110th Edition: March 2023

Key Points:

- Indonesian market slow in lead up to Ramadan and Lebaran with 100,000 ton frozen import quotas confirmed for both India and Brazil

- Vietnam market remains slow, especially without Chinese tourists

The South East Asian markets are still adapting to a new trading ‘normal’, which has been created by various key impacts in the region.

Across the entire region, the limiting factor for live export has shifted from the high prices of Australian cattle to low consumer demand for local slaughter.

This shift in consumer behaviour is a result of equally the COVID pandemic, which has led to changes in the use of some fresh products, and the impact of animal diseases, which continue to disrupt normal import and feedlot operations.

Irrespective of the lowering of prices of Australian cattle, the feedlots face a significant risk due to the larger numbers needed to fill a shipment. Slow sales, disease outbreaks, or further price drops would create additional challenges for feedlots.

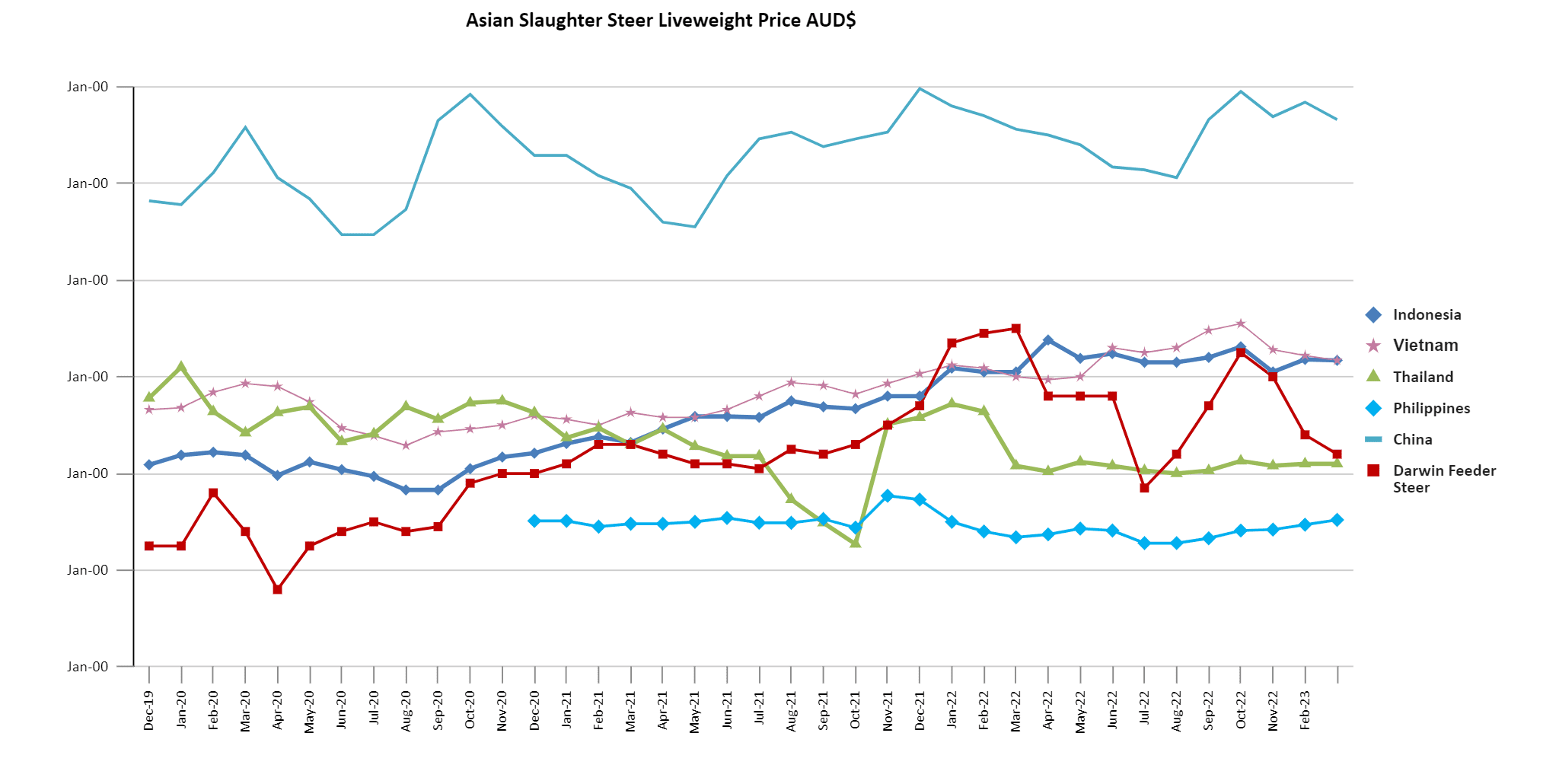

Indonesia: Steers AUD $5.17 / kg live weight (Rp10,245 = 1AUD)

Ramadan starts in Indonesia on the evening of March 22 and lasts until 21st April for Lebaran (Eid al-fitr).

Usually we see cattle prices start to increase in the lead up to this period, but the market is remaining stable at around Rp53,600 (AUD$5.17) which indicates that the live slaughter trade may remain slow.

The price of fresh beef in the market is 136,000 Rb/kg ($13.30) in wet markets and 176 Rb/kg ($16.83) in supermarkets.

The beef market is looking increasingly crowded for locally processed cattle, as prices remain relatively high and the government continues to look for ways of securing affordable beef in preparation for the festive period. Indonesia is a high consumer of processed or manufactured beef rather than whole beef products making it more open to substitution with cheaper alternatives such as Indian Buffalo Meat (IBM).

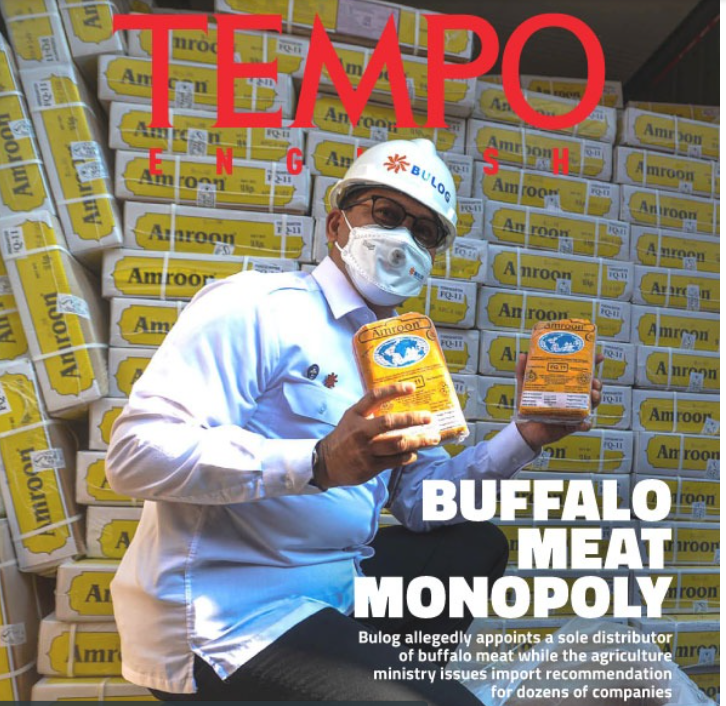

In 2016 IBM was introduced to the Indonesian market with the intention of reducing the price of beef. At that time the regulations limited import of IBM to State Owned Enterprises (SOE) and the state logistics agency Bulog was put in charge of import. From November 2022 a new regulation was put in place that created the potential for private imports of IBM. On the 25th January Bulog received a quota for 100,000 tons for 2023, and 100,000 tons of Brazilian beef was awarded to ID Food, another Indonesian state-owned food holding company. This has essentially left no room for imports from private companies and facilitated the retention of monopoly supplies. What makes the story more concerning is that the distribution has been left to one company, Suri Nusantara Jaya, with all requests made to Bulog from vendors and distributors forced to go through Suri. This seems to have resulted in Bulog and Suri making what mathematically looks like significant profit from the trade, especially as from 2017-2021 the listed prices of IBM were around Rb56,000 for Bulog and Rb85,000 for Suri. What was intended as a support for the poor has resulted in profit for the powerful. For those that want to read more about the players in the Buffalo trade I suggest you follow the link to the expose in Tempo magazine.

Tempo magazine front page looking at the monopoly of the buffalo trade in Indonesia. IBM was intended to help the poor.

FMD and LSD continue to move through the country and there are ongoing unofficial reports of it moving between islands. LSD infections appear to remain under-reported given the anecdotal information I have from several sources on the ground, especially in Central Java and Yogyakarta where there are many new infections of local cattle.

MLA has an ongoing project run by Ausvet that is supporting Indonesian feedlots to improve their biosecurity. Preliminary site risk assessment and consultation has found:

- The inappropriate use of disinfectant is common across many feedlots, including spraying or misting disinfectant into the air or onto live animals. This is not only an expensive procedure, but also ineffective. Disinfection should only take place once a pen has been thoroughly cleaned and contains no live animals. Disinfecting the air, live animals or pens that have not been cleaned is unlikely to be effective in controlling disease.

- In many feedlots, the highest biosecurity risks come from the entry of dirty trucks that then make contact with clean vehicles or animal pens. It is important that trucks are properly cleaned and disinfected before entering a property and then their contact with clean vehicles or pens containing live animals are limited.

- Most of the feedlots have already experienced at least one outbreak of FMD. This can help explain why there is general hesitation of some importers to restock with Australian cattle, even as prices begin to drop.

- Lack of supply of Australian feedlots will likely result in mixing of Australian and local cattle in the same facilities. We are seeing a similar story in Vietnam where low volumes of Australian cattle are resulting in more locally sourced cattle in the same facility to utilise the investment. Mixing Australian cattle with local breeds comes with the risk of disease because even Australian cattle vaccinated for FMD on arrival will take some time to develop immunity.

- There remain some vaccine supply and distribution issues, especially related to smallholders and LSD. The LSD vaccines that are available can cause vaccine site reactions that resemble infection (Neethling response). This creates obvious concerns for the farmers vaccinating their cattle and also increases risks involved in funding or running vaccination programs as farmers could make claims following vaccine reaction, and it remains unclear who would pay the compensation in these cases?

FMD vaccination has reached 11.994mil doses administered with the majority of infections being seen in the western islands of Smartra and Java. There has been no official reports of FMD cases further east than Southeast Sulawesi.

Data on infections and vaccination rates for FMD in Indonesia is freely available through the government site https://crisiscenterpmk.ditjenpkh.pertanian.go.id/?l=en

Vietnam: Steers AUD $5.17 (15,938 VND = 1AUD$)

The situation in Vietnam for live export does not look to improve quickly, as the market resets to a new normal. We are unlikely to ever see a return to numbers over 200,000 head per year that were possible pre-COVID.

The price into abattoirs is currently sitting at 84,000 VND/kg (AUD $5.30) and 82,000 VND/kg (AUD $5.17) for Australian bulls and steers respectively although there are now very few steers in feedlots. Thai bulls are receiving 86,000 VND/kg (AUD5.42) although due to movement restrictions across the Laos border there are few currently in Vietnam. The lack of supply of live animals has been compensated by Vietnamese buffalo backfilling into the Vietnamese market, these animals would normally move into China. The price of knuckle remains constant at around 200,000 VND/kg in traditional markets and 285,000 VND/kg in modern retail.

It was only a few years ago that my first line about Vietnam would have described their reliance on fresh (slaughtered the night before) meat as the reason Australian live cattle had a place in the market. After visiting both Hanoi and HCMC last week it is clear that frozen beef appears to now be playing a significant role in all parts of the market. The changes were already slowly happening in Vietnam but this has been significantly accelerated due to lockdowns and supply chain disruptions that existed over COVID. The frozen beef and pork that was perceived by consumers to be the meat not purchased in the market yesterday, is now accepted as consistent, cheaper, easier to use, has a longer shelf life, and in many cases tastes better. It will be a challenge for the local processing sector to return to previous volumes and the Australian cattle supply numbers reflect that.

Lotte Supermarket “Fresh meat display”. Impressive display of lean beef and pork from locally processed animals cut to local specifications. Only a few years ago this would have been a mess of meat. Product quality and general trends are maturing quickly in Vietnam now.

Demand remains the main constraint for live export. There was talk that some importers had been offered prices around US$3.20 CIF, which would have been profitable before COVID. But abattoir throughputs are reporting approximately 30-40% below historically normal numbers and there are now only about 20 abattoirs actively receiving Australian cattle through 4 importers, compared to 60-100 from around 10 importers before 2021.

The question remains as to what will happen to supply when tourist numbers return to normal. The lack of tourist numbers, and specifically Chinese tourists, is having an impact on the economy and on beef demand. China accounted for about 30% of foreign tourists to Vietnam pre-COVID but they dont look to return until the second half of the year due to restrictions on flights and permits to travel.

The Laos Vietnam border is expected to open for regional trade of cattle soon to supplement supply of livestock back into the country. The restrictions were put in place due to the detection of salbutamol in meat and urine in cattle, and lack of adherence to quarantine requirements. As the restrictions lift it is unclear what the new movement regulations will be or how long testing will last for.

Darwin / Townsville

We have seen several shipments out of Darwin in February. A total of 19,420 cattle were shipped out of Darwin during the month: 17,958 were sent to Indonesia and 1,472 to the Philippines. This is up from 5,526 in January and the 17,821 total for February 2022. Export numbers out of other ports were not available at time of publication, but there were two further shipments to Vietnam in March.

Although prices for live export cattle are starting to drop in Australia, the herd rebuild in the North is likely to continue across much of the region due to recent rains across much of the region. This has reduced the need for farmers to move cattle and in some cases the ability or cost to move cattle to ports is prohibitive. We are likely to continue to see a slow market from a supply side. Given the concurrent depressed demand in the key live export markets, it looks like it will be a slow start to the year for live exports.

Across the North, 280-380kg feeder steers are attracting around $4.20 and $4.00 for heavy steers over 450kg although as always prices range considerably. Cows have dropped below $3.00. It is understood that there are some motivated exporters and with the sharp drop in the EYCI we may see a reflection in prices of cattle sold into the markets by next month if demand increases.

China: Slaughter steer AUD $7.66 / kg live weight (RMB 4.65 = 1AUD$)

China prices for beef prices have had minimal change in Shanghai and Beijing in Jan to 96-102 RMB in wet markets and 126 RMB in supermarkets. Live cattle prices have remained unchanged at 35.6 RMB/kg liveweight (AUD 7.66) which is a reduction on last month.

China’s crackdowns at the borders continue with potentially significant impacts for the South East Asian region. The Vietnamese border has now moved towards strict legal trade of all goods barring a very small number of black market trades. Chinese GACC require products to show property codes and reprocessing or value adding plants in Vietnam are now audited for capacity and use. The impact to the beef industry is that it is now difficult to move beef products or cattle across the Vietnam border into China. The impact is that we will likely see this trade increasingly deviate to Laos or Myanmar where political relationships are better and China has invested in infrastructure through the Belt and Road Initiative.

Philippines: Slaughter Cattle AUD $3.52 / kg (Peso 36.93 to 1AUD$)

Contacts in the Philippines have reported that the general costs of living have not been impacted much in the last month. However, the price of onions has surged to be more expensive than meat and even higher than the country’s minimum wage. This inflation and the rising cost of living are expected to be a common issue throughout the year. To address this, the government has committed to limiting the impact on citizens and promoting local agricultural production.

In terms of cattle prices, there has been no change since November with the price sitting at P.130/kg for slaughter cattle. There are no other notable price changes to report in the Philippines, with knuckle prices remaining stable at P.560.00/kilo in the Mindanao wet market and P.600.00/kilo in supermarkets.

Thailand: Slaughter cattle AUD $4.10 (Tb 23.15 to AUD1$)

Thailand prices for cattle and beef have remained stable over the period although there is increasingly a need to move cattle across the borders again. Movement restrictions into Vietnam are expected to be lifted in the coming weeks and we are therefore likely to see some pressure taken off local traders to find alternative markets for Thai cattle.

The question remains as to how hard Vietnam will police the borders in regard to both quarantine restrictions and salbutamol testing, and for how long. From some meat yield data I have seen in abattoirs that are clean, there is a significant impact to lean meat yields and without its use the profitability of any live cattle slaughter remains questionable.