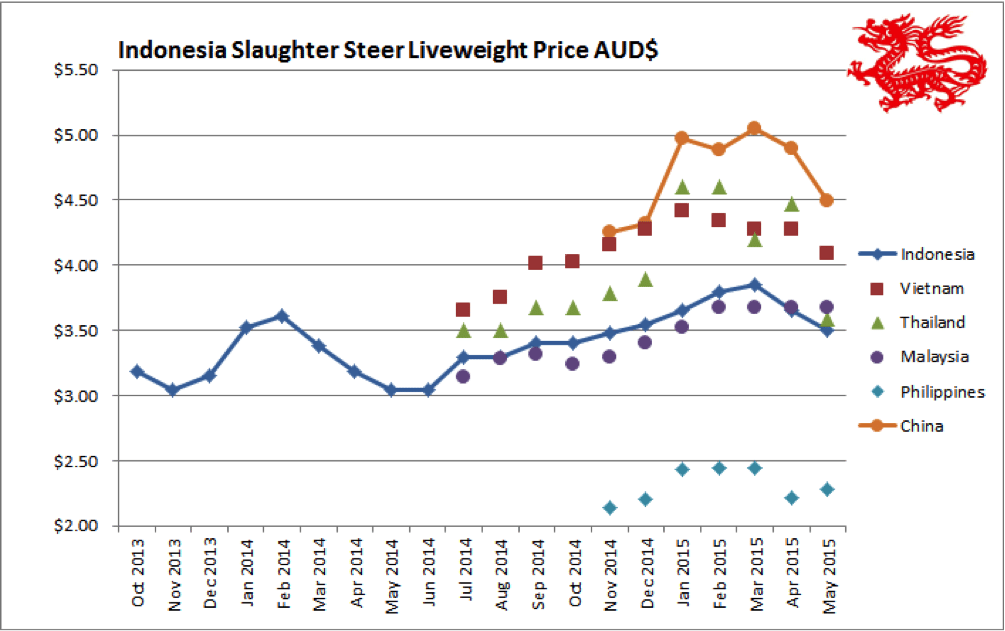

Indonesia: Slaughter Steers A$3.50/kg live weight (Rp10,300 = $1AUD)

FEEDER imports continued at a furious pace throughout May, racing to get as many of the 250,000 head permitted for Q2 in before the end of June.

The only significant change from last month is that over-filled feedlots are beginning to drop their slaughter prices further.

Figures of as low as Rp35,500 per kg for fat cattle have been offered in West Java but generally the price sits at around Rp36,000.

In north Sumatera, the market is also weakening but in this case it appears that the reason is declining buyer demand due to restrictions in incomes.

With dramatic reductions in the prices of rubber and palm oil – the two big commodity earners for Sumatera, wages are also being squeezed and beef purchases are being reduced as a direct result.

It’s also “back to school” time in Sumatera so spending tends to be directed to school needs and away from luxuries like fresh beef.

The live price in the north is around Rp38,000 for heavy steers while the exchange rate for the month has been more like Rp10,300 to the AUD.

I will use 36,000 as the monthly price producing an AUD indicator price for May of $3.50. Supermarket prices seem to be levelling out as buyer demand comes off to match the reduction in supplies of secondary cuts.

The Indonesian Department of Agriculture has a new Director General of Livestock Services. The holder of this position is arguably the most influential person in respect to policies for the live cattle trade after the Minister so it will be a very interesting few months as industry meets with the new incumbent and discovers his personal policy focus.

Vietnam: Slaughter Steers AUD $4.09 / kg (VND17,000 to $1AUD)

The crunch has come in Vietnam as the massive HAGL group and other feedlotters begin the serious fight for market share in both the northern and southern markets.

Prices as low as VND68,000 per kg have been offered to butchers for fat cattle in the south although the major sales have been in the 69 -70,000 range.

Prices in the north have declined to around VND71,000. Cross rates for the month have averaged about 17,000 VND to AUD$1.

For this month I will use an “average” southern price of 69,500 for the indicator figure which converts to AUD$4.09.

Imports continue at a fast pace despite the strong shipping activity into Indonesia.

Exporters continue their push for maximum ESCAS compliance with installation of CCTV for all supply chains well under way.

Wellard’s has gone a step further with the introduction of a new feature where the GPS location can be re-confirmed each time an RFID tag is read and transmitted (using a linked smart-phone) at the knocking box.

The double check is facilitated using the appropriate CCTV vision which allows the transmission time of the RFID read to be checked against the time of the actual slaughter and read process as viewed on the video recording for the specific animal in question.

This type of advancement in the control and traceability of supply chains demonstrates the commitment of exporters to the welfare of their livestock and the future of the trade.

Thailand: Slaughter Steers AUD $3.59 / kg (Baht 26.5 to $1AUD)

Two entirely unrelated political disputes in different locations have caused major disruptions to the Thai slaughter and feeder cattle trade.

- The China/Burmese cross border shootem-up involving the ethnic Kachin in the north west of Myanmar has resulted in the retaliatory closure of the importation of fat cattle from north-eastern Myanmar into China. These cattle arrived in Myanmar after a 2 day boat journey up the Mekong from northern Thailand. This slaughter cattle (and buffalo) export trade from northern Thailand has been the most lucrative option for Thai producers for several years with about 3,000 head per week being exported up river.

Thai cattle loading onto Lao riverboats for export to Myanmar then China. July 2014.

A local political dispute on the Thai side of the border has led to the closure of the Mae Sot cattle and buffalo crossing which is the main source of livestock from Myanmar. These animals once cleared from quarantine in Thailand are dispatched to feedlots in Thailand or sent onwards for slaughter or further fattening to Vietnam via Cambodia and Laos. After fattening in Thailand, slaughter stock are either killed for local consumption or exported to China via the Mekong.

Border crossing from Myanmar to Thailand near Mae Sot: Closed for business for now.

While the market forces resulting from each of these factors is pushing the supply and demand needle in opposite directions, the halting of the export trade to China has had the most powerful affect resulting in the live cattle slaughter price in Thailand falling from about 105-110 Baht per kg last month to around 95 Bht in the first week of June.

It will be very interesting to follow the affects of these two closures as their impact will have wide spread consequences.

Firstly the Yunnan province in south western China with suffer a severe shortage of live cattle as a result of the closure of the Mekong live cattle traffic. These cattle will then be redirected to alternative markets including Vietnam and south-eastern China via Cambodia and Laos respectively. These redirected cattle could effectively replace the flow from the closure of Mae Sot in the short term but many of these cattle originally came into Thailand via Mae Sot so sooner or later if both closures remain in place there must be a severe shortage of feeders, slaughter cattle and buffalo in Thailand and the surrounding region.

Australian live cattle prices are also likely to be affected positively if the ban from Myanmar stays in place for an extended period.

Another piece of interesting information to come out of Thailand this week was the official national slaughter figures for 2014/2015 which were reported to be close to 1 million head with a similar figure presented for the last 2 years.

As this figure is much easier to be accurately recorded compared to the national breeder herd population numbers this provides some solid clues as to the size of the Thai herd. Assuming that the amount of cattle coming in from Myanmar are similar to those being sent to China and Vietnam, therefore neutral, then a kill of 1 million would mean that the domestic herd must include about two million breeding cows to produce that number to kill and replace itself. So 4-5 million would seem a reasonable guess as a national cattle (and buffalo) herd total.

Malaysia: Slaughter Steers AUD $3.68 per/kg (RM2.85 to $1 AUD)

Once again, little change in the Malaysian market.

Exchange rate used RM 2.85 = AUD$1

Philippines: Slaughter Cattle AUD $2.28/kg (mainly cull cows & bulls)

Steady as she goes for the Philippines with minimal changes. Seasonal conditions having limited impact at the moment.

For this month I have used the exchange rate of AUD$1 to Peso 35.0

China: Slaughter Cattle AUD $4.49/kg (RMB 4.90 = AUD$1)

The price in Shanghai has taken a sharp downwards turn compared to the last few months plummeting 16% in a single month. The Beijing slaughter price has also dropped from 24 to 22 RMB per kg live weight. No idea why. I will continue to use the Beijing figure as the indicator price.

The dairy industry is on the path of growth again after the extended period of decline following the 2008 melamine poisoning scandal.

As the China diary herd grows in total numbers and production volumes, the number of small operators is shrinking fast as government tax incentives have encouraged larger corporate enterprises to expand and small farmers to sell out.

This is perhaps the reason for the very low price in Shanghai where slaughter is largely cull dairy cows. While the general trend is for China to produce a larger proportion of its domestic dairy products, this comes at a high price for certain inputs. For example in 2007, China imported just over 2,000 tonnes of alfalfa hay for its dairy cows (mostly from the USA). In 2014 China imported 900,000 tonnes of alfalfa hay!

Unfortunately I don’t have an agent in Kunming, the capital of the southwestern province of Yunnan. It would be fascinating to follow the prices of live cattle and beef in that city following the closure of 3,000 head per week of live imports from Myanmar via the Mekong in northern Thailand.

Uruguay

This is the only country in South America with Foot and Mouth Disease freedom for the whole country. As a result, its small but useful cattle herd of 13.5 million head is able to sell live cattle and beef into the same markets as Australia and NZ.

During 2014 it exported a total of 171,000 tonnes of beef with China taking 29%, 24% to NAFTA (Canada, USA and Mexico) and 23% to the EU.

With a small herd, modest export volumes and a location that makes live shipments extremely expensive, they do not represent a significant threat to Australian producers and exporters. With a latitude similar to New South Wales, the majority of its cattle are temperate breeds.

Dr Ross Ainsworth’s monthly South East Asian reports are first published exclusively on Beef Central. To view more of Dr Ross Ainsworth’s previous Beef Central articles click here. To visit his personal South East Asia report blog site, click here.

Market price table for May 2015

(All prices converted to AUD)

These figures are converted to AUD$ from their respective currencies which are changing every day so the actual prices here are corrupted slightly by constant foreign exchange fluctuations. The AUD$ figures presented below should be regarded as reliable trends rather than exact individual prices. Where possible the meat cut used for pricing in the wet and supermarket is Knuckle/Round

| Location | Date | Wet MarketAUD$/kg | Super market$/kg | Broiler chicken$/kg | Live SteerSlaughter WtAUD$/kg |

| Jakarta | Jan 2015 | 11.00 | NA | 3.50 | 3.60 |

| Feb 2015 | 11.00 | 12.75 | 3.30 | 3.70 | |

| March 2015 | 10.50 | 12.00 | 3.00 | 3.85 | |

| April 2015 | 11.00 | 15.00 | 3.60 | 3.65 | |

| May 2015 | 10.68 | 12.33 | 2.52 | 3.50 | |

| Medan | Jan 2015 | 3.75 | |||

| Feb 2015 | 11.75 | 11.75 | 1.70 | 3.95 | |

| March 2015 | 10.00 | 12.00 | 1.40 | 3.90 | |

| April 2015 | 9.70 | 11.50 | 1.70 | 4.00 | |

| May 2015 | 9.32 | 9.90 | 2.14 | 3.69 | |

| Philippines | Jan 2015 | 6.11 | 6.61 | 3.58 | 2.43 |

| Feb 2015 | 7.03 | 6.38 | 3.56 | 2.45 | |

| March 2015 | 6.25 | 6.45 | 3.54 | 2.44 | |

| April 2015 | 5.80 | 6.02 | 3.47 | 2.22 | |

| May 2015 | 5.86 | 6.28 | 3.51 | 2.28 | |

| Thailand | Jan 2015 | 9.60 | 11.20 | 2.80 | 4.60 |

| Feb 2015 | 9.60 | 11.20 | 2.80 | 4.60 | |

| March 2015 | 9.20 | 11.20 | 2.80 | 4.20 | |

| April 2015 | 9.88 | 11.07 | 2.77 | 4.47 | |

| May 2015 | 9.05 | 10.57 | 2.64 | 3.68 | |

| Malaysia | Jan 2015 | 10.10 | 10.25 | 2.60 | 3.52 |

| Feb 2015 | 9.86 | 10.21 | 2.46 | 3.68 | |

| March 2015 | 9.92 | 10.28 | 2.48 | 3.68 | |

| April 2015 | 9.93 | 10.28 | 2.48 | 3.68 | |

| May 2015 | 9.82 | 10.18 | 2.46 | 3.68 | |

| Vietnam | |||||

| HCM | Jan 2015 | 15.75 | 16.96 | 9.69 | 4.36 |

| HCM | Feb 2015 | 15.66 | 16.87 | 7.83 | 4.34 |

| HCM | March 2015 | 15.66 | 16.97 | 7.83 | 4.28 |

| HGM | April 2015 | 14.97 | 16.77 | 7.78 | 4.28 |

| HCM | May 2015 | 14.70 | 16.47 | 7.65 | 4.09 |

| China | |||||

| Beijing | Jan 2015 | 14.10 | 19.08 | 4.15 | 4.98 |

| Beijing | Feb 2015 | 16.32 | 16.32 | 4.08 | 4.89 |

| Beijing | March 2015 | 14.73 | 19.28 | 4.21 | 5.05 |

| Beijing | April 2015 | 14.28 | 18.36 | 4.08 | 4.90 |

| Beijing | May 2015 | 14.29 | 18.69 | 4.08 | 4.49 |

| Shanghai | Dec 14 | 19.64 | 19.64 | 5.12 | 3.55 |

| Shanghai | Jan 2015 | 18.67 | 18.67 | 4.98 | 3.52 |

| Shanghai | Feb 2015 | 18.36 | 17.55 | 4.08 | 3.47 |

| Shanghai | March 2015 | 18.94 | 18.02 | 5.47 | 4.00 |

| Shanghai | April 2015 | 18.36 | 20.00 | 5.31 | 3.98 |

| Shanghai | May 2015 | 18.36 | 20.00 | 5.31 | 3.37 |