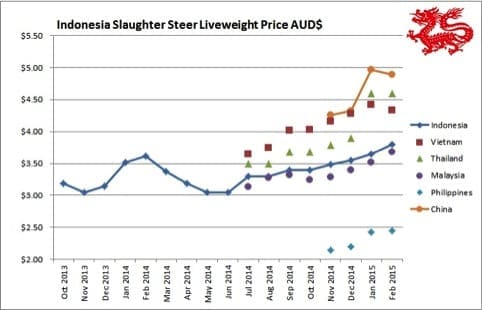

Indonesia: Slaughter steers AUD $3.80/kg live weight

Live cattle prices are climbing as supplies begin to thin out. Some feedlots that imported reduced numbers during Q4 in 2014 have already run out of slaughter cattle.

Those with adequate numbers on feed will be making sure they ration their numbers to look after their customers with a consistent supply.

The supermarket prices have lifted by the largest margin as their supplies of processed beef have been affected the most by the new policy of no permits for secondary cuts (and offals).

As the figures recorded for this report are for knuckle, a secondary cut, it is one of the classes of beef that is in shortest supply. Secondary cuts from the small number of western abattoirs (all in the West Java area) are unlikely to be able to substitute adequate volumes of product to the supermarkets in greater Jakarta let alone the rest of Indonesia. Prices recorded for secondary cuts will begin to vary wildly between those outlets that have run out and those that still have adequate supplies.

Cross rates have been relatively steady this month with the average sticking around Rp10,000 to AUD$1. Live cattle prices in north Sumatera have lifted to around Rp39,500 while in West Java they have risen to Rp37,000. I have “averaged” these out to Rp38,000 for the graph plot as the Java figure relates to a greater proportion of the monthly kill. Local cattle remain at about Rp45,000 throughout Java although this rate is also likely to start to rise further during the coming months as supplies begin to be held back for Ramadan (June/July).

The big question now is how many cattle will be permitted for importation in Q2. Last year this figure could be expected to be announced prior to the end of the previous quarter but this didn’t occur last quarter so it’s anyone’s guess when we will find out. Insiders suggest that the Ministry of Trade is arguing for a larger allocation while the Agriculture Ministry is still satisfied that there are plenty of cattle around therefore imports can continue to be restricted.

Vietnam: Slaughter steers AUD $4.34/kg

The live cattle prices in Vietnam have remained steady since last month. This price stability is despite higher levels of live imports via Cambodia. Ho Chi Minh City (HCM) is the primary driver of the beef market in Vietnam. It is the largest and richest city in the country and consistently has the highest imports, local supply and demand. For these reasons I have chosen to reduce my Vietnamese reporting sites to cover only cattle and beef prices in HCM City. The steer price above relates to VND72,000 per kg live weight which is the HCM rate today. Hanoi remains at 75,000. Using exchange rate of VND 16,600 to AUD$1.

An article in the Vietnamese press last week noted that the national beef cattle herd was in the order of 5 million head. This is the first confidently expressed figure that I have seen and could well be in the right order of magnitude. It would certainly explain the high levels of demand for imports given that 5 million head of cattle, many of which would be used for draft, would have no hope feeding 90 million Vietnamese beef lovers. If 5 million beef cattle produced an optimistic 1.5 million head for slaughter annually, with a carcase weight of say 180kg, this would provide consumers with 270,000 tonnes of carcase beef. When this volume is divided by 90 million consumers it equates to an annual consumption of 3 kg per head. Probably just enough for everyone to get their fix of Pho (beef noodle soup), but not much more. If a significant proportion of the national annual cattle production ends up being trucked live into China then the volume left for local consumers shrinks even further.

I took the first photo below in an abattoir in HCM city last month where the owners explained that many of their cattle are sourced from Mae Sot on the Myanmar/Thai border. I took the second photo of the two cattle on the loading ramp at Mae Sot sale yards last Friday. These animals are examples of a well established Myanmar beef breed called a Shew Ni which are short stature, red cattle while there is another major Myanmar breed seen in the export market which is a tall grey animal called a Pyar Zein. More on these cattle in later blogs.

Slaughter bull ex Myanmar at Ho Chi Minh abattoir February 2015.

Feeder bulls ex Myanmar at the Mae Sot sale yard last Friday 27th February 2015.

Thailand: Slaughter steers AUD $4.60/kg

Prices and exchange rate with the AUD have remained remarkably stable throughout February. I am still using 25 Baht for $1AUD.

The significant news for January is that the first two shipments of Australian cattle have been delivered with another one on the water and due to arrive in the second week of March. These shipments were a mixture of feeder and slaughter cattle providing importers with a combination of immediate slaughter and feeding options. Reliable sources advise that there are a significant number of new importers in the process of getting their supply chains in order so the predictions that Thailand could import 20–30,000 head of live cattle from Australia during 2015 look pretty sound.

This new source of cattle from Australia provides Thailand with three supply options: overland from Myanmar, the domestic breeder herd and now Australian imports. Supplies from Myanmar appear to be secure and have potential to increase, albeit slowly while locally bred cattle are in very short supply. Cattle and buffalo imported from Myanmar are expensive and are, in general, genetically inferior to Australian stock so this market appears likely to be a good steady customer for the longer term.

Last week I visited Mae Sot, a small Thai town on the western border with Myanmar. This is the only significant location where cattle and buffalo from Myanmar enter Thailand. The photo below is of the Mae Sot sale yard where about 3000 cattle and 1000 buffalo are sold every Friday. Prices in the sale yard are a little over 100 Baht per kg or AUD$4 per kg live weight. The details of the border crossing and cattle sale are the subject of some upcoming articles.

Friday Cattle sale at Mae Sot, western Thailand. 3000 Cattle, 1000 buffalo.

Malaysia: Slaughter steers AUD $3.68/kg

Once again, little change in the Malaysian market with the slight price increase resulting from currency fluctuations only. Exchange rate used RM 2.84 = AUD$1

Philippines: Slaughter cattle AUD $2.45 / kg (mainly cull cows & bulls)

Cattle prices have edged up very slightly during February while the cross rates have remained relatively steady for most of the month. Beef and chicken prices remain steady.

Optimism persists in the Philippines as they continue to enjoy an extended run without the usual natural or man-made disasters. Peso 34.5 to AUD$1.

China: Slaughter Cattle AUD $4.89 / kg (RMB 4.9 = AUD$1)

The prices reported by my agents for slaughter cattle this month have remained the same as in January – RMB24 per kg in Beijing and RMB17 in Shanghai. I will use 24 for the monthly slaughter price as I am confident that the very low price in Shanghai is a special case while cattle supplies remain short in the rest of the country. The flood of cull dairy cattle onto the market in the Shanghai area is showing no signs of let up as reflected by the price remaining at a very low RMB17 per kg. Chinese New Year appears to have only had a minor affect on retail prices.

The fundamentals however do not appear to have changed so the long-term shortage of supply remains the dominant market driver. Last month I speculated that the Chinese domestic beef cattle herd was around 60 to 70 million head. I have recently received reliable advice that this figure is actually closer to 60 million.

Cattle producers and exporters are reporting huge interest from large Chinese corporations desperate to import live cattle to fill their empty feedlots and abattoir supply chains. Import demand for live cattle from Thailand and Vietnam continues without any sign of weakening. Given all these indicators, the pressure for the Chinese government to resolve the health protocol issues and commence live cattle imports from Australia must be reaching a point where they decide to open the gates.

This monthly market report is first published exclusively on Beef Central. To view more of Dr Ross Ainsworth’s previous articles on South East Asia, click here to view archived articles on Beef Central and here to visit his personal South East Asia blog site.

Market price table for February 2015

(All prices converted to AUD)

These figures are converted to AUD$ from their respective currencies which are changing every day so the actual prices here are corrupted slightly by constant foreign exchange fluctuations. The AUD$ figures presented below should be regarded as reliable trends rather than exact individual prices. Where possible the meat cut used for pricing in the wet and supermarket is Knuckle / Round.

| Location | Date | Wet MarketAUD$/kg | Super market$/kg | Broiler chicken$/kg | Live SteerSlaughter WtAUD$/kg |

| Jakarta | October 14 | 10.37 | 11.32 | 2.73 | 3.30 |

| Nov 14 | 10.62 | 11.58 | 2.90 | 3.38 | |

| Dec 14 | 11.33 | 11.82 | 3.25 | 3.44 | |

| Jan 2015 | 11.00 | NA | 3.50 | 3.60 | |

| Feb 2015 | 11.00 | 12.75 | 3.30 | 3.70 | |

| Medan | October 14 | 8.58 | 8.30 | 1.32 | 3.53 |

| Nov 14 | 9.17 | 9.66 | 1.35 | 3.67 | |

| Dec 14 | 9.35 | 9.85 | 1.57 | 3.74 | |

| Jan 2015 | 3.75 | ||||

| Feb 2015 | 11.75 | 11.75 | 1.70 | 3.95 | |

| Philippines | October 14 | 5.10 | 5.22 | 3.06 | 1.98 |

| Nov 14 | 5.43 | 5.48 | 3.32 | 2.14 | |

| Dec 14 | 5.65 | 5.70 | 3.40 | 2.20 | |

| Jan 2015 | 6.11 | 6.61 | 3.58 | 2.43 | |

| Feb 2015 | 7.03 | 6.38 | 3.56 | 2.45 | |

| Thailand | October 14 | 8.42 | 9.82 | 2.45 | 3.68 |

| Nov 14 | 8.68 | 10.12 | 2.53 | 3.79 | |

| Dec 14 | 8.92 | 10.40 | 2.60 | 3.90 | |

| Jan 2015 | 9.60 | 11.20 | 2.80 | 4.60 | |

| Feb 2015 | 9.60 | 11.20 | 2.80 | 4.60 | |

| Malaysia | October 14 | 9.66 | 9.50 | 2.24 | 3.24 |

| Nov 14 | 9.62 | 2.47 | 3.29 | ||

| Dec 14 | 9.79 | 10.05 | 2.52 | 3.40 | |

| Jan 2015 | 10.10 | 10.25 | 2.60 | 3.52 | |

| Feb 2015 | 9.86 | 10.21 | 2.46 | 3.68 | |

| Vietnam | |||||

| H | Sept 14 | 13.41 | 16.58 | 6.97 | 4.02 |

| HCM | Sept 14 | 11.80 | 13.95 | 6.97 | 4.02 |

| H | October 14 | 13.44 | 16.61 | 6.99 | 4.03 |

| HCM | October 14 | 11.82 | 13.97 | 6.99 | 4.03 |

| H | Nov 14 | 13.89 | 17.18 | 5.55 | 4.16 |

| HCM | Nov 14 | 12.78 | 14.45 | 9.44 | 4.16 |

| Hanoi | Dec 14 | 4.28 | |||

| Ho Chi Minh | Dec 14 | 13.14 | 14.86 | 8.57 | 4.28 |

| Ho Chi Minh | Jan 2015 | 15.75 | 16.96 | 9.69 | 4.36 |

| Ho Chi Minh | Feb 2015 | 15.66 | 16.87 | 7.83 | 4.34 |

| China | |||||

| Beijing | Nov 14 | 12.40 | 19.72 | 4.64 | 24 RMB |

| Shanghai | Nov 14 | 17.40 | 17.40 | 4.64 | 18 RMB |

| Beijing | Dec 14 | 13.80 | 19.64 | 3.94 | 4.73 |

| Shanghai | Dec 14 | 19.64 | 19.64 | 5.12 | 3.55 |

| Beijing | Jan 2015 | 14.10 | 19.08 | 4.15 | 4.98 |

| Shanghai | Jan 2015 | 18.67 | 18.67 | 4.98 | 3.52 |

| Beijing | Feb 2015 | 16.32 | 16.32 | 4.08 | 4.89 |

| Shanghai | Feb 2015 | 18.36 | 17.55 | 4.08 | 3.47 |