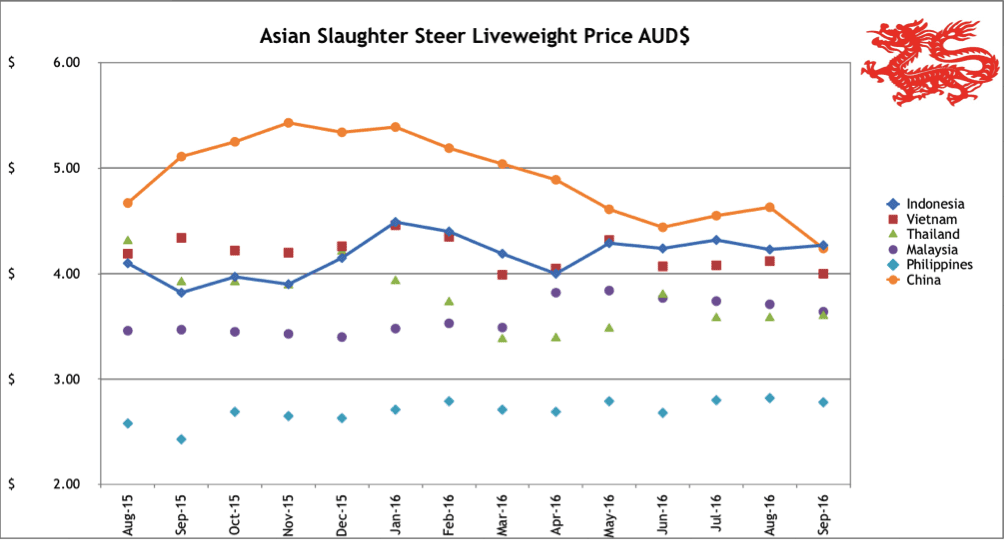

Indonesia: Slaughter Steers AUD $4.27/kg live weight (Rp9,950 = $1AUD)

Live steer prices remain unchanged with the average at Rp42,500 per kg live weight. The apparent small increase in the AUD price above is due to currency movements only. As for last month, importers dare not increase slaughter cattle prices in case they are punished by the various interested Ministries.

Most importers are yet to receive their import permits for T3 because they have so far refused to officially agree to the government of Indonesia’s (GOI) demands for imports of breeding cattle on a 1 to 5 ratio with feeders. These demands are further complicated by the fact that some Ministerial “policies” are verbal via press releases, some are verbal via direct contact with exporters individually or as a group and some are actual regulations. Given the massive capital investments involved in this industry, it seems extremely dangerous for any business to make such critical commercial decisions with such a limited level of certainty.

As an example, a medium-sized importer with a feedlot capacity of say 10,000 head would expect to have three full cycles of fattening per year, so would need to buy a total of close to 30,000 head of feeders in the course of an average year.

Throughput must be evenly spread to provide consistent operational activity and consistent supplies to customers. This means that the monthly imports will need to average about 2,500 head of feeders at say 320 kg live weight. Using a very conservative estimate of today’s rates, where the imported price might be in the order of AUD$4.40 per kg (or more) CIF, average monthly shipments carrying this number will mean an outlay of 2,500 head x $4.4 per kg x 320 kg = AUD$3,520,000 per month.

I suspect that most importers don’t have this amount of cash sitting in their savings account so they will have to go to the bank and ask for credit to not only buy these animals but also enough operational cash to feed 2,500 head for three to five months, say another million dollars or so. So every month they must access credit for about AUD$4.5 million and wait three to five months for a return with the possibility of having close to $20 million on credit from the bank at any one time.

Now add the new demands to buy breeders at a ratio of 1 breeder to every 5 feeders meaning that notionally, the importer needs to buy another $750,000 worth of breeders per month (breeders are more expensive than feeders) to match 20% of the feeder numbers.

They don’t need to come in all at the same time but the “breeder obligation” continues to build and must be delivered at some point into the not too distant future. And these breeders don’t exit the feedlot in 120 days with a potential for profit, they accumulate over the coming years and eat and eat and eat.

It’s not difficult to see why most importers can’t see any commercial sense in complying with the GOI demands to sign up with the new arrangements considering the rather hazy policy requirements and the massive investment required.

My advice is that with zero imports during September (the first month of T3) and only a very limited number of permits allocated so far to only 3 importers, numbers of cattle on hand in feedlots is alarmingly low and, assuming further delays in import permit allocations, feedlots are expected to essentially run out of fat cattle around January.

As we have seen on a number of occasions in the past when imported feeders have been blocked through a variety of reasons, when the feedlots are empty the focus for fresh beef shifts to the domestic breeding herd.

A large proportion of the males in the herd have just been slaughtered for the festival of Eid ul Adha with the result being that the majority of fat cattle remaining in the local herd are breeding females. With no other alternatives and prices for these local cattle at very attractive rates, the sale of these breeders for slaughter becomes an extremely attractive proposition. And crash goes the domestic herd once again.

If all this is not disturbing enough, the fate of the supply and demand dynamics for next year’s Ramadan festival are now effectively set with supplies of slaughter-ready live cattle almost certainly going to be completely inadequate. Ramadan for 2017 commences on the 27th May and concludes on the 25th of June 2017.

Assuming cattle are fed for 120 days in the feedlot, then in order to have fat cattle ready for sale on the 27th of May, feedlots must be well stocked 120 days earlier or some time in February. If we take into account the analysis above which estimates that feedlots will be almost destocked by January and combine that with the normal supply difficulties and price spikes from northern Australia during the wet season from December to March, then the chances of feedlots having anything like reasonable stock levels in February are virtually zero.

One can only guess at the new level of finger pointing from all parties when someone needs to be identified as the cause of this highly unsatisfactory situation. For once the importers should be on fairly safe ground because if they don’t get import permits allocated to them then they can hardly be blamed for failing to import.

Indian buffalo meat continues to be imported with lots of new supply chains being established to allow effective distribution to the retail consumers. There is very little feedback on its impact at the moment with most wet markets currently preferring to offer only fresh product from both local and imported live cattle sources.

The role of buffalo beef will soon be tested when supplies of fresh product begin to dry up. Perhaps by the time Ramadan comes around Indonesian consumers will have embraced buffalo beef consumption and the supply and price problems for the nation will be solved.

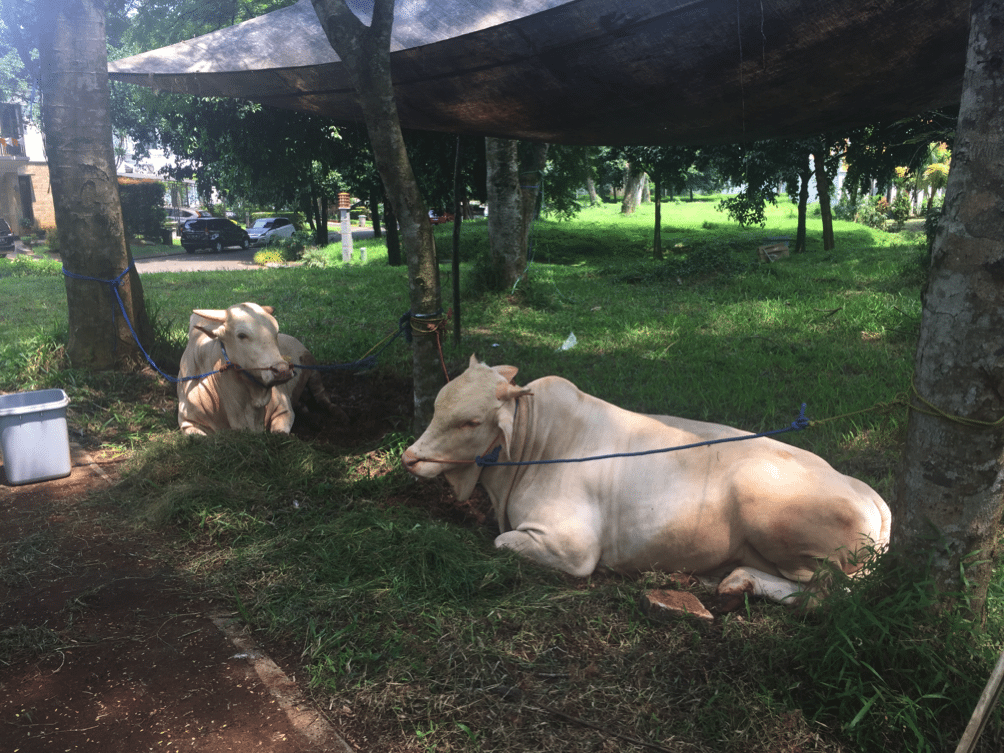

The Islamic celebration of Eid ul Adha took place on 12th of September. During this celebration the faithful are encouraged to purchase bulls or sheep or goats and donate them to the local Mosque. The Mosque then arranges for the ritual slaughter and distribution of the meat to the poorer people in the community.

The two magnificent bulls in the first picture below were held for a few days on a vacant block in my residential compound before being slaughtered on this site on the day of the Eid. The second picture is the volunteers from the local community cutting up the meat and measuring it out into 1 kg lots and packing it in the red plastic bags. These bags are then distributed to the helpers and the needy as soon as the process has been completed.

Click on images to view in larger format.

Vietnam: Slaughter Steers AUD $4.00/kg (VND17,000 to $1AUD)

Domestic prices have eased slight during September with top prices in the dominant southern market backing off to Dong 69,000 while top northern rates remain at D74,000. With bottom prices in the south down as low as Dong 64,000 and 67,000 in the north I have chosen Dong 68,000 as the indicator price for September.

My sources tell me that Vietnamese feedlot capacity is now in the order of 150,000 head following some significant new facilities being constructed during the last 12 months. At the present time the best estimate that I have is that this capacity is about 50% utilized. This low usage is driven by a number of factors including a slowly rising CIF price and the Australian government suspending a number is significant supply chains including two Australian exporters, several feedlots and a large number of their associated abattoirs as a result of a range of non-compliance issues with ESCAS regulations. The two Australian exporters have recently regained their access to the Vietnamese trade and at least one of them has already delivered a shipment in recent weeks.

North Vietnam is receiving large numbers of Burmese cattle that have been fattened in Thailand and trucked overland through Laos. See the photo below showing these cattle apparently in excellent shape after their journey across Thailand and Laos. My advice is that their landed price in Vietnam is around 20 cents per kg higher than Aussie imports.

Burmese fats after spending time in Thai feedlots then being exported by road to North Vietnam via Laos.

The Vietnamese importers are one of the very few beneficiaries of the ongoing Indonesian import restrictions as they represent the only significant alternative export destination for Aussie exporters who need to keep their ships moving.

This unique opportunity has allowed the Vietnamese importers to keep the lid on CIF prices from Australia despite strong feeder rates in northern Australia and some exporters ending their time charter shipping obligations.

The next six months will see a major shift in this trade as higher imported cattle prices collide with understocked feedlots. With a bit of luck, significantly lower kills in Vietnam will force domestic prices up and in due course allow importers to pay the increased CIF rates necessary for exporters to operate in the black. Watch this space.

Thailand: Slaughter Steers AUD $3.60/kg (Baht 26.4 to $1AUD)

Thai live cattle markets remain weak with the best prices only available for high quality slaughter cattle suitable for export to Vietnam. These cattle have recently achieved Bht105 farm gate but the domestic prices still battle to pass the 90 Baht mark for local slaughter. Local feeders can achieve 95 Baht per kg.

Given this split I have once again used 95 for this report’s indicator price. The 105 price for export was only available with testing and certification that the cattle had not been treated with illegal Beta-agonists. These pirate chemicals continue to be a problem in the Thai industry with their use and discovery in some local feedlots blamed for the loss of valuable market access into China.

Malaysia: Slaughter Steers AUD $3.64 per/kg (RM3.13 to $1 AUD)

The Malaysian exchange rate continues its steady decline while the local live cattle prices are quite stable. This explains why the live price in AUD has declined to $3.64. The beef market is subdued after the major celebration of Eid ul Adha on the 12th of September.

Philippines: Slaughter Cattle AUD $2.78/kg (Peso 36.0 to AUD$1)

Prices for live cattle in the Peso are stable with a slight weakening of the currency the cause of the small change in the AUD figure above since last month. My agent in the Philippines has sent me such an upbeat monthly comment that I thought that it would be best passed along in full so you get the strong tone of his very personal observations:

“As we are nearing the end of the 3rd quarter, we can say, it’s going to be a great end of the year. That’s my prediction. We see many positive things happening around us and I am NOT referring to the average of 40 people a day who get shot in the anti drug campaign. We see shelves emptying as fast as they are refilled. Super Markets and Market places are somehow buzzing full of people. We are BUSY. Sales of ALL KIND, are on the rise especially “construction” materials.That’s “always” a good gauge to know how things are working out. In some quarters the “opposition” is trying to “shake” the new president, which would make matters “unstable”, but as of yet, HE HAS THE SUPPORT ACROSS THE BOARD from the population. and while the Peso has slightly lost value, the market is doing well.”

Cambodia: (Cambodian Riel (KHR) 3,176 to AUD$1)

David Tea from SLN reports that prices are similar to last month with their vacuum packed knuckle selling for AUD$11.20 in the wet market and the same product selling for AUD$14.80 supermarket. During the last few days, Cambodians celebrated Pchum Ben or Ancestor day (or Hungry Ghost Festival) which is a major public holiday in for the country. Prices for local beef and chicken doubled while SLN maintained their rates at normal levels.

SLN meat shop display with all cuts presented in vacuum packaging.

China: Slaughter Cattle AUD $4.24/kg (RMB 5.07 = AUD$1)

Live slaughter cattle prices are sliding fast in both Beijing and Shanghai this month. Beijing reports Y20 -23 per kg while the rate in Shanghai has fallen to Y15.6. For this month’s indicator price I will continue to use the Beijing price and average these figures at Y21.5.

No reason given for the drop in Beijing while the continued cow cull from the unprofitable dairy industry remains the reason provided for the weakness in Shanghai slaughter market.

The most interesting part of the reports this month is that my agent in Beijing advises that for the “first time, the very low price beef from Brazil displayed in the supermarket, priced at Y50 per kg”. This is a dramatic discount to the current rate for our usual reported product (knuckle) which has been selling for around Y91.6 for most of this year while this month’s price is Y94.5.

It would be reasonable to assume that this is a special price to get customers to try this “new” offering. As we know, Brazilian beef has been imported in vast quantities through the grey channels of Hong Kong and Vietnam but it would not have been wise to advertise its origin when everyone knew it was smuggled product.

Brazil and USA and China – some positive information to calm the nerves.

On the face of it, the newly opened access for Brazilian beef to the US and China and for US beef into China look like very dangerous competitive threats to Aussie beef exports.

BUT:

· The Brazilians have access to the US but are restricted by a quota system which will only allow them to export about 40,000 tons for the rest of this financial year with restrictions continuing into the future. At this time the total quota for the Brazil category of US access is 64,800 tons which they share with “other countries” so unless the US changes the rules further Brazilian imports will be limited to modest volumes.

· Brazil and the USA had already been exporting “freely” into China but by the back door grey channel through Hong Kong and Vietnam. What will happen when both their beef exports go through the front door is that they will attract import tariffs from the Chinese government who think that they should get them instead of the smugglers enjoying all the margins.

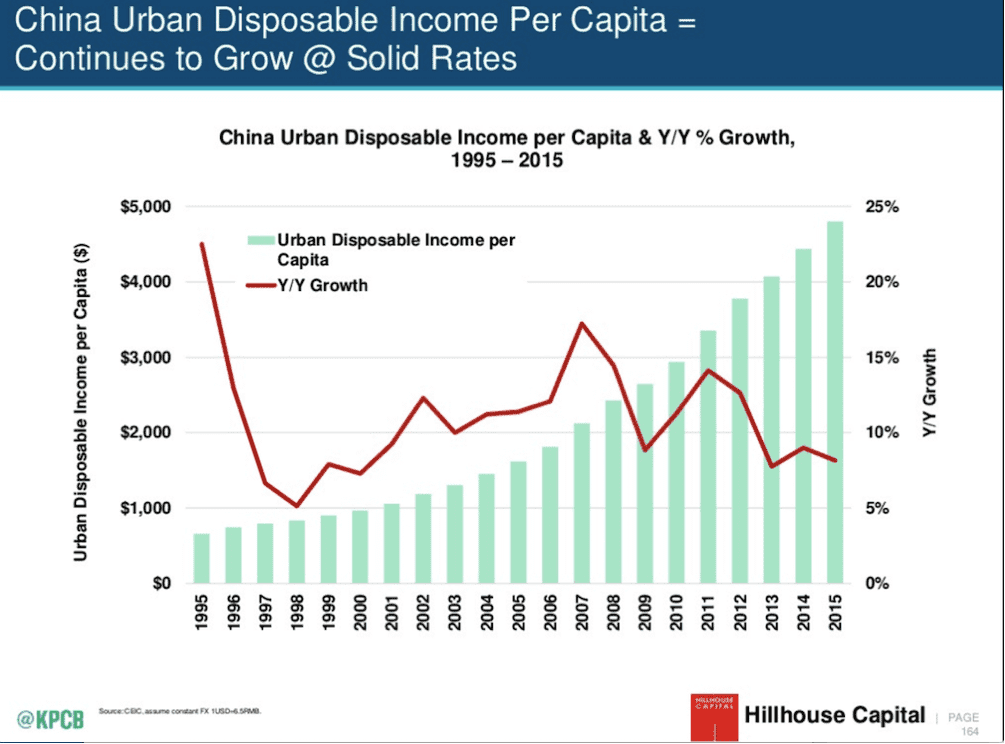

· Beef remains one of the premier foods in China with high quality Aussie beef sitting up near the top of the pile. Given our premium product position and the continued growth of disposable income of China’s urban population (see graph below) there appears to be little reason to expect that consumption will do anything else than keep rising.

· World bank data states that in 2014, China’s urban population was 749 million people with their numbers continuing to expand. In 1980 the World Bank reported that only 19.6 million Chinese lived in urban environments.

· In the event that these new competitors manage to crush our markets then the prices in Australia will slide. If this happens then China will quickly commence live exports and the Aussie producer will be back in business. One of the main reasons that China has not commenced large scale live exports is that our prices are so high. This new destination waiting in the wings puts a nice floor in the market if it does actually start to fall off the cliff.

· USA beef producers are the largest users of legal HGP’s and Beta-agonists to promote the growth of their cattle in feedlots. As both these products are banned from imports to China, the presence of these two chemicals in the majority of US product should place serious restrictions on eligible volumes. In addition, the US has no HGP markers as Australia does so it becomes much more difficult for them to prove that the meat they are exporting is free of the specified chemicals.

Market price table for September 2016

(All prices converted to AUD)

These figures are converted to AUD$ from their respective currencies which are changing every day so the actual prices here are corrupted slightly by constant foreign exchange fluctuations. The AUD$ figures presented below should be regarded as reliable trends rather than exact individual prices. Where possible the meat cut used for pricing in the wet and supermarket is Knuckle/Round.

| Location | Date | Wet Market

AUD$/kg |

Super market

$/kg |

Broiler chicken

$/kg |

Live Steer

Slaughter Wt AUD$/kg |

| Jakarta | April 16 | 13.00 | 18.20 | 2.90 | 4.00 |

| May 16 | 13.27 | 18.57 | 3.06 | 4.29 | |

| June 16 | 13.63 | 18.89 | 3.54 | 4.24 | |

| July 16 | 13.06 | 17.59 | 3.22 | 4.32 | |

| August 16 | 13.13 | 17.41 | 2.99 | 4.23 | |

| Rp 9,950 | Sept 16 | 13.56 | 17.60 | 3.12 | 4.27 |

| Philippines | April 16 | 7.93 | 7.50 | 3.39 | 2.69 |

| May 16 | 8.38 | 8.23 | 3.38 | 2.79 | |

| June 16 | 8.14 | 7.43 | 3.43 | 2.68 | |

| July 16 | 8.29 | 7.72 | 3.46 | 2.80 | |

| August 16 | 8.45 | 8.17 | 3.80 | 2.82 | |

| P 36.0 | Sept 16 | 8.47 | 8.33 | 3.89 | 2.78 |

| Thailand | April 16 | 9.06 | 10.57 | 2.64 | 3.39 |

| May 16 | 9.27 | 10.81 | 2.70 | 3.48 | |

| June 16 | 8.74 | 10.65 | 2.66 | 3.80 | |

| July 16 | 8.78 | 10.57 | 2.64 | 3.58 | |

| August 16 | 8.68 | 10.57 | 2.64 | 3.58 | |

| Bht 26.4 | Sept 16 | 9.09 | 10.61 | 2.65 | 3.60 |

| Malaysia | April 16 | 10.06 5.87 | 11.74 | 1.85 | 3.82 |

| May 16 | 10.10 5.89 | 11.78 | 2.02 | 3.84 | |

| June 16 | 9.93 5.79 | 8.94 | 2.48 | 3.77 | |

| July 16 | 9.84 5.84 | 8.85 | 2.79 | 3.74 | |

| August 16 | 9.77 5.80 | 9.45 | 2.60 | 3.71 | |

| Rg3.13 | Sept 16 | 9.58 5.69 | 9.58 | 2.49 | 3.64 |

| Cambodia | Sept 2016 | 11.20 | 14.80 | ||

| Vietnam | April 16 | 14.88 | 16.67 | 7.74 | 4.05 |

| HCM City | May 16 | 15.43 | 17.28 | 7.41 | 4.32 |

| June 16 | 14.97 | 16.77 | 7.19 | 4.07 | |

| July 16 | 14.79 | 16.51 | 7.10 | 4.08 | |

| August 16 | 14.70 | 16.47 | 9.41 | 4.12 | |

| D 17,000 | Sept 16 | 14.70 | 16.47 | 9.41 | 4.00 |

| China | April 16 | 14.28 | 18.69 | 4.08 | 4.89 |

| Beijing | May 16 | 14.26 | 19.20 | 4.19 | 4.61 |

| June 16 | 13.73 | 18.50 | 4.04 | 4.44 | |

| July 16 | 13.86 | 18.14 | 3.96 | 4.55 | |

| August 16 | 13.81 | 17.95 | 3.94 | 4.63 | |

| Y 5.07 | Sept 16 | 14.20 | 18.64 | 3.94 | 4.24 |

| Shanghai | April 16 | 13.88 | 16.33 | 5.70 | 3.43 |

| May 16 | 14.68 | 15.43 | 5.87 | 3.46 | |

| June 16 | 18.58 | 19.79 | 5.66 | 3.27 | |

| July 16 | 15.84 | 19.41 | 5.54 | 3.21 | |

| August 16 | 15.78 | 19.33 | 5.52 | 3.16 | |

| Sept 16 | 15.78 | 19.64 | 5.52 | 3.07 |