head’

My advice is that the total shipping capacity allocated for Indonesia in Q4 is about 60,000 head per month or a maximum total number that can be shipped in Q4 of 180,000 head (a substantial amount of shipping space is already booked for China and elsewhere in Q4).

That’s assuming everything works perfectly with no loading or discharge delays.

More importantly, sources in the north of Australia predict that there are only about 100,000 head available for shipment in Q4.

And, prices in Australia have shot up and will probably continue to do so for the next six months at least.

Some importers will almost certainly baulk at the new higher rates and purchase less than their allocations.

When all this is put together, the total cattle imported for 2014 is probably going to be pretty close to 600,000 head.

This restriction in the capacity to supply Indonesian customers and the oncoming monsoon season in Australia is likely to be the trigger for rising prices and shrinking supplies.

It all depends on the northern Australian wet season.

The present period of steady prices in Asia could well be the calm before the storm.

A good wet season could see Australian prices go as high as $3 per kg next season creating shock waves throughout our live export markets across Asia.

The outgoing government has once again made moves to allow beef imports from Brazil and India by accepting the proposition of Regional Certification for FMD freedom.

This initiative is likely to be reviewed by the new administration when it is finally in place next month.

The only “whispers” regarding the possible policy direction of the new government are that they will refocus on self -sufficiency although with a more pragmatic approach than the present policy makers.

Korban (Qurban) Sales Poster

This poster in my local shopping mall is advertising the cattle, sheep and goats available for sale for the Korban festival. It lists the weight ranges, prices and even gives the bank account details at the bottom for electronic funds transfer.

If we use the middle of the weight range then a 275 kg bull (Sapi) from Java (Pulau Jawa) costing Rp15,555,000 = AUD$1,453 or $5.28 per kg. The cheaper bull alternative is sourced from outside Java. A sheep (domba) or goat (kambing) with an average weight of 32.5 kg costs Rp2.255,000 = AUD$210 or $6.48 per kg.

Vietnam: Slaughter steers AUD $4.02/ kg

The beef and live cattle market was static during September with only currency issues influencing the AUD price.

With the strong economy and beef prices, entrepreneurs continue to be encouraged to plan more cattle projects in Vietnam.

Some new feedlots are under construction while others are in the planning phase. Official statistics from the government census note that in 2007 the national cattle herd was 6.6 million head.

The figure quoted by government sources for 2013 is 4.97 million.

The same census states that dairy cow numbers have increased by about 15pc to around 200,000 head.

The big movement this month was in the chicken price which has increased by 30pc. This is due to the closure of the Chinese cross-border chicken trade as a result of Avian Influenza concerns in southern China.

This is a reminder of how lucky we are in Australia.

It is virtually impossible to restrict transmission of diseases such as Foot and Mouth Disease and bird flu across extremely long and porous land borders.

The irony is that when the borders are officially closed, the price differential across the border increases dramatically and the profit margins from smuggling stock from the infected side to the free side become much more attractive.

The result is that during disease outbreaks smuggling efforts are substantially increased.

Hanoi is famous for its beef and noodle dishes. While the amount of beef in each dish is small, with the city population of 6.5 million keen soup eaters, the overall consumption volumes are huge.

Beef noodle soup “Pho”

Beef and dried noodle

Dried beef and salad

Thailand: Slaughter steers AUD $3.68/kg

No change in live cattle prices with fat steers for local consumption and northern exports selling for the same prices, in local currency, as last month.

The only local report of note is a petition signed by a large number of cattle producers to lobby the government to restrict the supplies of imported frozen Indian beef.

Can’t blame them for wanting to keep out such cheap competition. My Thai sources tell me that the feeder health protocol is very close to agreement.

Malaysia: Slaughter steers AUD $3.32/kg

Little change in Malaysia except for reduced buying as many beef customers save their money for Korban.

This market in Malaysia is primarily supplied by live imports from Thailand (which probably originated in Myanmar).

These are small bulls led by nose ropes with an average live weight of around 250–350 kg. The selling price is up to 15 Ringgit per kg or AUD$5.24 per kg.

Some of the smarter beef cattle operations in Malaysia save their entire annual production of male cattle for this single day every year and make a “killing” as it is the one area where imported Australian cattle can’t compete.

Philippines: Slaughter cattle AUD $1.98/kg (mainly cull cows & bulls)

Cattle prices steady but pork prices have decreased sharply creating strong competition for beef.

The reason is the main rice and corn harvesting season in the southern Philippines has just finished with a bumper harvest resulting in reduced prices of both corn and rice.

Everyone but the farmers are happy because retail rice prices have finally dropped while low corn prices have led to a reduction in the cost of pork production which has been passed on to the consumer.

Brazil: Slaughter steers AUD $2.02/kg

We often hear how Brazil is the world’s largest beef exporter and how its beef is so cheap that it is a serious competitive threat to the Australian industry.

I contacted a friend in Brazil last week and he sent me the latest livestock sales figures.

Slaughter steers in Sao Paulo state were selling for US$1.81per kg live weight which translates to AUD $2.08 using today’s exchange rate of 87 cents.

The Sao Paulo retail price of hindquarter beef ranges from US$11 to US$18 per kg. Brazil is too far from Asia to ever present a threat to any of our live export markets in that region.

The sea freight cost alone for the 20 day trip from Brazil to Indonesia will cost more than the cost of the animal and the sea freight from Australia.

The news that China is expected to allow the re-entry of Brazilian beef imports after the 2012 closure caused by a suspected case of BSE should have minimal impact as Brazilian beef has continued to enter China since the ban by simply going through the grey route back door in Hong Kong.

Market price table

These figures are converted to AUD$ from their respective currencies which are changing every day so the actual prices here are corrupted slightly by constant foreign exchange fluctuations.

The AUD$ figures presented below should be regarded as reliable trends rather than exact individual prices. Where possible the meat cut used for pricing in the wet and supermarket is Knuckle/Round.

| Location | Date | Wet MarketAUD$/kg | Super market$/kg | Broiler chicken$/kg | Live SteerSlaughter WtAUD$/kg |

| Jakarta | Nov 13 | 8.80 | 10.46 | 3.24 | 2.92 * |

| Dec 13 | 9.26 | 9.16 | 1.85 | 3.15-3.43 | |

| Jan 14 | 9.63 | 9.75 | 2.04 | 3.52 | |

| Feb 14 | 9.26 | 9.63 | 2.77 | 3.61 | |

| Mar 14 | 8.80 | 9.72 | 2.64 | 3.33 | |

| April 14 | 8.52 | 5.93-8.52 | 2.77 | 3.06 | |

| May 14 | 8.52 | 8.80 | 2.77 | 2.96 | |

| June 14 | 8.52 | 8.80 | 2.77 | 2.96 | |

| July 14 | 11.00 | 12.38 | 3.00 | 3.30 | |

| August 14 | 10.09 | 10.36 | 3.02 | 3.30 | |

| Sept 14 | 10.28 | 10.36 | 3.08 | 3.36 | |

| Medan | Nov 13 | 8.33 | 8.24 | 3.43 | 3.15 |

| Dec 13 | 8.33 | 8.61 | 1.85 | 3.07 | |

| Jan 14 | 8.80 | 8.33 | 2.20 | 3.66 | |

| Feb 14 | 8.80 | 8.33 | 1.85 | 3.66 | |

| Mar 14 | 8.80 | 7.87 | 1.66 | 3.47 | |

| April 14 | 7.60 | 7.22-8.33 | 1.76 | 3.33 | |

| May 14 | 7.50 | 8.80 | 1.76 | 3.29 | |

| June 14 | 7.40 | 8.80 | 1.76 | 3.29 | |

| July 14 | 10.09 | 11.00 | 1.92 | 3.39 | |

| August 14 | 8.44 | 8.44 | 1.92 | 3.45 | |

| Sept 14 | 8.69 | 9.11 | 1.63 | 3.50 | |

| Philippines | Feb 14 | 4.90 | 5.09 | 2.74 | 1.91 |

| Mar 14 | 4.90 | 5.26 | 2.74 | 1.96 | |

| April 14 | 5.14 | 5.39 | 2.69 | 1.96 | |

| May 14 | 5.07 | 5.29 | 2.64 | 1.96 | |

| June 14 | 4.90 | 5.14 | 2.81 | 1.91 | |

| July 14 | 4.90 | 5.09 | 2.79 | 1.91 | |

| August 14 | 4.90 | 5.12 | 2.79 | 1.91 | |

| Sept 14 | 5.08 | 5.18 | 3.05 | 1.98 | |

| Thailand | Feb 14 | 8.33 | 7.33 | 2.33 | 3.33 |

| Mar 14 | 8.33 | 7.33 | 2.33 | 3.33 | |

| April 14 | 9.33 | 7.50 | 2.33 | 3.33 | |

| May 14 | 9.33 | 7.33 | 2.33 | 3.50 | |

| June 14 | 9.33 | 7.33 | 2.33 | 3.50 | |

| July 14 | 9.33 | 7.33 | 2.33 | 3.50 | |

| August 14 | 9.50 | 7.33 | 2.33 | 3.50 | |

| Sept 14 | 8.07 | 9.82 | 2.45 | 3.68 | |

| Vietnam | |||||

| Hanoi | July 14 | 12.50 | 15.45 | 2.75 | 3.65 |

| Ho Chi Minh | July 14 | 12.00 | 13.00 | ||

| H | August 14 | 12.62 | 15.45 | 3.75 | |

| HCM | August 14 | 12.00 | 12.62 | ||

| H | Sept 14 | 13.41 | 16.58 | 6.97 | 4.02 |

| HCM | Sept 14 | 11.80 | 13.95 | 6.97 | 4.02 |

| Malaysia | July 14 | 8.69 | 8.69 | 2.07 | 3.14 |

| August 14 | 9.50 | 9.50 | 2.07 | 3.25 | |

| Sept 14 | 9.79 | 2.27 | 3.32 |

- To visit Dr Ross Ainsworth’s South East Asia blog click here