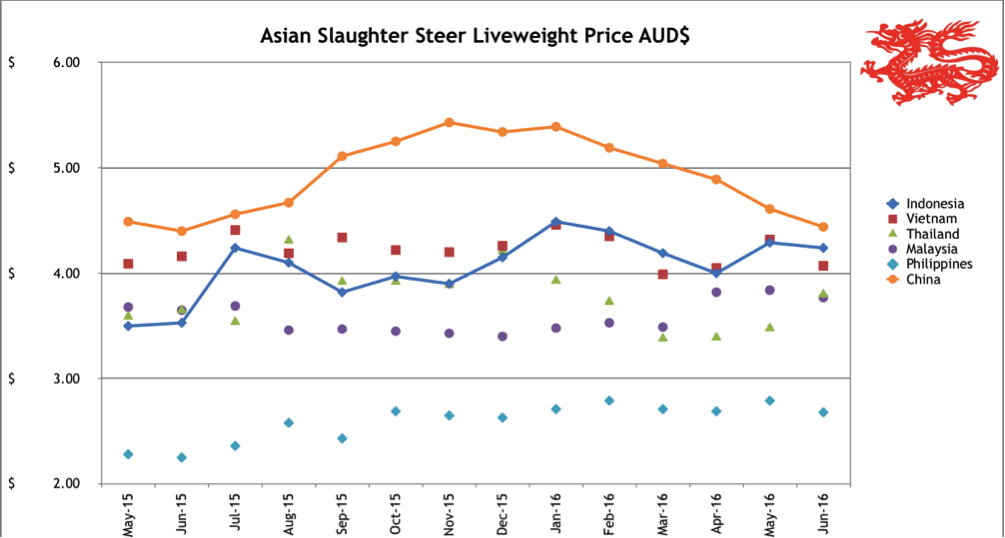

Indonesia: Slaughter Steers AUD $4.24/kg live weight (Rp9,900 = $1AUD)

Prices for slaughter cattle have been held steady at about Rp42,000 per kg following the very persuasive encouragement provided to importers by the Minister of Agriculture.

While this didn’t result in the Minister’s desired price of Rp80,000 per kg in the wet market, he was able to achieve his desired price for about 5,800 tons of frozen product which was “borrowed” from 10 of the larger processed beef importers in Jakarta and sold from government offices around the city.

In return, the importers have been offered quicker and easier processing of their next import permits in order to replace the product. This extraordinary action by the Minister was taken once it became clear that the importation of Indian buffalo beef (approved for importation on the 8th of June) would not arrive in time to supply the needs of Ramadan and Lebaran.

The extract of the Jakarta Post article below shows how and when this frozen product was to be distributed. I am told that despite the fact that the Jakarta Police station, National Police Headquarters, Trade Ministry Headquarters and other government offices were not exactly designed with frozen meat distribution in mind, the sales of meat did occur as planned.

Jakarta Post 21st June 2016

I followed wet market prices in both Jakarta and Bali (thanks to David Heath) over the month of Ramadan. The interesting finding is that changes in beef prices are modest while the movement in key household food items are dramatic. I am yet to understand why the government has such a strong public focus on beef prices while the prices of commodities like sugar, garlic and chilli can double or triple with little or no comment from anyone. See the table below showing the steep rises in daily staples that would seem to warrant political intervention well before beef is considered. Ramadan began on the 6th June and ended 6 July with the Lebaran holiday effectively continuing from the 6th to Monday the 11th July.

| Wet Market | 15th June | 22 June | 29 June | 5 July |

| Knuckle Jakarta | Rp130,000/kg | 130,000 | 135,000 | 135,000 |

| Beef in Bali | 95,000 | 105,000 | 105,000 | 95-100,000 |

| Jakarta chicken | 30,000 | 35,000 | 35,000 | |

| Bali chicken | 45,000 | 48,000 | 48,000 | 36,000 |

| Cooking oil | 8,000 Rp/ kg | 13,000 | 13,000 | 12,000 |

| Rice | 10,000 | 12,000 | 12,000 | 10,000 |

| Flour | 6,000 | 10,000 | 10,000 | 8,000 |

| Potato | 8,000 | 14,000 | 14,000 | 15,000 |

| Tomatoe | 3,000 | 7,000 | 10,000 | 8,000 |

| Carrots | 8,000 | 16,000 | 25,000 | 23,000 |

| Shallots | 20,000 | 32,000 | 30,000 | 35,000 |

| Chilli | 11,000 | 20,000 | 26,000 | 30,000 |

| Garlic | 5,000 | 35,000 | 32,000 | 32,000 |

| Onions | 22,000 | 40,000 | 40,000 | 40,000 |

| Sugar | 8,000 | 11,000 | 18,000 | 16,000 |

David Heath also followed the prices of live slaughter bulls selling from Bali’s main cattle market at Beringkit near Tabanan. Numbers were modest at around 100 head or less per week with medium bulls around the mid 3-400kg range selling for about Rp42,000 per kg live which is quite similar to the live rates for Aussie cattle in Jakarta. These bulls (all Bali cattle) were trucked to Surabaya where they would have been sold again to butchers for the Ramadan festival. The numbers of cattle presented in this market over the years has declined dramatically. 10 years ago the yard was full several days during the week with large numbers of heavy bulls, slaughter buffalo and breeders. Today a total of 200 head including breeders and slaughter cattle is a big day. It is now quite rare to see any buffalo at all as diesel powered hand tractors have taken their job.

Photo from David Heath: Beringkit cattle market Tabanan, Bali – mid Ramadan. The market is clearly “down in the calf pen”.

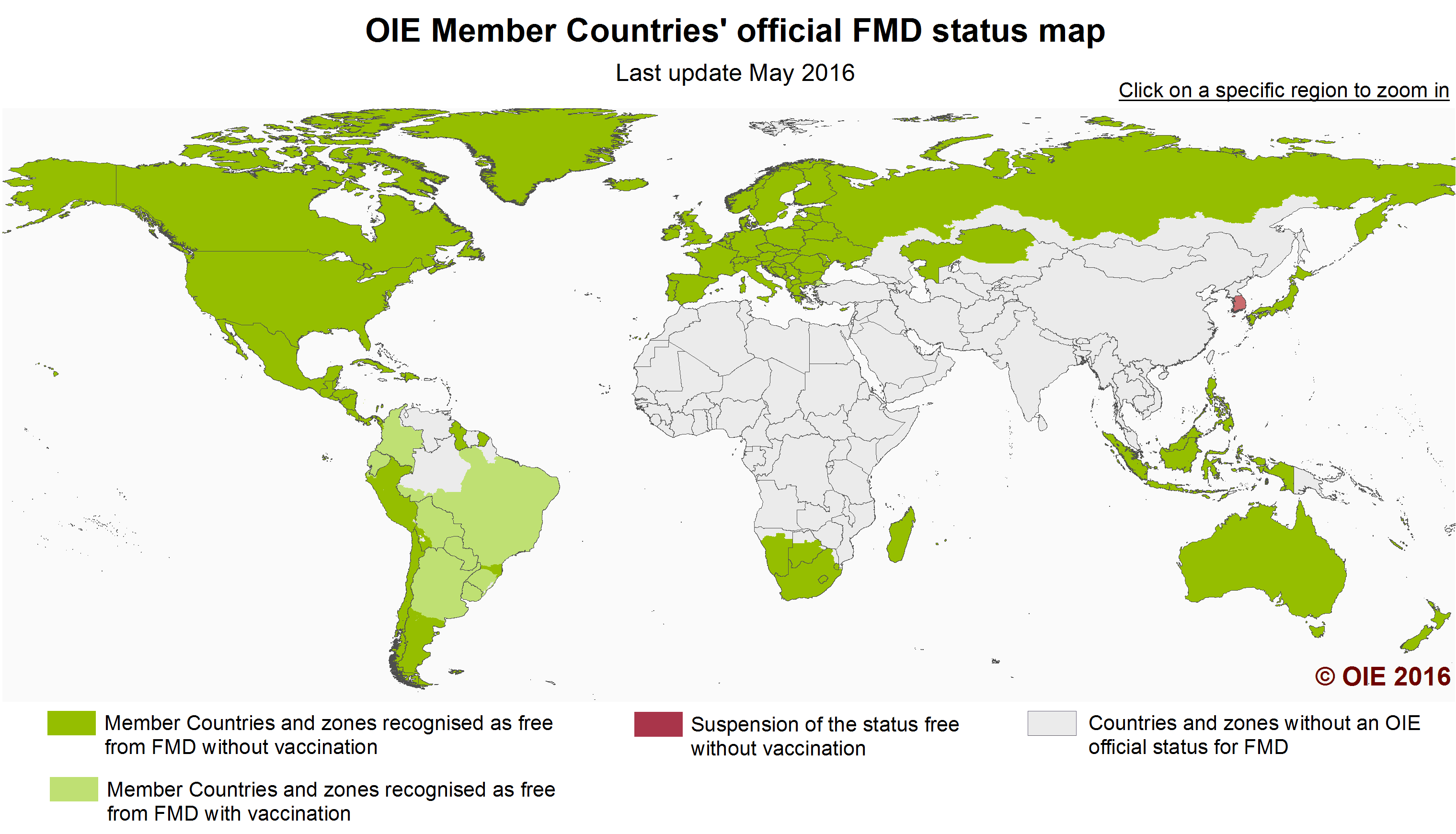

The historic news for this month of course is the issuing of permits for Indian buffalo beef to be imported from 10 approved abattoirs in various locations around India. This government policy is the most significant event in the Indonesian beef industry since the decision to allow importation of Australian feeder cattle in 1990. I intend to write a separate article regarding the impacts of this decision but in summary I expect that the medium term result will be a reduction in import demand for Australian live cattle to around 300,000 per year from calendar year 2017 onwards. Indonesian consumers will still require fresh meat for the wet markets so some Australian feeder cattle will still be fattened here while about half of the current market will be captured by Indian beef. The main destination of this frozen product will be the bakso ball (meat ball) market which is quite comfortable using frozen product. Buffalo beef is reputed to have excellent properties as a manufacturing base product so with an estimated 50% of all Australian wet market beef ending up as bakso balls today, this is likely to be the greatest area for substitution of demand.

By coincidence, the Medan Tribune newspaper reported that on the 13th of June, a unit of the Indonesian army seized about 8 tons of smuggled Indian buffalo meat from a domestic premises in Medan.

Photo from the Medan Tribun. Army officers seize smuggled Indian beef.

As I understand it from the press reports, the basis of the Indonesian government’s decision to import Indian beef is that it is importing meat only from abattoirs that slaughter cattle sourced from zones classified as free from FMD. The OIE is the world organisation governing international animal health issues and it has a web site which includes a summary of the FMD countries and zones recognised by them as free with and without vaccination. For some reason India or any regions/zones of India do not appear in any of these web site lists which identify the officially recognised free zones (see OIE FMD status map below). The data on the web site is stated to be updated by Resolution N° 16 (84th General Session of World Assembly, May 2016).

Vietnam: Slaughter Steers AUD $4.07 / kg (VND16,700 to $1AUD)

Rates remain similar to last month with the price decrease above only due to currency movements. The theme of the market remains oversupply with discounting by some of the larger feedlotters continuing to cause market difficulties for the rest of the importers. The numbers remaining in some of the larger feedlots are so great that this downward pressure on price through discounting is likely to be the main feature of the market for some months to come.

One very knowledgeable Vietnamese source has told me that the supply of cattle coming into Vietnam through Lao and Cambodia (primarily ex Thailand and Myanmar) are decreasing with prices rising accordingly. This reduction in supply from these traditional sources might work in the favour of the importers by offsetting the oversupply in some of the larger feedlots which could reduce the incentive for discounting.

The major event for the Vietnam trade in June was the exposure (on Australian TV) of shocking animal welfare practices in some Vietnamese abattoirs. While these abattoirs where not approved to receive Australian cattle, some of the cattle that were slaughtered in them appeared to be from Australia. The implication of this being that these cattle “leaked” from approved supply chains and found their way to non-approved facilities. The result has been a quick ban on some importers and some abattoirs followed by a detailed investigation of every Australian exporter sending cattle to Vietnam. This investigation is still underway so we won’t know the specific outcome for a few weeks yet at least. My sources suggest that it is quite possible that more importers and some exporters will be the subject of further sanctions by DAFF. The most severe sanction for an exporter is for their license to export to be revoked. In the event that some importers and some exporters are removed from the trade (at least in the short term) this will create both chaos and opportunities in the market. The Vietnamese press has provided significant coverage of these welfare issues involving Australian cattle.

I was in Vietnam last week and visited one of their major supermarket chains. As you can see from the photos below, the meat presentation is very well done with clearly marked displays of different levels of quality and type of product. In this area, the Vietnamese industry is way ahead of the Indonesian supermarket retailer presentation which would generally be given a mark of 3 to 4 out of a possible score of 10.

Locally slaughtered product (Grade 1) which in most cases will be sourced from Australian cattle slaughtered in Vietnam. Well presented & hygienic displays.

Grade 2 is for locally slaughtered offals and secondary cuts.

Absolutely no doubt of what it is and where it comes from.

Thailand: Slaughter Steers AUD $3.80 / kg (Baht 26.3 to $1AUD)

Local live cattle prices are firming slightly although I am not clear on the reasons for the improvement. There is some talk about the Mekong river trade into China slowly coming back on stream but this has not been confirmed. From Vietnam, the reports suggest that supply is drying up from Thailand causing the prices of imports from Thailand and Myanmar to rise sharply. The Thai government is also increasing their efforts to control Foot and Mouth Disease which has been causing serious problems for both breeders and fatteners.

Malaysia: Slaughter Steers AUD $3.77 per / kg (RM3.02 to $1 AUD)

Prices have moved a little mainly due to currency changes.

My agent in Malaysia reports on the price of frozen Indian buffalo beef knuckle which has been quite consistent at Rg17.50 per kg for many months. At today’s currency conversion rates, this translates to about AUD$5.79 or Rp57,320 per kg. If this retail price can be sustained in Malaysia then it seems highly likely that the Indonesian Minister’s wish for a price to the retail market of Rp80,000 per kg should be easily achieved.

My Malaysian agent also advises that their government has price restrictions in place for all food commodities during the Ramadan and Lebaran festival period to prevent excessive price spikes. This seems to make better sense than trying to control only one sector of the production system for the whole year without any consideration of the rest of the supply chain.

Philippines: Slaughter Cattle AUD $2.68 / kg (Peso 35 to AUD$1)

The currency has weakened a little now that the excitement of the new President is out of the way. Prices remain generally steady although recent rises of 2 Peso per litre for both diesel and petrol across the Philippines might cause some changes by next month. The new President has only just officially taken office so it will be interesting to watch his performance and see how this might affect the beef markets. As far as we are aware he doesn’t have the same intense focus on imported beef as his counterparts in Indonesia.

China: Slaughter Cattle AUD $4.44 / kg (RMB 4.95 = AUD$1)

Live cattle prices have remained fairly steady in both Beijing and Shanghai this month. In Beijing, the price ranged from Y20 to Y22, with Y20 offered for cull dairy cows while Y22 is offered for beef cattle breeds. The Shanghai price has eased a little further to Y16.2

Once again, I have used the figure of Y22 for this month’s graph price.

My Beijing agent advised that the recent slow reduction in cattle prices might be a reflection of lower feed cost following favourable harvests leading to the price of corn and soybean meal decreasing through 2016. In addition, he reports that there has been a significant lift in beef imports which is also putting downward pressure on prices especially in the supermarket. The agent also reports the following prices for cattle across a range of provinces in northern China :-

- Liaoning Province, >600kg, Simmental cattle, 23¥/kg.

- Heilongjiang Province, Simmental fattening cattle, 22.5 ¥/kg; Holstein fattening cattle, 20¥/kg.

- Jilin Province, Simmental fattening cattle, >400kg, 24 ¥/kg.

- Henan Province, fattening cattle, >600kg, 23 ¥/kg.

- Hebei Province, fattening cattle, >500kg, 22.5 23 ¥/kg.

Dairy farmers across China are experiencing the similar price reductions as our Aussie farmers with many small and medium farmers continuing to be forced out of the market with slaughter the only option for their surplus cows.

UK: spare a thought for the UK beef producer (and all their farmers).

Beef and sheep producers in the UK were already experiencing a lot of pain with weak prices across the board. These weak rates were offset to a limited extent by the various subsidies and incentives received from the EU including zero tariff exports.

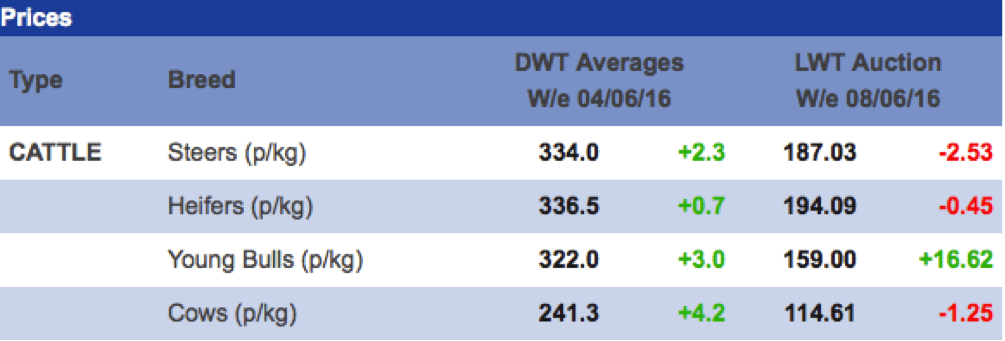

With Britain now leaving the EU, the picture is grimmer than ever with some of the less efficient farmers likely to come under great pressure to exit the industry. See below a table taken from the Quality Meat Scotland (QMS) website news of June 13th 2016:

Using the new Brexit British pound exchange rate of AUD$1 being worth 58.3 pence, the price above for Scottish slaughter steers is equivalent to AUD$3.20 per kg live weight. Knowing that British farmers have higher costs of land and inputs for their production, $3.20 is a rather poor price for first class cattle.

Britain is a net importer of meat (of all types) with 80% of this product sourced from the EU. Brexit means that zero tariff trade with the EU will end which is expected to result in an increase in the cost of all imported products. Exports to the EU will also be subject to tariffs’ in the future so this is likely to further reduce returns to farmers in the medium term.

Uncertainty always depresses markets so the meat industry in the UK looks to be in for at least 2 years of volatility before the future trading position becomes a little clearer. The only positive affect for exporters so far has been the collapse of the Pound Sterling.

Beef Central’s Dr Ross Ainsworth will be speaking at the upcoming BeefEX feedlot industry conference on the Gold Coast in October. Click here to access a preview. Dr Ainsworth’s monthly South East Asian reports are first published exclusively on Beef Central. To view previous Beef Central articles click here. To visit his personal South East Asia report blog site, click here.

Market price table for June 2016

(All prices converted to AUD)

These figures are converted to AUD$ from their respective currencies which are changing every day so the actual prices here are corrupted slightly by constant foreign exchange fluctuations. The AUD$ figures presented below should be regarded as reliable trends rather than exact individual prices. Where possible the meat cut used for pricing in the wet and supermarket is Knuckle/Round.

| Location | Date | Wet Market

AUD$/kg |

Super market

$/kg |

Broiler chicken

$/kg |

Live Steer

Slaughter Wt AUD$/kg |

| Jakarta | Jan 2016 | 13.26 | 16.32 | 3.26 | 4.49 |

| Feb 2016 | 12.95 | 19.69 | 2.90 | 4.40 | |

| March 16 | 12.83 | 18.18 | 2.93 | 4.19 | |

| April 16 | 13.00 | 18.20 | 2.90 | 4.00 | |

| May 16 | 13.27 | 18.57 | 3.06 | 4.29 | |

| June 16 | 13.63 | 18.89 | 3.54 | 4.24 | |

| Medan | Jan 2016 | 12.24 | 10.61 | 2.45 | 4.29 |

| Feb 2016 | 11.92 | 10.36 | 2.54 | 4.14 | |

| March 16 | 11.11 | 10.50 | 2.12 | 4.49 | |

| April 16 | 12.00 | 10.40 | 1.70 | 4.40 | |

| May 16 | 11.73 | 12.24 | 4.59 | 4.49 | |

| June 16 | 11.11 | 11.11 | 2.42 | 4.44 | |

| Philippines | Jan 2016 | 7.53 | 7.23 | 3.70 | 2.71 |

| Feb 2016 | 8.24 | 7.50 | 3.82 | 2.76 | |

| March 16 | 8.00 | 7.28 | 3.57 | 2.71 | |

| April 16 | 7.93 | 7.50 | 3.39 | 2.69 | |

| May 16 | 8.38 | 8.23 | 3.38 | 2.79 | |

| June 16 | 8.14 | 7.43 | 3.43 | 2.68 | |

| Thailand | Jan 2016 | 9.84 | 11.02 | 2.76 | 3.93 |

| Feb 2016 | 9.02 | 10.98 | 2.75 | 3.73 | |

| March 16 | 9.39 | 10.52 | 2.63 | 3.38 | |

| April 16 | 9.06 | 10.57 | 2.64 | 3.39 | |

| May 16 | 9.27 | 10.81 | 2.70 | 3.48 | |

| June 16 | 8.74 | 10.65 | 2.66 | 3.80 | |

| Malaysia | Jan 2016 | 9.18 5.83 | 11.47 | 2.13 | 3.48 |

| Feb 2016 | 10.00 5.74 | 11.67 | 2.17 | 3.53 | |

| March 16 | 9.90 5.78 | 11.55 | 1.91 | 3.49 | |

| April 16 | 10.06 5.87 | 11.74 | 1.85 | 3.82 | |

| May 16 | 10.10 5.89 | 11.78 | 2.02 | 3.84 | |

| June 16 | 9.93 5.79 | 8.94 | 2.48 | 3.77 | |

| Vietnam | Jan 2016 | 15.82 | 17.72 | 8.86 | 4.46 |

| HCM City | Feb 2016 | 15.52 | 17.39 | 8.07 | 4.34 |

| March 16 | 14.88 | 16.66 | 7.74 | 3.99 | |

| April 16 | 14.88 | 16.67 | 7.74 | 4.05 | |

| May 16 | 15.43 | 17.28 | 7.41 | 4.32 | |

| June 16 | 14.97 | 16.77 | 7.19 | 4.07 | |

| China | Jan 2016 | 15.86 | 19.91 | 4.35 | 5.39 |

| Beijing | Feb 2016 | 15.11 | 19.49 | 4.26 | 5.19 |

| March 16 | 14.23 | 18.61 | 4.07 | 5.04 | |

| April 16 | 14.28 | 18.69 | 4.08 | 4.89 | |

| May 16 | 14.26 | 19.20 | 4.19 | 4.61 | |

| June 16 | 13.73 | 18.50 | 4.04 | 4.44 | |

| Shanghai | Jan 2016 | 19.56 | 21.73 | 6.09 | 3.91 |

| Feb 2016 | 17.87 | 21.70 | 5.96 | 3.72 | |

| March 16 | 14.63 | 18.21 | 5.69 | 3.45 | |

| April 16 | 13.88 | 16.33 | 5.70 | 3.43 | |

| May 16 | 14.68 | 15.43 | 5.87 | 3.46 | |

| June 16 | 18.58 | 19.79 | 5.66 | 3.27 |