120th Edition: January 2024

Key points:

● Indonesian election in February is a major consideration for trade

● Q1 is Festival period in Asia. Tet/CNY 10 February and Ramadan in March

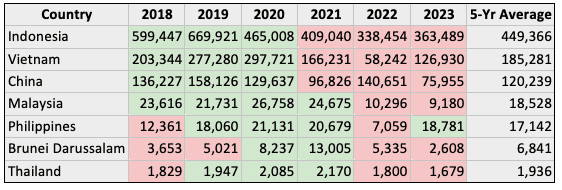

● Live Exports remain below 5 year averages

Regional Trends and Overview

Dr Michael Patching

The first quarter of the year is a period of disruption, trade, and often disrupted trade.

While many Australians still haven’t had time to start to recover back any of the Christmas kilograms, the rest of Asia is already focused on other key events. These are worth noting if you are trading or travelling soon.

In Asia the Christmas and New Year holidays are shorter with many locations having only one or two days holiday. Although there are always delays at ports with officials making the most of the change in the calendar year to take holidays.

For Vietnam, China, and Singapore the Lunar New Year, Tet in Vietnam or Chinese New Year (CNY), which is officially on the 10 January is their extended family event. It causes disturbances from as early as the 5 Jan and lasts for generally the whole week and sometimes more. Bringing products or having meetings with anyone in Vietnam and China over this time can be difficult as everyone generally returns to home villages in the countryside. The city generally closes and consumption in the main cities decrease, while overall consumption in the country increases.

Once we get beyond that we encounter Ramadan in Malaysia and Indonesia which is from 10th March until April 9th in 2024. This is a period of fasting during the day and banqueting with family at night. It results in a significant increase in consumption for meat and locals are starting to think about it now, feeder live cattle should theoretically be arriving into Indonesia for this now. For completeness Hari Raya Haji/Eid al-Adha/Qurban is around the 16 June this year and is the festival of sacrifice in the Muslim world which is marked by a pilgrimage to Mecca or live sacrifice of livestock.

Photo: Vietnamese Wet Market. Thit Bo means Fresh Beef

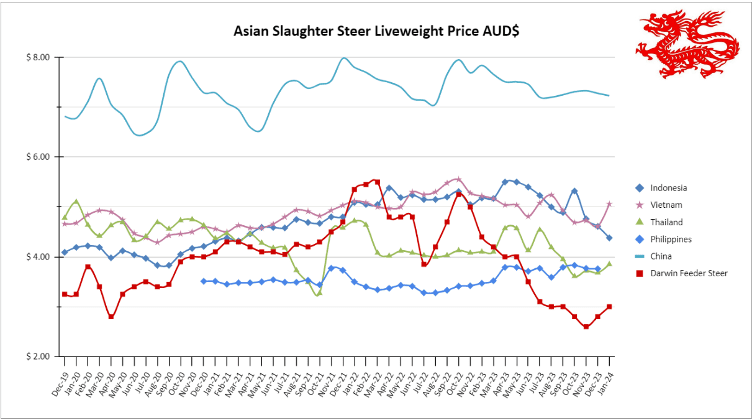

Indonesia: Steers AUD $4.38 / kg live weight (IDR 10,394.16 = 1 AUD)

In the period leading up to Christmas 2023 and the New Year there was a notable increase in beef prices in the market, along with other staple foods like rice and chicken meat. Specifically, more premium beef prices saw a rise of 0.36 percent, an increase of Rp500, to reach Rp138,150 per kilogram (kg). Lower quality beef experienced a slightly higher increase of 0.66 percent, going up by Rp850 to reach Rp129,450 per kg. Across most cities, beef prices escalated from around Rp130,000 per kg to approximately Rp140,000 per kg.

December saw a big end to the 2023 live export calendar with 58,250 cattle sent to Indonesia, a significant jump on previous months. This was partly driven by motivated Indonesian importers looking to utilise their existing import permit allowances prior to them expiring, particularly because of uncertainty around the issuing of new 2024 import permits by the Indonesian government. As of mid-January some Indonesian importers had not yet received new import permits which is holding up new orders and of significant concern given that feedlots are looking to fill their inventories leading in to the festival periods mid-year.

Addressing this situation, the Coordinating Minister for Maritime Affairs and Investment, Luhut Pandjaitan, emphasized the government’s efforts to bring beef prices down to below Rp100,000 per kg. He expressed optimism that by March 2024, prices might even fall to between Rp80,000 and Rp90,000. This reduction, he suggested, could be achieved through increasing beef imports, not just from India and Australia, but also from other countries like South Africa, Kenya, and Brazil. Additionally, the possibility of importing buffalo meat from Australia was mentioned.

Alongside beef, Luhut stated the government’s intention to import breeding bulls and calves from Brazil. He reassured that Foot and Mouth Disease (FMD) should not be a concern due to the implementation of quarantine measures.

Indonesia’s Election Debate: Dairy Imports and School Milk Program

The Indonesian election is important for Australian interests in the region and should be reiving more attention than the American primaries. Especially for Australian interests in exports and relationship with our near neighbour.

In the thick of Indonesia’s election campaign, Presidential candidate Prabowo Subianto has put forward an ambitious proposal. He advocates for importing 1.5 million dairy cows, likely from India, to support a national initiative: providing free milk to schoolchildren. Prabowo argues that cow-sourced milk, free from added sugar and preservatives, is superior to packaged varieties. The program aims to distribute milk to an estimated 82 million children, requiring about 4 million tons annually. To sustain such a massive milk production, Prabowo suggests maintaining a herd of 2.5 million cows, emphasizing long-term investment in domestic cow development.

However, this proposal has met with criticism. Vice Presidential candidate Cak Imin has expressed scepticism, warning against hasty moves that might benefit importers disproportionately. He advocates for diversifying protein sources, pointing out limited public interest in milk and the prevalence of milk allergies. Instead, Cak Imin recommends focusing on the agro-maritime sector.

Adding to the debate, Presidential Candidate Ganjar Pranowo urges for economic self-sufficiency. He supports developing Indonesia’s own breeding and production facilities, moving away from reliance on imports.

Teguh Boediyana, Chairman of the National Dairy Council, also weighed in. He acknowledges the need for dairy imports to meet the annual demand of 4 million tons of fresh milk – a figure significantly higher than the current domestic production of 800,000 tons. While he agrees with the concept of importing dairy cows, Boediyana finds Prabowo’s figure of 1.5 million cows unrealistic. He suggests a more gradual approach and seeks clarity on operational responsibilities – whether it will involve small-scale farmers or larger corporations. Additionally, Boediyana raises concerns about importing cows from India, citing disease-related quarantine challenges and the lack of a suitable quarantine facility in Indonesia.

Implications of Indonesian Import Policies for Australian Cattle and Beef Exporters

The Indonesian government has recently made significant decisions regarding meat imports. In 2024, they have allocated a quota of 100,000 tons of buffalo meat imports from India to Perum Bulog (Bulog), a state-owned enterprise. Additionally, the private sector in Indonesia has been granted permission to import 50,000 tons of Indian buffalo meat. ID Food, a government-controlled holding company, is also set to import 20,000 tons of beef from Brazil.

These decisions are crucial for Australian cattle and beef exporters, as Indonesia has been a key market for live cattle exports. The shift towards buffalo and beef imports from India and Brazil may influence the demand for Australian products and shows a growing narrative of a shift away from Australia.

Further complicating the scenario is Presidential candidate Anies Baswedan’s pledge to reassess Indonesia’s beef import policies if elected in 2024. Anies has critiqued the current import strategies, suggesting they may be detrimental to local Indonesian farmers’ welfare. He advocates for greater investment in domestic beef farming to boost production and meet Indonesia’s growing beef consumption needs. This focus on enhancing local production could potentially reduce Indonesia’s dependence on imported cattle and beef, including those from Australia.

For Australian exporters, these developments signal a potential shift in the Indonesian market. A move towards self-sufficiency in beef production in Indonesia, or a preference for red meat imports from countries other than Australia, could lead to a decline in the demand for live Australian cattle or at least a shift from a preference for imports. The extent of this impact would depend on the specific policies enacted and their actual implementation.

It’s important to note that while these policy proposals and commitments are significant, their actual execution and effect on the Australian cattle and beef export market might unfold gradually. This evolution will likely be influenced by various factors, including political negotiations and global market dynamics. Australian exporters should closely monitor these developments to anticipate and adapt to potential changes in the Indonesian market.

Vietnam : Steers AUD $5.06/ kg live weight (VND16,217.52 = 1AUD)

The pricing dynamics for Australian cattle delivered to Vietnamese abattoirs remain competitive, offering a cost-effective alternative to local cattle and imports from Thailand and Laos. There’s been an increase in steer prices, now at VND 86,000 per kg liveweight.

With the Lunar New Year (Tet) in Vietnam approaching in early February, expectations for boosted cattle sales are rising. Tet, a time of heightened meat demand due to festive meals and gifting, often leads to a temporary spike in live cattle prices. Farmers tend to withhold stock in anticipation of higher prices during this period. However, accurately predicting the exact impact of Tet on cattle prices is complex, and as we regularly comment the demand for the period is now influenced by competitive pressures from beef imports and imported cattle from the region.

Although December recorded several live cattle shipments arriving in Vietnam, January is expected to be quieter for deliveries. Current understanding suggests that Vietnamese feedlots are sufficiently stocked for the Tet period. Given the recent price increase of Australian cattle, importers in Vietnam are likely to closely monitor price trends to make informed decisions for the remainder of 2024.

Printed Source: Asia Beef Network

Feeder Steers Darwin $3.00 Townsville $2.90

Indonesia helped with a serge of imports in December, but lack of permits in January for Indonesia and full feedlots in Vietnam has affected export demand in January. The speed that the permits will be issued in time for the festive period stocking will be a major determinant of volumes in the first half of 2024.

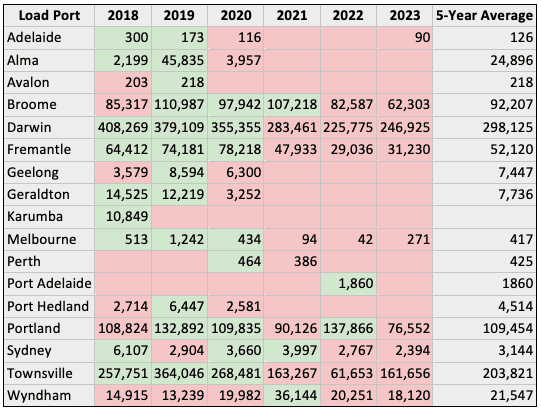

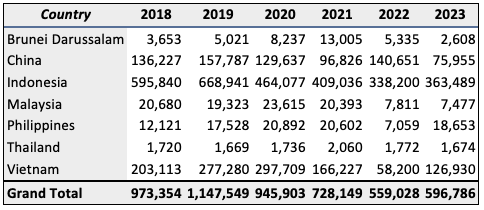

2023 Year to December figures for cattle sea freight across Asia for our different ports from the DAFF website:

Year to December for cattle sea freight comparison across Asian markets from DAFF figures:

2024 Live Exports In Review

Given the high prices of Australian cattle and reduced demand from key markets, plus the emergence out of COVID impacting 2022 numbers, 2023 was always pegged to be an important year to see how things were going to rebound. With the release of the official numbers it seems to have created more questions than answers.

Vietnam has clearly bounced back from a slump in imports in 2022, however there should remain some caution about interpreting these numbers too positively. Another importer has gone into bankruptcy and cattle are being managed by the bank and a large importer is leasing out their northern feedlot to a local dairy fattening operation. If cattle prices remain competitive it is likely that imports will continue around the 100,000 mark, given the concurrent decrease in overall live export turnoff from the north of Australia it is likely Vietnam will still maintain a key relief value for producers.

Indonesia has done little in the last 12 months to assure anyone that we are going to see a resurgence in imports above 5 year averages irrespective of what happens with the price. The impact of FMD and LSD, combined with high cattle prices and low availability, plus the changing demands from consumers who have now greater acceptance for frozen imports and IBM has found a place at least in the bakso ball market. Added uncertainty from the elections and the outcomes from that is surely impacting import appetite from Indonesian importers, feedlots, and abattoirs.

The big question is what is happening in Northern Australia, especially the NT. Mathematically and logically there should be significant numbers of cattle available that were not exported in 2023 or have been moved somewhere else in Australia. It is possible we are either starting to see, or are about to see a fundamental shift in supply chains in the north with less cattle going into live export.

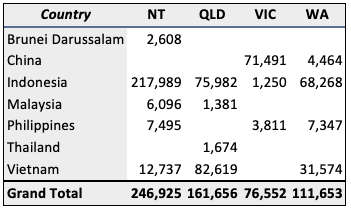

The southern ports of Portland and Adelaide are connected to breeder trade, mostly to China. And we have included airfreight in the port table for completeness, these would all be breeder cattle.

5-Year Average by Market

5-Year Average by Port