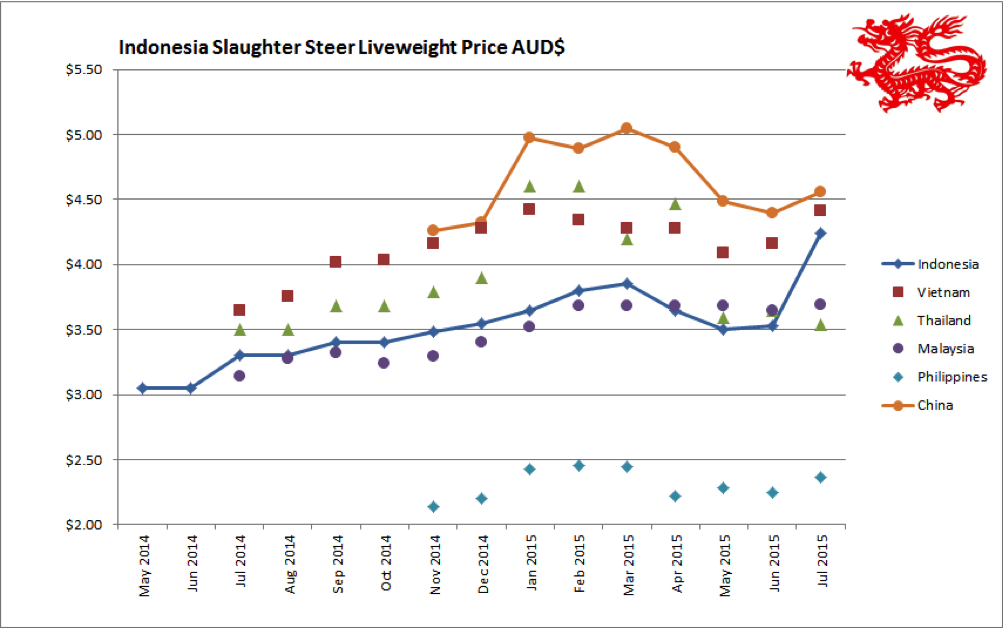

Indonesia: Slaughter Steers AUD $4.10 / kg live weight (Rp10,000 = $1AUD)

While there have been some major announcements relating to future import permit allocations from the Indonesian government during August, the future for importers is more unclear than it has ever been.

At the beginning of August the government announced that an additional 50,000 head of import permits would be issued for Q3 but the importation of these cattle would be under the control of the State Owned logistics agency called BULOG. As Bulog does not have an importers license or any ESCAS approvals, it would operate through the State Owned Enterprise (SOE) Berdikari which manages a number of small to medium sized feedlots around West Java. As Berdikari has supply chains approved with only three Australian exporters this means that until further supply chains can be established, Bulog can only import through three exporters and one relatively small capacity importer. To make matters a little more difficult, the import permits were for slaughter cattle which are rather scarce in northern Australia at the moment and prices of all cattle across Australia are rising faster than they have in the last 40 years. At the end of August only about 8000 head had been imported by Bulog.

Early in the month the Ag Minister initiated a police investigation into the live cattle import industry following allegations that feedlotters were withholding fat cattle from the market with the aim of manipulating the price to an excessively high level. All reports appear to indicate that the police found no evidence of excessive “hoarding” of cattle and in fact confirmed what industry already knew, which is that numbers on feed are quite low and not adequate to supply the market with the volumes of product needed to prevent prices from remaining at historical highs. Butchers also demonstrated around West Java and Lampung, complaining that there was not enough cattle to supply the needs of their customers and that rapidly rising prices were forcing them out of business.

Just to add a further complication, feedlotters are required by law to hold feeder cattle for a minimum of 120 days in the feedlot before being permitted to sell into the market so the government’s own rules are one of the many reasons that the feedlotters are not in a position to suddenly send more cattle to supply the market with the aim of dampening prices.

‘You can only feel for importers who find themselves in an impossible position’

Later in August there was a Ministerial reshuffle. The new Minister for Trade reviewed the situation and announced that permits for 300,000 head would be issued for Q4 but with no details as to who would get the permits and what conditions might be attached to them. The Minister for Agriculture, who survived the reshuffle, then announced to importers that he expected them to sell their slaughter cattle at Rp38,000 per kg live weight which I am advised is in most cases below the cost of importation. You can only feel sorry for the importers who find themselves in an impossible position. If they offer to act as a subcontractor for state owned Berdikari then it is likely that they would be expected to sell their cattle at the prices set by the Minister. If they don’t cooperate with the Bulog supply chain then they run the risk of getting no permits for imports under their own independent license arrangements. Either option represents a serious risk to their future profitability.

Efficient feedlotters are able to make modest profits even when they sell below the cost of cattle purchases if their fattening process is highly efficient. The key to this business model however is throughput. Very tight margins can be offset by large numbers fattened but clearly this is not an option at present until the Q4 permits are clarified. Further black clouds are building on the horizon as a result of the rapidly rising prices in Australia and the forthcoming northern wet season. Prices always rise during Q4 and Q1 because this is the most difficult time for Australian producers to supply. If the issue of a rapidly shrinking Australian herd is combined with a potentially large demand, if 300,000 permits are finally allocated during October, the result can only be even higher price rises at the farm gate in Australia so it looks like further pain for importers regardless of the permit outcome.

As at the end of August, the Minister’s wishes were being granted by a significant proportion of importers who were selling fats at Rp38,000 per kg live weight. Prices in north Sumatera were closer to Rp42-44,000 while some importers in Java and South Sumatera have chosen not to follow the Minster’s request entirely with sales from Rp40 to Rp42,000 – still a lot less than prices in the beginning of the month when they reached as high as Rp46,000. For this month’s report I am using an “average” price of Rp40,000 for the price chart. While the Minister appears to have remarkable control over the prices that the importers sell to slaughter houses, I am sure he has no control over the 10,000 or more middle men and retail outlets across the country. My guess is that these entrepreneurs will happily take the discounted slaughter cattle prices but then sell into the retail market at a rate that actually reflects the true supply and demand situation i.e. short supplies and high beef prices to the public.

The Indonesian government are once again looking seriously at allowing imports of beef and live animals from countries that have FMD free zones. This certainly includes Brazil and potentially India. While box meat might be a chance, I don’t think there is any real risk that live cattle will come from such locations once all the costs, risks and complications are fully considered. As there are significant legal, legislative and logistic hurdles to overcome, this option will take some years to fully open up if ever.

The Rupiah has followed the collapse of the AUD very closely so this is one aspect that the importers don’t have to worry about for the moment.

There is quite a bit of talk in the coffee shops and in the press here about the weakening of the Indonesian economy. I visited my local supermarket again last week and found that they were selling Australian Wagyu Rib Eye for AUD$150 per kg so someone must still be doing OK.

Most food products in Indonesia are sold by the 100 gram units. This Wagyu steak is selling for AUD $15 per 100 grams or AUD$150 per kg.

Vietnam: Slaughter Steers AUD $4.19 / kg (VND16,000 to $1AUD)

The Vietnam beef industry is now being forced to endure a major re-evaluation of the pricing structures within their business models.

As the trade began to seriously ramp up in 2014, the outflows of cattle from new feedlots remained modest which kept fat cattle prices high across the entire country. Importers naturally used these selling prices as their guide when planning their investment strategies, buy in prices and margins. The high selling prices at the time allowed them to pay more than any other market for live cattle from Australia. This also drove additional supplies to be delivered overland from Myanmar and Thailand via Cambodia and Laos. Large numbers of high capacity feedlots were quickly constructed during 2013/14 and cattle imported at high prices to fill them. When these very large numbers of feeder cattle finally became ready for sale over the last 6 months (and still coming) they effectively flooded the market and began to depress prices. For importers with large inventories, and large debits to go with them, there is little room to manoeuvre once the cattle are ready for sale. If they sell them in to a falling market they stand to lose some or all of their expected margin. If they hold them back, they still need to be fed an expensive ration so their margins are eroded just the same. My sources in Vietnam advise that while the price is still holding at close to Dong70,000 per kg live for fat cattle in the north, reports of discounting slaughter steers to Dong65,000 in the south are now common. I have even heard reports of heifers selling in the south for Dong 63,000. Only 6 months ago the price in the north was Dong75,000 while the price in the south was Dong72,000 and firm.

When these falling margins are combined with the ongoing pressure to enforce ESCAS requirements and a skyrocketing price of Australian feeder and slaughter cattle, the next 6 months in the Vietnam industry will be an extremely challenging period during which some of the less efficient operations may have difficulty surviving.

Thailand: Slaughter Steers AUD $4.31 / kg (Baht 25.5 to $1AUD)

Thai prices have recovered significantly following the re-start of the Mekong river trade to China and the reopening of the Myanmar border crossing. Seasonal conditions have also improved with monsoon rains finally delivering welcome storms. The monsoon also arrived in Myanmar with some massive rainfall events leading to severe flooding in some areas where cattle are produced. See photo below:

Burmese cattle escaping recent monsoonal flood waters.

Low margins and a reluctant uptake of ESCAS requirements has resulted in a very slow start to the importation of live cattle from Australia. Only one shipment was delivered during August making a total of 4 since the opening of the trade earlier this year. Difficult trading conditions are likely to continue to keep the numbers of live imports at a low level for the medium term future.

Thai importers and officials are considering a potential offer of live cattle from Brazil at a price that is quite competitive to those from Australia. It is likely that this offer is related to a back-loading opportunity provided by a shipment of animals going to South America then returning with a load of cattle from one of the FMD free zones of Brazil. As Thailand, Cambodia and Vietnam are all endemic for FMD there is little additional risk from importing live cattle from FMD free zones. The fact that these cattle will not be subject to ESCAS requirements will be an additional attraction with significant opportunity for better trading margins.

Malaysia: Slaughter Steers AUD $3.46 per / kg (RM3.00 to $1 AUD)

The Malaysian Ringgit has devalued 6% during the month against the AUD!

In Ringgit terms, fresh beef (knuckle) is selling for RM 28 per kg in the wet market and RM 35 per kg in the supermarkets. Frozen Indian buffalo beef (strip loin) is selling for RM 16 per kg so competition is tough.

Malaysia has millions of hectares of palm oil plantations but has been prevented from profitable integrated cattle production due to cheap live imports from Thailand and even cheaper frozen Indian buffalo beef. Now that world prices are climbing steeply, planters are giving cattle breeding a serious rethink providing another potential future market for Australian breeders. I recently visited the Sarawak plantation belonging to Jeffrey Ong and his family where they are pioneering some new cattle and plantation management strategies to lead the way for other Malaysian planters to follow. One simple but effective strategy is to sell all male production once a year for the Qurban religious festival. This makes for simplified marketing and achieves the highest price every year.

Breeders imported from Australia on the Ong plantation near Kuching in Sarawak.

Philippines: Slaughter Cattle AUD $2.58 / kg (mainly cull cows & bulls)

The Philippines is one of the few places in Asia to buck all the trends with beef prices rising slightly in the markets (in local currency) while the Peso has firmed a little against the AUD. As this country has very little of their own oil and gas resources, their economy gets a major boost from low oil prices. Add to that a run of relatively good seasons and only a few minor recent natural disasters and the Filipino economy is moving forward nicely. Peso 33.3 to AUD$1

China: Slaughter Cattle AUD $4.67 / kg (RMB 4.5 = AUD$1)

Little to report from China this month where prices for slaughter cattle remain weak although retail prices in the two major cities of Beijing and Shanghai are fairly constant. Shanghai continues to liquidate large numbers of cull dairy cattle with prices slipping to as low as 16 Y per kg live weight. Beijing prices remain around the 21Y level. The apparent price rise since August is a reflection of the collapse of the AUD being even greater than the official devaluation of the Yuan by the Chinese government.

While there is plenty of hype surrounding the forthcoming shipments of live cattle from Australia to China it may be a few more months before the first delivery takes place. Word is that the earliest shipments may well be small numbers by air.

The two photos below are a nice demonstration of how Chinese tastes differ from those in the west. The chicken feet below are more expensive than legs and thighs!

Supermarket photos from Angus Adnam during a trip to China in August.

Dr Ross Ainsworth’s monthly South East Asian reports are first published exclusively on Beef Central. To view more of Dr Ainsworth’s previous Beef Central articles click here. To visit his personal South East Asia report blog site, click here.

Market price table for August 2015

(All prices converted to AUD)

These figures are converted to AUD$ from their respective currencies which are changing every day so the actual prices here are corrupted slightly by constant foreign exchange fluctuations. The AUD$ figures presented below should be regarded as reliable trends rather than exact individual prices. Where possible the meat cut used for pricing in the wet and supermarket is Knuckle/Round.

| Location | Date | Wet MarketAUD$/kg | Super market$/kg | Broiler chicken$/kg | Live SteerSlaughter Wt

AUD$/kg |

| Jakarta | March 2015 | 10.50 | 12.00 | 3.00 | 3.85 |

| April 2015 | 11.00 | 15.00 | 3.60 | 3.65 | |

| May 2015 | 10.68 | 12.33 | 2.52 | 3.50 | |

| June 2015 | 10.78 | 14.60 | 2.94 | 3.53 | |

| July 2015 | 13.13 | 19.19 | 3.38 | 4.24 | |

| August 2015 | 13.00 | 19.00 | 2.70 | 4.10 | |

| Medan | March 2015 | 10.00 | 12.00 | 1.40 | 3.90 |

| April 2015 | 9.70 | 11.50 | 1.70 | 4.00 | |

| May 2015 | 9.32 | 9.90 | 2.14 | 3.69 | |

| June 2015 | 9.41 | 10.09 | 2.35 | 3.73 | |

| July 2015 | 12.12 | 10.30 | 3.22 | 4.24 | |

| August 2015 | 11.50 | 11.50 | 2.60 | 4.20 | |

| Philippines | March 2015 | 6.25 | 6.45 | 3.54 | 2.44 |

| April 2015 | 5.80 | 6.02 | 3.47 | 2.22 | |

| May 2015 | 5.86 | 6.28 | 3.51 | 2.28 | |

| June 2015 | 5.88 | 6.40 | 3.17 | 2.25 | |

| July 2015 | 6.09 | 6.60 | 3.58 | 2.36 | |

| August 2015 | 6.30 | 6.76 | 3.69 | 2.58 | |

| Thailand | March 2015 | 9.20 | 11.20 | 2.80 | 4.20 |

| April 2015 | 9.88 | 11.07 | 2.77 | 4.47 | |

| May 2015 | 9.05 | 10.57 | 2.64 | 3.68 | |

| June 2015 | 8.85 | 10.76 | 2.69 | 3.65 | |

| July 2015 | 9.45 | 11.02 | 2.75 | 3.54 | |

| August 2015 | 9.02 | 10.98 | 2.75 | 4.31 | |

| Malaysia | March 2015 | 9.92 | 10.28 | 2.48 | 3.68 |

| April 2015 | 9.93 | 10.28 | 2.48 | 3.68 | |

| May 2015 | 9.82 | 10.18 | 2.46 | 3.68 | |

| June 2015 | 9.72 | 10.42 | 2.36 | 3.65 | |

| July 2015 | 9.93 | 10.63 | 2.53 | 3.69 | |

| August 2015 | 9.33 | 11.66 | 2.40 | 3.46 | |

| Vietnam | March 2015 | 15.66 | 16.97 | 7.83 | 4.28 |

| HCM City | April 2015 | 14.97 | 16.77 | 7.78 | 4.28 |

| May 2015 | 14.70 | 16.47 | 7.65 | 4.09 | |

| June 2015 | 14.97 | 16.77 | 7.78 | 4.16 | |

| July 2015 | 15.53 | 17.39 | 8.07 | 4.41 | |

| August 2015 | 15.63 | 17.50 | 8.13 | 4.19 | |

| China | March 2015 | 14.73 | 19.28 | 4.21 | 5.05 |

| Beijing | April 2015 | 14.28 | 18.36 | 4.08 | 4.90 |

| May 2015 | 14.29 | 18.69 | 4.08 | 4.49 | |

| June 2015 | 14.66 | 19.20 | 4.19 | 4.40 | |

| July 2015 | 15.20 | 17.30 | 4.35 | 4.56 | |

| August 2015 | 15.55 | 17.69 | 4.44 | 4.67 | |

| Shanghai | March 2015 | 18.94 | 18.02 | 5.47 | 4.00 |

| April 2015 | 18.36 | 20.00 | 5.31 | 3.98 | |

| May 2015 | 18.36 | 20.00 | 5.31 | 3.37 | |

| June 2015 | 18.87 | 20.55 | 5.45 | 3.98 | |

| July 2015 | 19.56 | 16.95 | 5.22 | 4.02 | |

| August 2015 | 20.00 | 21.33 | 5.33 | 3.55 |