AUSTRALIAN livestock exporters are currently negotiating with their importing customers in the United States to send feeder cattle across the Pacific to be grain-finished in their southwestern feedlots.

There are still a number of administrative issues to resolve including some sticking points with the health protocol but these are expected to be sorted out with time, goodwill and the assistance of the very strong mutual benefits associated with this prospective trade.

The US is after feeder cattle similar to the Indonesian weight specifications and may take a wide range of genetics from Brahmans to British breeds.

The spectacular collapse of the US cattle herd has been well-reported during the last few years and it has now reached the point where their usual sources of live cattle imports from Canada, Mexico and Hawaii are simply not enough to top up their domestic production of feeders to keep their feedlot sector fully occupied.

With the A$ in the mid US70c region, US lotfeeders are paying the equivalent of A$6.60 per kg live weight for feeders. These high prices are driven by a combination of reduced cattle supplies due to their shrinking cow herd, solid retail beef demand, under-utilised feedlot space and cattle ration prices that are the lowest for five years.

Some of the big Mexican cattle feeders who previously supplied live cattle to the US are now utilising their cheaper production and slaughter costs to process inside Mexico, sending some of the beef into the US and marketing the remaining secondary products and offals at home.

More Canadian-born calves are also being fed and processed in Canada leaving fewer numbers for US feedlots.

Australia simply has some of the cheapest land in the world, much of it suitable only for breeding cattle combined with a stable business and social environment and a squeaky-clean disease status that allows our live cattle to travel freely, virtually anywhere on the planet.

Some of the highest processing costs in the world and a small domestic market conspire to provide a powerful incentive to export cattle live. Brazil has millions of handy feeder cattle quite close to the US, but a Foot and Mouth Disease status that makes live cattle exports to the US absolutely out of the question.

Live exports could pass 2.5 million head within 3 years

Given the strong prospects of the entry of both China and the US into the Australian live cattle market, it is quite possible that exports could reach a figure in the order of 2.5 million head per annum within the next three years.

This will imply a tectonic shift in the Australian beef industry as traditional lotfeeding and meat processing supply chains will be heavily impacted while the focus of demand will be forced back down the line to producers who will sell directly to the live cattle exporter.

This surge of demand for live exports may well be offset by an easing in demand for frozen product, as Asian customers replace imported boxed beef with live cattle that allow them to add value using their agricultural waste products as cheap sources of feed and their much cheaper and efficient processing sector.

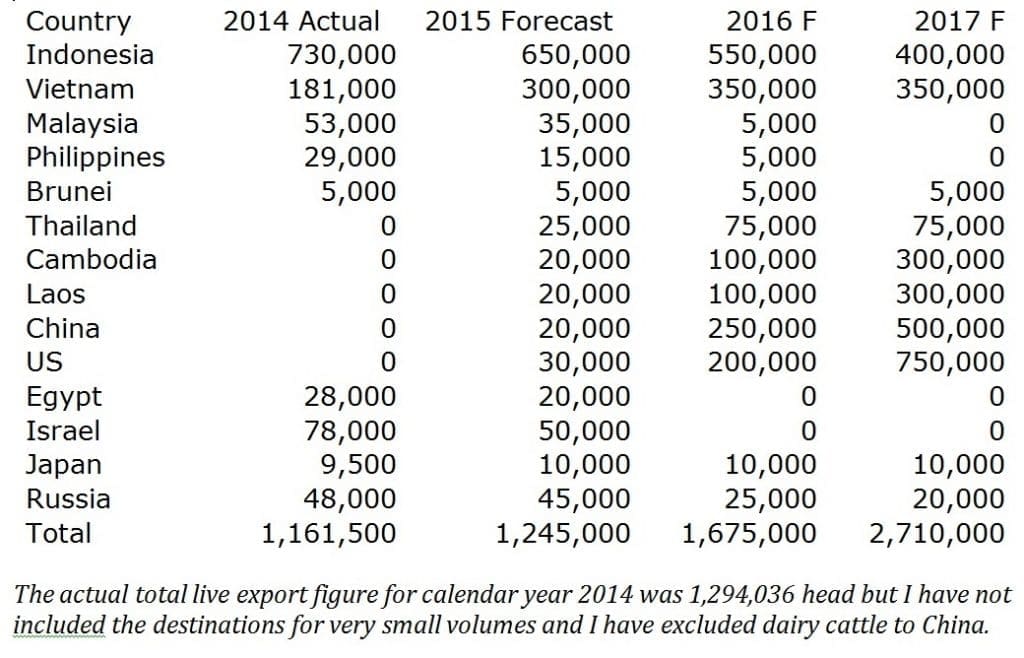

The table below presents an optimist’s view of the current and possible future live beef cattle exports to Australia’s major importing destinations:

China is in a slightly similar position to the US in which its domestic herd has been decimated, leaving its feedlot and processing sectors with under-utilised capacity.

The pressure to open the trade is more political compared to the US where the opening of the market will most likely be based on primarily commercial considerations. The end result is still likely to be the same, however, as they are both desperately short of cattle and will begin imports when they are good and ready i.e. soon.

‘Soon’ might mean three months or one year, but probably not much more, in my opinion.

The significant difference in the case of China is that they will be primarily interested in finished cattle as their own existing cattle production systems (including 14 million dairy and 60 million beef cattle) are currently utilising the bulk of their domestic ruminant feed resources and they don’t want to place any further strain on the system by feeding additional imported cattle for extended periods.

The higher prices that are likely to be generated by these two new markets will probably cause our current live cattle importers to back off to varying degrees but the net export volumes should still represent a massive increase in total numbers.

Cambodia and Laos will effectively be operating as the back paddock for Vietnam and in the medium-term, China. Cambodia is currently constructing at least two very large international standard abattoirs while equivalent facilities in Laos are only in the planning stages.

High-performance feedlots and abattoirs on low-cost land, with low-cost feed and the low-cost labour environments of Cambodia and Laos have the potential to develop into a major new “silk road” for the entry of processed beef from Australian-sourced cattle into China via its south east Asian neighbours.

Thai importers are most likely aiming to replace their local cattle supplies with Australian cattle rather than process them for re-export.

Shipping capacity

The primary restriction for all this expansion will be shipping space which needs several years to build and deliver additional capacity.

The long transit time across the Pacific to the west and south coasts of the US will effectively reduce the annual live export capacity of the existing fleet so a significant number of new and very large ships will be required to meet the forecasts above.

Live shipments to the US have the options of discharging near San Francisco or onto the Texas coast after transiting the Panama Canal, the Caribbean and the Gulf of Mexico. The additional time to transit via Panama will make the delivery time to Texas frustratingly slow.

The building of additional shipping capacity is another story in itself, but I do know that there are some new ships in dry-dock but probably not enough at this stage to support a possible live export volume of 2.5+ million head within three years.

This monthly market report is first published exclusively on Beef Central. To view more of Dr Ross Ainsworth’s previous articles on South East Asia,click here to view archived articles on Beef Central, and here to visit his personal South East Asia blog site.