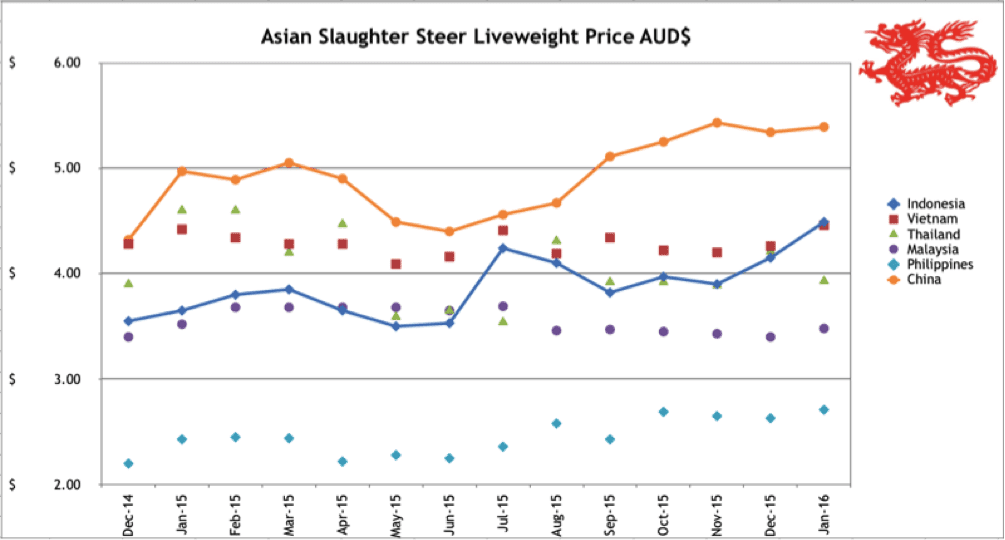

Indonesia: Slaughter Steers AUD $4.49/kg live weight (Rp9,800 = $1AUD)

The ongoing shortage of slaughter cattle supplies following on from the very low import permit allocations in Q3 2015 has kept live prices up again to around Rp44,000 (excluding GST).

The weakening AUD makes the price rise look even higher than it is locally. There were signs however that by the end of January supplies were improving and price pressure was changing from upward to downward.

There is no other way to describe the current regulatory and commercial environment in the Indonesian beef industry but total chaos. While the government continues to claim that its aim is to reduce the price of beef (and other foods) to domestic consumers, it somehow manages to deliver a seemingly endless stream of policies that have precisely the opposite effect:

- The 2016 Import Permits for feeder cattle were officially announced at the beginning of January 2016 as expected, but what isn’t widely known is that the actual documentation was not provided to importers at that time but took from 7 to 14 days or more to be finally delivered. This hard copy of the Import Permit must be sighted by the Australian Government before they will allow a shipment to be exported from Australia so once again shipping was held up in Australian ports waiting for documents for up to 2 weeks. Not only does this cost the exporter dumurrage fees (waiting charges with the ship’s meter running) but it means that those two weeks are lost forever to the capacity of shipping to delivery potential numbers for the year. The result is that annual shipping costs will be greater than they needed to be on an annual per head basis. Naturally this additional cost of freight is passed on first to the exporter, then eventually to the importer, the Indonesian butcher and finally to the Indonesian customer.

- As advised by the Indonesian government at the end of 2015, permits would be issued on both an annual total and 4 monthly split basis to provide industry with additional certainty and flexibility to plan for their future commitments. Let’s call them T1, T2 and T3 permit allocations. When the T1 permits were finally received by the importers in mid-January they discovered that they were in fact written on the old documentation which refers to Quarterly permit allocations which in this case terminate at the end of March 2016. This means that the T1 permit allocation did not allow any animals to be imported after the end of March unless the documentation was changed to include April. This has now been done but it took quite a while and added considerable difficulties to those in the trade trying to plan for April activities.

- As one importer explained it to me, there were two bombs let off on January the 14th, one in Jalan Thamrin by ISIS terrorists and one by the tax department when they advised that a new 10% PPN tax (GST) was to be added to live feeder cattle and back dated until the 8th. This new GST tax also covered other live animals including chickens, goats, sheep and pigs. AND the Indonesian Department of Agriculture knew nothing about it! Chaos once again as importers (and the food industry at large) tried to contact the appropriate agencies to find out what on earth was going on. And there was no similar tax on imported beef! Eventually when this new tax was confirmed in writing and cattle importers commenced charging their customers the 10% PPN (and presumably all other live animal traders) there was a ground swell of protest around Indonesia which culminated in the Indonesian Co-ordinating Minister announcing that the tax would be cancelled. But, the tax is officially in force until it is officially rescinded and as of the end of January this had not occurred. As a result some importers have been charging their customers the 10% PPN with the understanding that should the tax be rescinded as advised by the Minister then they would get a refund while some importers are not charging it and taking the risk themselves. I have no idea how this is dealt with by the butchers and meat traders when they make their sales but it must be a mess.

- The Indonesian Ministry of Transport has commissioned the building of two new cattle ships, the Camara Nusantara 1 with a capacity of about 500 head and another which is still being completed. The purpose of these vessels is to provide a government subsidised sea-freight service to facilitate the efficient flow of live slaughter cattle from the Eastern Islands to Java to “beef up” the supplies of cattle in the main areas of consumption in order to support the efforts to reduce prices to consumers. During the first voyage in December 2015, traders were unable to fill the vessel as the price they were prepared to offer was not attractive enough to the Eastern Islands suppliers. My advice is that the second voyage has not been a great success either. I have spoken to many local buyers of domestic cattle from the Eastern Islands and they all confirm that the main problem is that there are so few cattle left in the islands that it will be extremely difficult to consistently fill these vessels regardless of the prices offered. As an indication, David Heath advises that this week’s price of Bali cattle bulls at the Beringkit live cattle market in Bali is Rp43 to 44,000 per kg live weight in the market place which would imply that the price landed into East Java would be at least Rp46k or a lot more if the destination was West Java.

- The Indonesian government is now publicly announcing that it is actively investigating and promoting the importation of Indian buffalo beef with the aim of reducing domestic beef prices. While this is one potential solution to the problem of retail beef prices, it also introduced a large number of potential complications for the industry and the government itself. Firstly, when this proposal has been raised by government in the past, aggressive farmer opposition has ensured that it has been defeated in the courts. If it were to go ahead, large volumes of legislation would need to be changed, eliminated and created as currently this importation is illegal. If we consider the time it takes to change the simple wording on an import permit and translate that to a massive change to a vast array of complex legislative instruments combined with a background of vigorous opposition from the very powerful cattle farmer lobby across Indonesia then it seems like the consumer is being promised something that might not be delivered in the short to medium term if ever. In addition, Indian buffalo beef is all frozen and there is an extreme distrust of all frozen beef products in the wet markets which will require a massive re-education process and significant discounting to achieve widespread uptake of the buffalo beef product.

- The Indonesian government legal action against the majority of cattle importers for alleged withholding of slaughter cattle in order to artificially raise prices continues.

Vietnam: Slaughter Steers AUD $4.46 / kg (VND15,800 to $1AUD)

Prices have risen a little in the south and a lot in the north. HCM quotes range from 69,000 to 72,000 Dong per kg live weight while Hanoi prices range from 73 to 76,000 Dong. In both cases my advice is that a combination of the cold weather and improved feeding has tended to reduce carcase fat with buyers happy to pay more for higher yielding animals. The currency has also strengthened against the AUD pushing the A$ price to a new high. Vietnam’s lunar New Year celebrations of Tet are also coming up in the second week of February and this traditionally increases demand and prices across the board.

On the 31st of December the Vietnamese government reduced the import tax on all live cattle (breeder/feeder/slaughter) from 5% to zero which should give importers a nice jump in future profitability as a Tet holiday gift.

During this month, a small number of Australian feeder cattle were confirmed to be infected with Foot and Mouth Disease (FMD) in a limited number of feedlots from north to central Vietnam. Remarkably, despite zero immunity in most cases, the Australian feeders suffered only mild symptoms and generally recovered uneventfully after a short period with mouth lesions and some mild lameness. Spread amongst the Australian cattle was slow and limited to low numbers in each group. Many of the infected cattle were not previously vaccinated although all animals in the affected facilities were quickly vaccinated once the diagnosis was confirmed. Vaccination protocols vary between importers with some routinely vaccinating all animals on arrival and some only bothering if a risk appears. Thankfully, the capacity for the spread of FMD in susceptible cattle in the Vietnam environment appears to be dramatically less than in temperate areas like Europe.

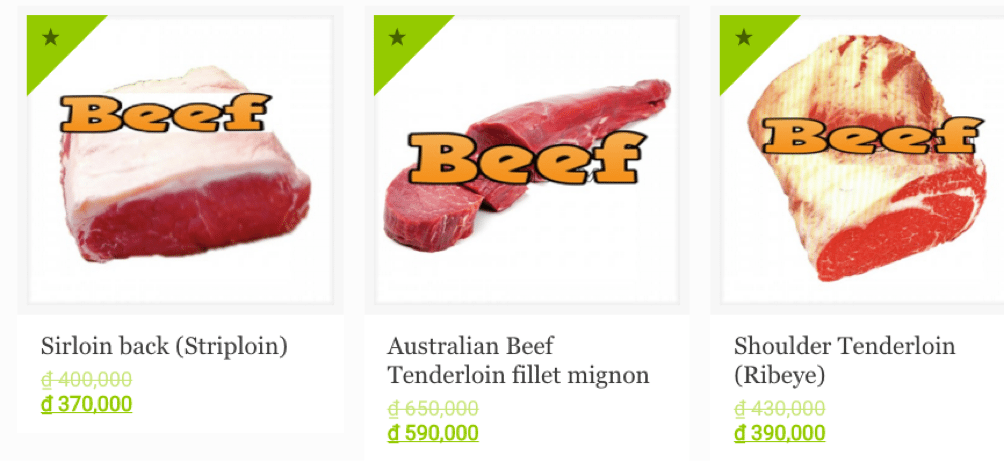

Meat sales across the internet in Vietnam appear to be gaining popularity including local, USA and Australian product available for home delivery. See prices in this internet advertisement below.

AUD$23.41 per kg AUD$37.34 AUD$24.68

Thailand: Slaughter Steers AUD $3.93 / kg (Baht 25.4 to $1AUD)

Prices remain subdued at about Bht100 per kg live weight for domestic slaughter as the export trade to China continues to be restricted.

The only reason that the price has changed above is the Baht has strengthened against the AUD. Given this trading environment there is very little chance of future imports of live feeder or slaughter cattle from Australia until the fundamentals change to once again provide a useful margin for importers. The Thai government continues to investigate their options for live imports from alternative countries.

Malaysia: Slaughter Steers AUD $3.48 per / kg (RM3.05 to $1 AUD)

The Malaysian currency actually strengthened against the AUD this month while live cattle and beef prices remained static. The net effect on the quoted AUD price above is a small rise.

Philippines: Slaughter Cattle AUD $2.71 / kg (Peso 33.2)

Little change in the Philippines which is extremely good considering that means a continued run of good seasons and stable politics. The peso has strengthened against the AUD which is the only reason that the cattle price has risen above.

China: Slaughter Cattle AUD $5.39 / kg (RMB 4.60 = AUD$1)

The cold weather, beef eating winter season this year coincides with Chinese New Year (8th February) resulting in slightly higher retail prices across all recorded categories. Live prices in Beijing and Shanghai are fairly steady at Y24.8 and Y18 per kg live weight respectively.

Insiders tell me that the preparations for ramping up of live cattle imports from Australia to China are progressing at a snails pace as a result of a great deal of bureaucratic confusion and miscommunication relating to the complex ESCAS requirements and many other regulatory issues. The massive Chinese demand will no doubt eventually translate into greater imports of live cattle but it doesn’t look like there will be any significant numbers traded for perhaps 6 to 12 months at least. The vast array of very detailed regulations associated with live imports from Australia ensures that authorities can micro-manage every aspect of the imported cattle supply chain from where and how long they are in quarantine to when and how they can be slaughtered. Restrictions on the mixing of imported cattle make the business environment particularly difficult as multiple facilities are needed to hold separate shipments of stock to prevent them from contacting each other. Hopefully, the authorities will finally discover that most of these restrictions serve no purpose in terms of risk management of imported livestock and revert back to workable protocols.

Laos: Wet market beef prices AUD $13.66 per kg (1 AUD$ = 5,710 Lao Kip)

During a visit to southern Lao last month I took this photo in a provincial town wet market. There were only a few beef stalls with the majority of meat on offer chicken and pork. The ladies on the stall advised that some of the beef on display was from buffalo and this was priced at almost 10% more than cattle beef. Considering the very low average incomes of Lao workers this represents close to the highest price of beef in S E Asia in terms of average daily spending power.

The beef (and buffalo) section at the Pakse wet market, southern Laos.

Dr Ross Ainsworth’s monthly South East Asian reports are first published exclusively on Beef Central. To view more of Dr Ainsworth’s previous Beef Central articles click here. To visit his personal South East Asia report blog site, click here.

Market price table for January 2016

(All prices converted to AUD)

These figures are converted to AUD$ from their respective currencies which are changing every day so the actual prices here are corrupted slightly by constant foreign exchange fluctuations. The AUD$ figures presented below should be regarded as reliable trends rather than exact individual prices. Where possible the meat cut used for pricing in the wet and supermarket is Knuckle/Round.

| Location | Date | Wet Market

AUD$/kg |

Super market

$/kg |

Broiler chicken

$/kg |

Live Steer

Slaughter Wt AUD$/kg |

| Jakarta | August 2015 | 13.00 | 19.00 | 2.70 | 4.10 |

| Sept 2015 | 12.75 | 18.63 | 2.64 | 3.82 | |

| October 15 | 13.27 | 16.32 | 2.85 | 3.98 | |

| Nov 15 | 13.00 | 19.00 | 3.00 | 3.90 | |

| Dec 15 | 13.00 | 19.00 | 3.50 | 4.15 | |

| Jan 2016 | 13.26 | 16.32 | 3.26 | 4.49 | |

| Medan | August 2015 | 11.50 | 11.50 | 2.60 | 4.20 |

| Sept 2015 | 9.80 | 10.98 | 2.64 | 3.92 | |

| October 15 | 11.73 | 12.24 | 2.65 | 4.08 | |

| Nov 15 | 10.50 | 11.00 | 3.30 | 3.70 | |

| Dec 15 | 10.00 | 11.00 | 2.20 | 4.10 | |

| Jan 2016 | 12.24 | 10.61 | 2.45 | 4.29 | |

| Philippines | August 2015 | 6.30 | 6.76 | 3.69 | 2.58 |

| Sept 2015 | 6.33 | 6.91 | 3.73 | 2.43 | |

| October 15 | 6.29 | 6.77 | 3.67 | 2.69 | |

| Nov 15 | 6.47 | 6.88 | 3.61 | 2.65 | |

| Dec 15 | 6.90 | 7.02 | 3.65 | 2.63 | |

| Jan 2016 | 7.53 | 7.23 | 3.70 | 2.71 | |

| Thailand | August 2015 | 9.02 | 10.98 | 2.75 | 4.31 |

| Sept 2015 | 9.41 | 10.98 | 2.75 | 3.92 | |

| October 15 | 9.41 | 10.98 | 2.75 | 3.92 | |

| Nov 15 | 9.34 | 10.89 | 2.72 | 3.89 | |

| Dec 15 | 9.19 | 10.73 | 2.68 | 4.21 | |

| Jan 2016 | 9.84 | 11.02 | 2.76 | 3.93 | |

| Malaysia | August 2015 | 9.33 | 11.66 | 2.40 | 3.46 |

| Sept 2015 | 9.18 | 11.80 | 2.36 | 3.47 | |

| October 15 | 9.12 | 11.72 | 2.25 | 3.45 | |

| Nov 15 | 9.06 | 11.33 | 1.78 | 3.43 | |

| Dec 15 | 9.00 | 11.25 | 1.99 | 3.40 | |

| Jan 2016 | 9.18 | 11.47 | 2.13 | 3.48 | |

| Vietnam | August 2015 | 15.63 | 17.50 | 8.13 | 4.19 |

| HCM City | Sept 2015 | 15.72 | 17.61 | 8.18 | 4.34 |

| October 15 | 15.53 | 17.39 | 8.07 | 4.22 | |

| Nov 15 | 15.43 | 17.28 | 7.41 | 4.20 | |

| Dec 15 | 15.43 | 17.28 | 7.40 | 4.26 | |

| Jan 2016 | 15.82 | 77.72 | 8.86 | 4.46 | |

| China | August 2015 | 15.55 | 17.69 | 4.44 | 4.67 |

| Beijing | Sept 2015 | 15.56 | 17.69 | 4.44 | 5.11 |

| October 15 | 15.32 | 19.69 | 4.38 | 5.25 | |

| Nov 15 | 15.22 | 21.65 | 4.34 | 5.43 | |

| Dec 15 | 15.38 | 19.57 | 4.27 | 5.34 | |

| Jan 2016 | 15.86 | 19.91 | 4.35 | 5.39 | |

| Shanghai | August 2015 | 20.00 | 21.33 | 5.33 | 3.55 |

| Sept 2015 | 20.00 | 21.78 | 5.33 | 3.78 | |

| October 15 | 19.69 | 21.44 | 6.13 | 3.83 | |

| Nov 15 | 19.56 | 20.87 | 5.65 | 3.80 | |

| Dec 15 | 18.37 | 20.94 | 5.98 | 3.84 | |

| Jan 2016 | 19.56 | 21.73 | 6.09 | 3.91 |