137th Edition: June 2025

Key Points:

- China’s domestic cattle prices improving, but Australian live exports remain well below previous levels.

- Indonesia’s live cattle imports hesitate momentarily amid import permit uncertainty; positive government signals yet to translate into renewed buying.

- Vietnam’s weakening currency adds cost pressure on cattle imports as competition from boxed beef continues to weigh on demand.

Regional Trends and Overview

China cattle market in recovery mode

Dr Michael Patching

China’s domestic beef and live cattle prices have been edging higher — a potential positive sign for Australian exporters.

In May 2025, the national average beef price reached RMB 69.89/kg (approx. AUD 15.10/kg), while live cattle in key provinces such as Hebei averaged RMB 26.89/kg (approx. AUD 5.81/kg), up 16.2% year-on-year.

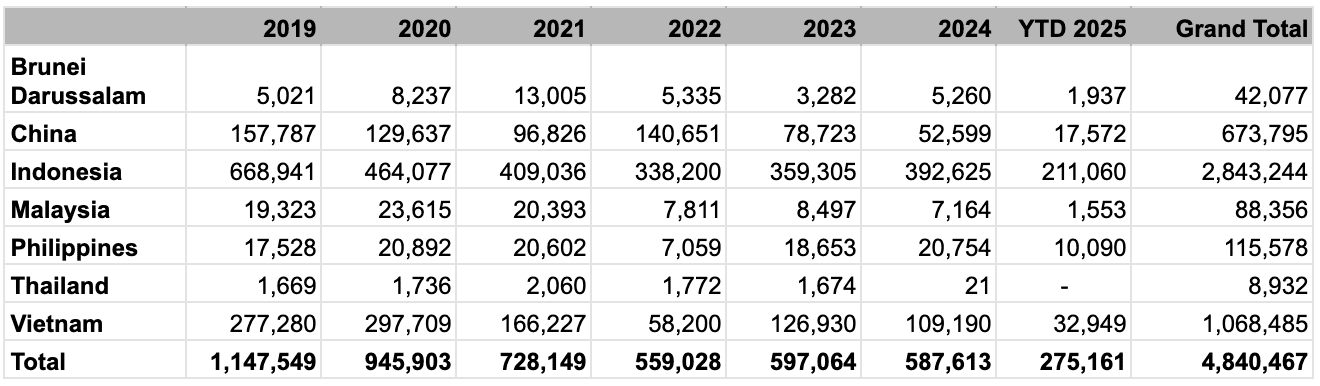

But so far, this price recovery hasn’t flowed through to Australian breeder cattle exports. After falling sharply to just 52,599 head in 2024, exports to China have slowed even further this year — with only 17,572 head shipped year-to-date.

The drop in imports is also a reflection of what has been an over production in China’s domestic market. But will stronger local prices eventually pull more Australian breeder cattle into the market? Possibly — but for now, the trade remains well below the levels we were seeing just a couple of years ago. It’s one we’ll continue to watch closely in the second half.

Cambodia and Laos: Import bans imposed, partial easing as anthrax concerns persist

In early May, Vietnam, Cambodia and Laos imposed temporary bans on livestock and meat imports from Thailand following an anthrax outbreak in Mukdahan Province. By late May, Laos partially lifted its ban for disease-free provinces under strict protocols, though restrictions remain for products from Mukdahan. Thailand is now in talks with Laos and Vietnam to lift the remaining cattle import bans. Prior to the suspension, 10,000–15,000 head were moving monthly via Nakhon Phanom in the country’s northern region. Thailand officially exported 133,416 live cattle in 2024 — a 53.1% increase on 2023’s 87,144 head. Of this total, 58,236 head went to Vietnam, 38,222 head to Malaysia, and 36,958 head to Laos. The unofficial number is likely much higher.

While the trade disruption has been sharp, industry contacts suggest that demand in Vietnam and Laos remains strong — if disease controls can be managed effectively, the flow of cattle should pick up again fairly quickly. These border negotiations should continue to progress in the weeks ahead.

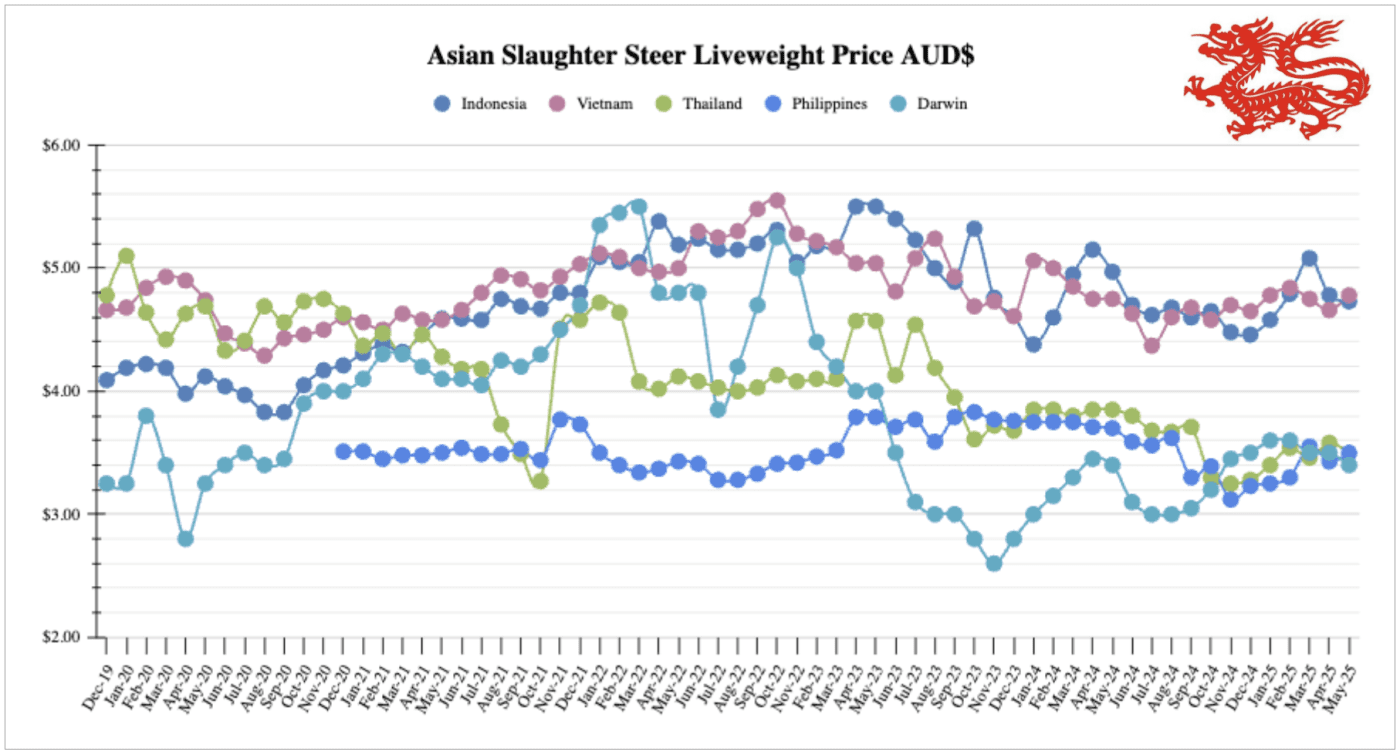

Indonesia: Slaughter Steers $4.73 AUD per kg live weight (IDR 10,476 = $1 AUD)

Prices

Slaughter steer prices in Lampung have eased slightly in June, now averaging IDR 49,500 per kilogram live weight ($4.73 AUD). Heifers are trading at IDR 47,500/kg ($4.53 AUD). The adjustment reflects higher feedlot inventories and a typical softening of demand following Ramadan. From conversations with local operators, margins remain under pressure — but for now, inventories are moving steadily enough to avoid a more severe correction.

Industry and Trade Developments

There is some uncertainty around import permits for live cattle for the second half of 2025. Indonesian feedlots are still operating under their existing import permits, with no additional permits allocated at this stage. The Indonesian government took a different approach this year, issuing only half the usual number of permits initially — a move aimed at enforcing the condition that importers must bring in 3% breeding cattle alongside their feeder cattle.

Some feedlots have exhausted their import quotas, while many others have not yet been able to utilise theirs. Feedlots that have run out but hold contracts with exporters may borrow quotas from other feedlots; however, this involves lengthy administrative procedures and requires approval from various government bodies. In the meantime, feedlots that have used up their quotas are attempting to import breeding cattle, which is a primary requirement for securing additional import quota allocations.

Many importers remain cautious about forward bookings until there’s clarity around when the remainder of this year’s permits will be released. That said, there’s reason for some optimism following the government’s recent move to increase the total 2025 import quota, as reported by Beef Central.

Whether that change flows through in time to support Q3 shipments remains to be seen — but it will certainly help restore some confidence if the new permits land soon.

Qurban demand softens

Photos: Beef from Qurban sacrifice prepared for community distribution in Lampung

This year’s Eid al-Adha (Qurban) period has now wrapped up, with participation falling to its lowest level in recent memory — even below the pandemic years.

According to a study by the Institute for Demographic and Affluence Studies (IDEAS), an estimated 1.92 million Muslims performed Qurban this year, down from 2.16 million in 2024. The decline was clearly felt across the trade, with reports from local processors and vendors in Lampung suggesting that cattle sales into the Qurban market were notably softer than usual. Rising unemployment, reduced consumer purchasing power, and economic uncertainty among the middle class all contributed to the weaker demand.

Qurban typically provides an important sales window for fresh beef from Australian cattle. While some volumes still moved through wet markets (see photos), the overall softness will weigh on short-term demand heading into the second half of the year.

Vietnam: Slaughter Steers $4.78 AUD per kg live weight (VND 16,835 = $1 AUD)

Industry and Trade Developments

Vietnam’s currency has been gradually weakening against the US dollar over several years — officially not a deliberate policy, though many in the local business community suspect otherwise. The softer VND has supported Vietnam’s export industries, particularly manufacturing and seafood, but it’s proving a challenge for importers. Live cattle importers are feeling the pinch, with the weaker currency driving up landed costs at a time when competition from imported boxed beef is already eroding demand for local cattle. The combination of these factors is making buyers more cautious and weighing on overall market activity.

The anthrax outbreak in Thailand and subsequent border restrictions for cattle don’t appear to have affected local live cattle prices in Vietnam just yet, though there has been a slight uptick over the last month.

Philippines: Slaughter Steers $3.50 AUD per kg Live weight (P35.71 = $1 AUD)

Prices

Wet market beef prices remain steady at around ₱390/kg ($10.92 AUD), while supermarket rates have eased slightly to ₱440/kg ($12.32 AUD).

Slaughter steer prices have dipped to ₱125/kg live weight ($3.50 AUD).

Pork and broiler prices continue to firm slightly, with pork carcass now trading at ₱228/kg ($6.39 AUD) and broilers edging up in recent weeks.

Photos: Local meat and livestock sales in Mindanao

Industry and Trade Developments

Live cattle consignments into the Philippines have continued to track slightly above long-term averages in 2025 — a positive sign for what remains an important secondary market for Australian exporters. Average consignment sizes are now consistently pushing past the 3,000 head mark. While demand here remains more price-sensitive than in larger markets like Indonesia or Vietnam, the steady growth in trade volumes is encouraging.

From discussions with local importers, the mood remains cautiously optimistic. There’s awareness that the Philippines’ economy is holding up reasonably well compared to some neighbours, which is supporting ongoing demand for beef and live cattle — though as always, currency movements and consumer spending trends will be key factors to watch as the year progresses.

Source: DAFF website – All live exports data

Australia: Feeder Steers Darwin $3.40

Feeder steer prices ex-Darwin eased through May to around $3.40 AUD per kilogram live weight. With the Darwin market so heavily tied to Indonesian demand, it remains very much a story of how that market is tracking. Buyer interest dried up noticeably through May in the lead-up to Eid — driven by full feedlots and ongoing uncertainty around import permits. Without clear signals from Jakarta, many Indonesian importers have been reluctant to commit to new orders. That said, sentiment on the ground is still positive. Indonesian feedlotters report a strong start to the year and welcome the government’s recent messaging around increasing import quotas and managing the impact of lumpy skin disease.

From an Australian perspective, exporters and producers will be watching closely over the next month or two to see when buying activity picks up again. With solid northern yardings and feeder supply in reasonable balance, the capacity is there to respond quickly once Indonesian demand reactivates.

Year 2025 cattle exports – comparison across SE Asian markets

Source: DAFF website

HAVE YOUR SAY